SAP SE (NYSE: SAP), the German enterprise software conglomerate, continues to embrace the predictable revenues and higher multiples of its subscription-based cloud business, even as it deals with the acquisition costs of Qualtrics, a deal that closed January 23.

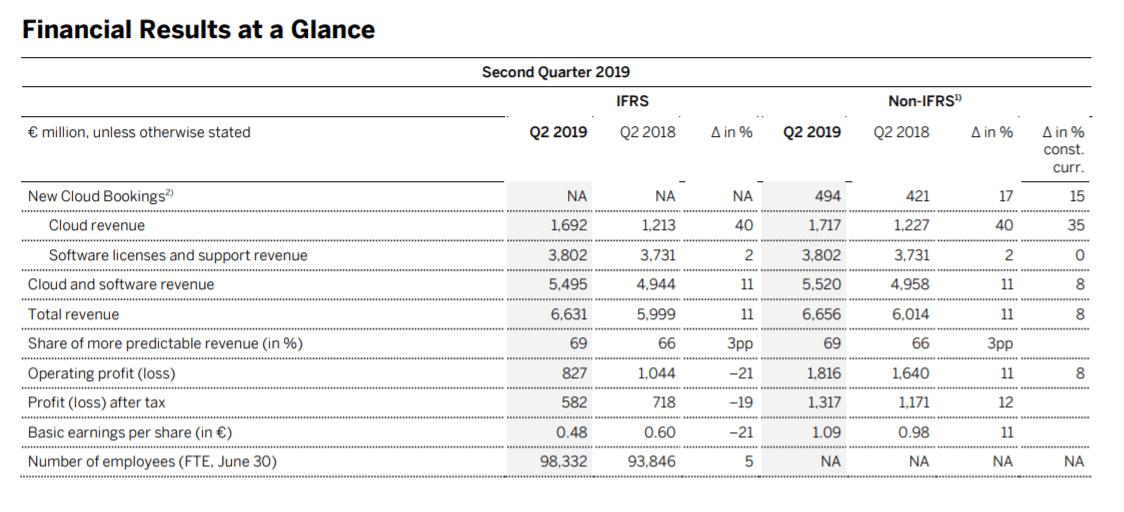

SAP posted basic earnings of €.048 per share (1 Euro = $1.12), or, on a non-IFRS basis, €1.09 per share. Total revenues were up 11 percent year-over-year to €6.65 billion (adjusted), and the share of more predictable revenue – i.e., cloud-based revenue and software support revenue – increased to 69 percent from 66 percent in the previous quarter. SAP management provided guidance that more predictable revenue will account for anywhere between 70 and 75 percent of its total revenue for the full year.

While Goldman Sachs equities analyst Mohammed Moawalla described SAP’s results as “modestly below expectations” in a client note, he wrote that “we do not see any changes to our long-term structural growth thesis on SAP.” Cloud revenues missed Goldman’s expectations by 4 percent, while total revenues missed Goldman’s expectations by 2 percent.

UBS equities analyst Michael Briest wrote that “disappointment with these results is likely,” calling out cloud bookings growth of “just” 15 percent and flat EBIT margins on the cloud business, despite no foreign exchange hit and improved gross margins. Higher general and administrative costs expenses may have been the chief culprit there.

Telling, software license sales were down 5 percent; the company blamed it on trade tensions that depressed Asia-Pacific results. The customer growth mix on S/4, its core platform, was about 50 percent net new customers, which may indicate that SAP is having trouble converting its legacy on-premise customers to the cloud, which drives more predictable revenue on higher margins.

This is a company that continually makes acquisitions (one so far this year but four in 2018) to grow top-line revenue but adds back acquisition costs and margin impacts in its non-IFRS financial reporting. The impact of the Qualtrics acquisition continues to be a profitability headwind, as seen in the unadjusted and adjusted operating profit numbers: unadjusted, operating profits were down 21 percent to €827 million; adjusted, operating profits were up 11 percent to €1.82 billion.

“SAP delivered double digit growth in total revenue, cloud revenue and non-IFRS operating income,” said Bill McDermott, CEO, in a statement. “Qualtrics is growing fast as the global standard in the Experience Management category. As shown by our rising cloud gross margins, we are progressing nicely on our ambition to be the Best-Run SAP. With XM driving the CEO digital transformation agenda, we resolutely reaffirm our full year guidance.”

SAP breaks out its business into three segments: Applications, Technology & Services (AT&S); Intelligent Spend Group; and Customer and Experience Management.

AT&S, which includes SAP S/4HANA, the company’s core enterprise resource management platform, grew revenues by 6 percent. Human Capital Management Solutions, the employee experience platform, SAP Leonardo, an artificial intelligence/machine learning analytics offering, and SAP’s cloud analytics business are also included in the segment.

The Intelligent Spend Group segment includes collaborative commerce (SAP Ariba), travel and expense processing (SAP Concur) and flexible workforce management (SAP Fieldglass). Revenues for the Intelligent Spend Group grew 22 percent in the quarter as it added new customers like Kawasaki Heavy Industry and Uniper.

Customer and Experiencement Management revenue was up 81 percent year-over-year to €365 million; comparisons benefited from the Qualtrics acquisition. SAP’s customer management platform, SAP C/4HANA, which competes with companies like Salesforce, is also included in the segment, but the growth likely was almost entirely due to Qualtrics.

“I am pleased that our operational excellence measures are already showing effect,” said Luka Mucic, SAP chief financial officer. “Our non-IFRS operating profit and margin performance is remarkable considering the margin headwinds from our latest acquisition and the recent short-term trade-related uncertainty in Asia that impacted our software revenue performance in the region. With continued strong customer demand and our tight focus on profitability, we remain as confident in our 2019 outlook as we are in our mid-term ambition.”