At this point, it’s unclear whether there will be a strike, as the International Longshoremen’s Association (ILA) is threatening, or whether a strike will be avoided, perhaps by the president invoking the Taft-Hartley Act, ahead of the strike deadline. Even a short work stoppage would greatly disrupt freight networks. Sea-Intelligence estimates that for every one day of disruption from a potential strike, it would take five days to clear. And the avoidance of a strike altogether would not avert disruption if disgruntled workers stay on the job while purposely reducing productivity levels.

The SONAR charts below show evidence of shippers looking to avoid getting caught in a potential ILA work stoppage.

Changing maritime shipping patterns

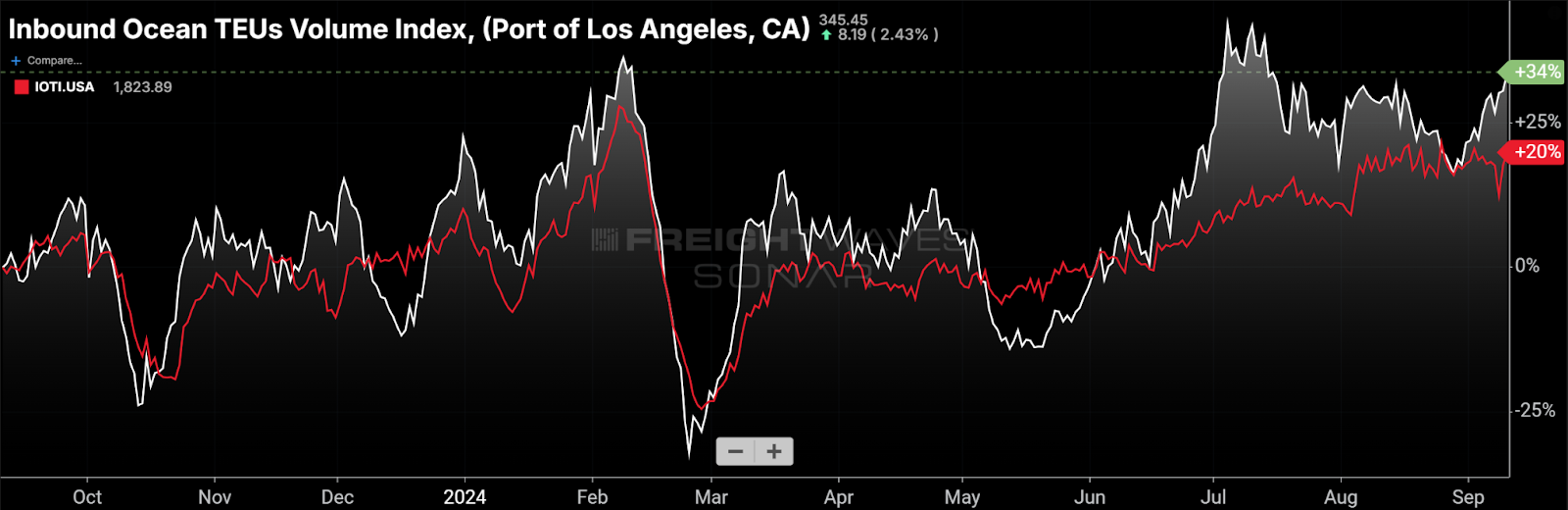

The inbound ocean booking volume index for the Port of LA has outperformed the index for the U.S. as a whole. (Chart: SONAR)

The West Coast ports have taken share of import volume over the past several months for numerous reasons. In addition to the ILA issues, West Coast U.S. port volume has benefited from the Red Sea attacks, labor issues in Canada (both on the rails and at the ports), low water levels at the Panama Canal (although those have improved of late) and, possibly, a pull-forward related to possible incremental tariffs next year.

As it relates to mitigating the risk of an ILA strike, shippers can do that in a few different ways. One is to move the goods earlier – for instance, import holiday items in July and warehouse them. Another is to move goods on vessels bound for the West Coast instead of the East. Yet another is for shippers to diversify their ports of entry – after all, shifting containers to the West Coast could end up being a “crowded trade” resulting in congestion.

