Amazon imposes inventory-placement fees and low-inventory fees

(Photo: Jim Allen/FreightWaves)

For anyone involved with selling through Amazon, I recommend going through the latest newsletter published by Cartograph, a company that helps brands sell profitably on Amazon. I interviewed Chris Moe, Cartograph’s CEO, on past The Stockout shows. Those discussions impressed upon me that brands must understand, and play by, Amazon’s numerous and frequently changing rules in order to sell profitably through the online giant. Now, Amazon is changing its policies for inventory placement within its fulfillment centers while also adding low-inventory fees. Both of these changes to fees seem to more heavily penalize smaller brands that are more likely to use smaller shipments and those that sell lower-value items, including CPG items.

Inventory-placement fees potentially punitive to LTL shipments:

What stood out to me in Cartograph’s writeup is the dramatic changes to potential fees associated with LTL shipments, which, in some cases, could rise from the low to mid-$100s to $2,000 or more per shipment. That could encourage some brands to consolidate LTL shipments into larger truckload shipments, but, according to Cartograph, that’s not necessarily better because Amazon will still rebalance inventory between warehouses at brands’ expense.

Low-inventory fees to impose explicit cost on de-prioritizing Amazon as an inventory channel:

New fees will be imposed for having less than 28 days of inventory, calculated weekly as average days of supply over 30- and 90-day periods. When both averages (30 and 90 days) fall below 28 days of inventory, there is a fee that ranges from 30 cents to $1 per item shipped (fees escalate at lower inventory levels). Since it’s calculated at the product level (which Amazon calls the Amazon Standard Identification Number), some varieties of a product can be out of stock without the brand incurring a fee. Since the fees are calculated weekly, Cartograph recommends moving products in and out of Amazon warehouses weekly. Another strategy is to reduce advertising and promotional spending when inventory levels decline to low levels.

Use Shein’s supply chain at your own risk

(Image: FWTV)

On Monday’s The Stockout show, Grace Sharkey and I discussed the impact of the Francis Scott Key Bridge collapse, Shein’s opening of its supply chain to outside designers, Home Depot’s acquisition and the current freight market.

The focus of the show was on last week’s announcement that controversial fast fashion online retailer Shein plans to launch a supply chain as a service offering. That would enable outside brand designers and manufacturers to tap into Shein’s supply chain infrastructure and technology, which uses real-time data to inform small-batch production schedules. Leveraging Shein’s supply chain could enable brands to test new designs efficiently without the need for large capital investments. The risk of using the company’s supply chain as a service is that outside brands could become entangled in the same controversies, which include suspicions of the use of forced labor in China, the circumvention of import duties, intellectual property infringement and environmental concerns.

See Monday’s episode here or see the full The Stockout playlist here.

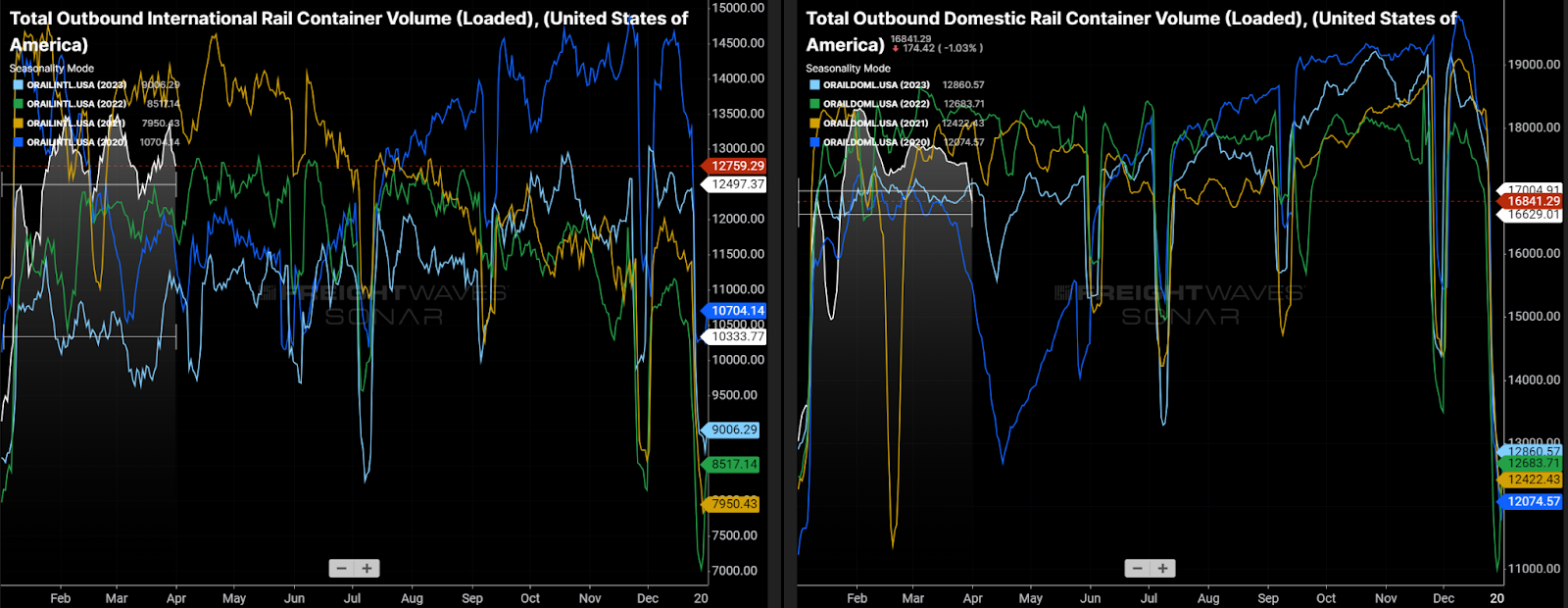

International intermodal outshines domestic intermodal in Q1

SONAR Tickers: ORAILINTL.USA Seasonality, ORAILDOML.USA Seasonality

Most public intermodal volume data sets conflate international and domestic intermodal volume, which should be treated as separate segments, as SONAR does. In Q1 2024, international intermodal was responsible for most of the intermodal volume growth. Specifically, in Q1, loaded international intermodal volume was up 20.9% year over year, while loaded containerized domestic intermodal volume was up 2.2%. Meanwhile, the more widely seen containerized intermodal volume data published by the Association of American Railroads was up 11.3% through March 23. That number includes both domestic and international volume as well as empty containers that are being repositioned (known as revenue-empties). SONAR data shows that revenue empties were up 28.8% year over year in the first quarter, primarily as a result of international containers being repositioned back to the port.

Containership lines are only willing to send international intermodal volume inland in large quantities when there are plenty of oceangoing containers available, as there appear to have been in the first quarter. In addition, it’s important for investment analysts to base their Q1 expectations for the domestic intermodal companies (e.g., J.B. Hunt, Hub Group and Schneider) off the domestic intermodal volume rather than a figure that combines segments. The breakdown is also important for domestic intermodal shippers, who should base their expectations for available capacity off the more modest year-to-date domestic intermodal volume growth.

To subscribe to The Stockout, FreightWaves’ CPG and retail newsletter, click here.