Intermodal volume growth

Intermodal volume benefits from West Coast ports’ market share gains. That’s simply because the population is still most densely concentrated along the East Coast, and those routes are more compatible with the intermodal networks. The Intermodal Association of North America has estimated that around 70% of the import volume coming through the West Coast ports is moved via rail intermodal versus only about 20%-25% of import volume coming through the East Coast ports.

SONAR allows users to view rail intermodal volume outbound from specific locations, broken down between international and domestic containers as well as between loaded and empty containers. In the third quarter, loaded international and domestic intermodal volume outbound from LA is up 43% and 14%, year over year, respectively. That is well ahead of the national year-over-year volume growth over the same time period for loaded international and domestic intermodal of 16% and 7%, respectively.

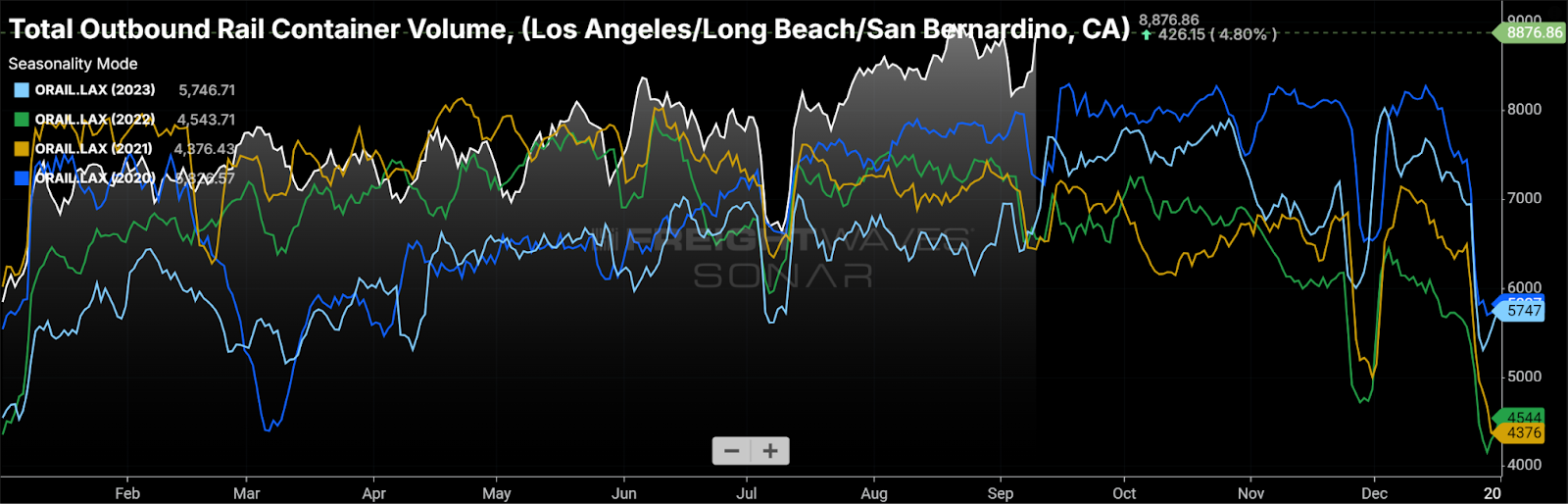

Outbound Southern California rail intermodal volume is up 26% y/y in Q3 of 2024 when all container sizes are included. (Chart: SONAR)

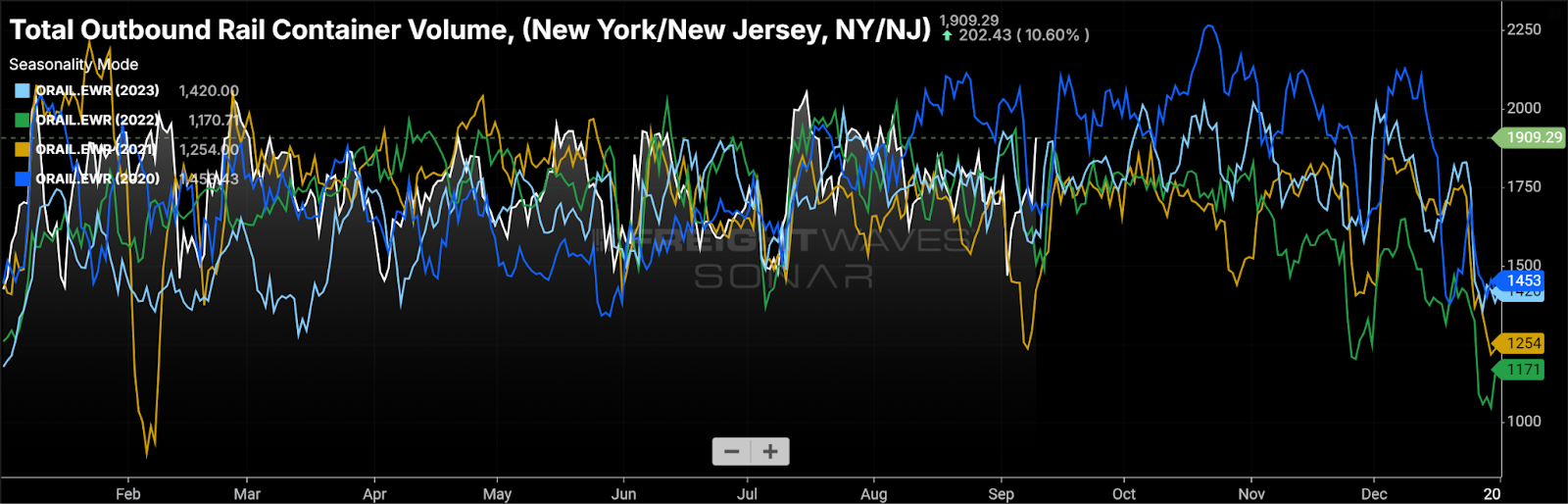

That same chart for outbound New York/New Jersey shows volume up just 1.1% y/y in Q3 of 2024. (Chart: SONAR)

Empty dometic containers inbound to LA have grown to support additional demand in the region for transloading imports from international containers into domestic containers. (Chart: SONAR)

Import volumes impact local truck markets

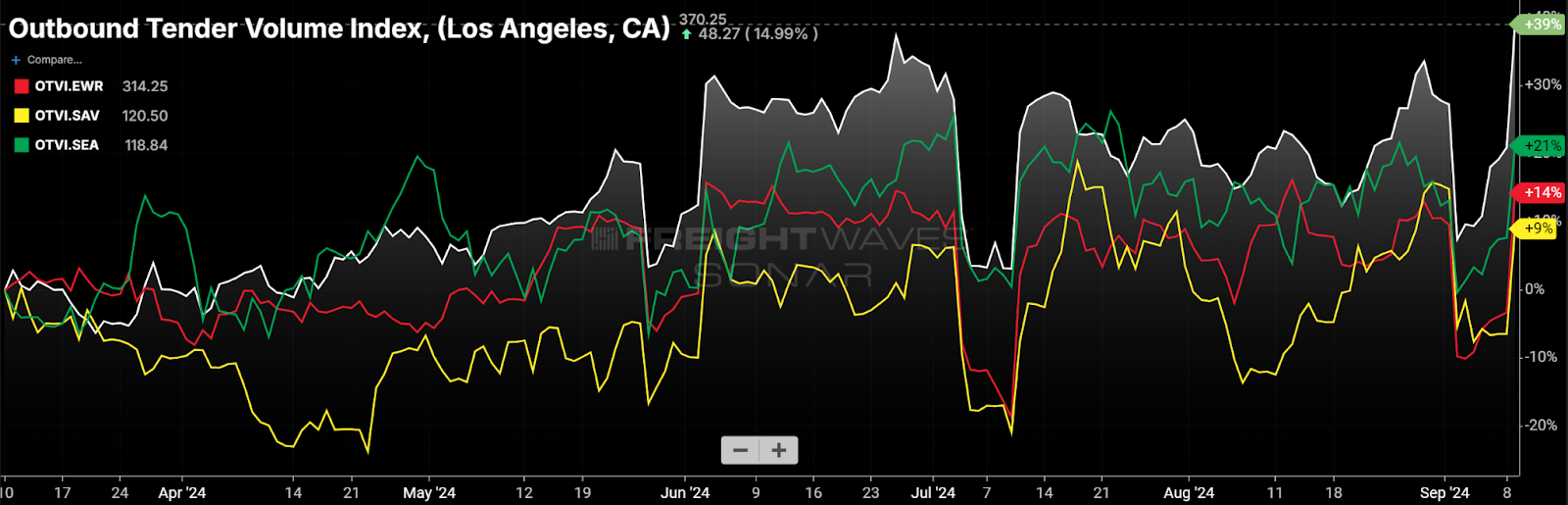

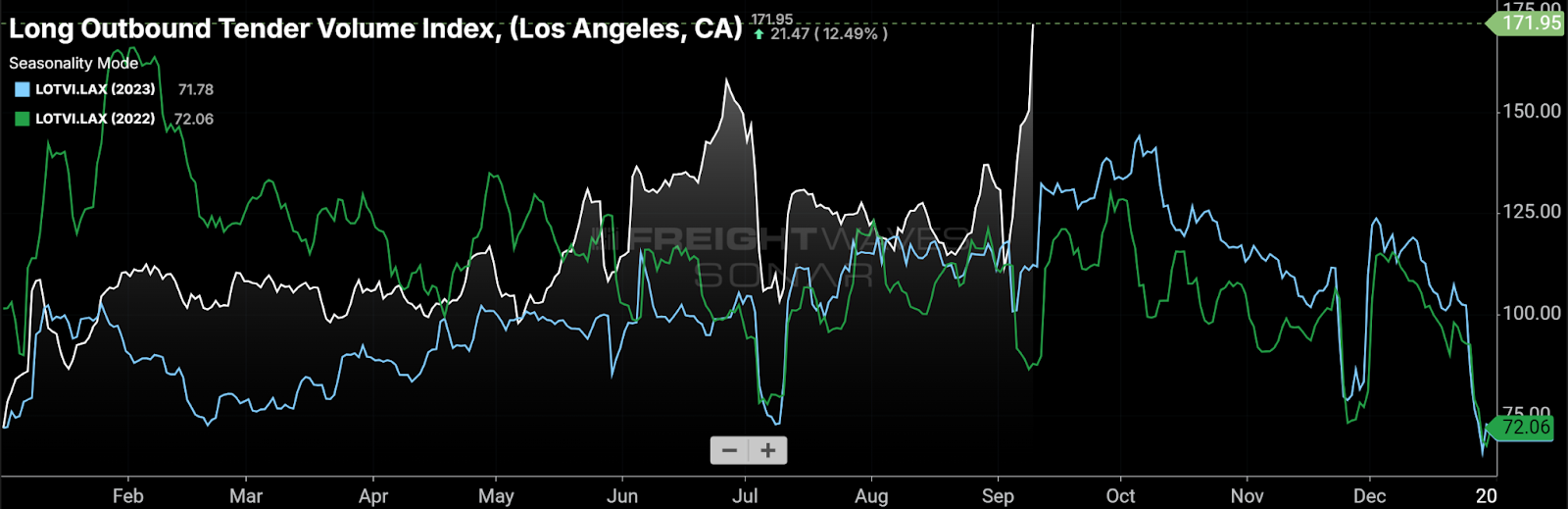

The Tender Volume Indexes for outbound LA and Seattle loads have grown faster than for outbound Newark, New Jersey, and Savannah, Georgia, loads. (Chart: SONAR)

Imports are major sources of outbound freight for port cities. A quick look at the relative tender volume indexes (a measure of truckload demand) among four port cities shows that requests for truckload movements have grown faster in the Western port cities than the Eastern port cities.

On its most recent analyst call, multimodal carrier J.B. Hunt said volume outbound from LA has not yet been commensurate with record-setting import volume at the West Coast ports – and it’s sure it isn’t losing share. Last week’s Freightonomics show explained why: There has been greater growth in upstream inventories (located near ports or warehousing districts, such as the California Inland Empire) than in downstream inventories (located in or near densely populated urban areas). The implication is that there is a lot pent-up demand to move freight eastbound from the Inland Empire later this year as the holiday season approaches.

A measure of demand, the volume of long-haul (greater than 800 miles) tenders outbound from LA spiked in recent days. This dataset, in addition to outbound LA rail intermodal volume, is one to watch as upstream inventory is moved downstream and could lead to periods of regional capacity tightness during the seasonally busy fall season. (Chart: SONAR)