The Covenant Transport Services earnings report released late Monday looked “sloppy,” one executive conceded on the company’s earnings call with analysts a day later. But the main message of that call is that it was a quarter of transition, of weak markets but implementation of cost-cutting measures as part of a broader strategic plan.

“I heard the words ‘sloppy’ or ‘messy’ last night to describe it, and it was,” Covenant co-President and Chief Administrative Officer Joey Hogan said of the company’s earnings. “The response has been to focus on the long term and doing the right thing for the business.”

Sloppy earnings report or not, investors liked what they heard. Covenant stock rose 9.36% on the day, to $18.34. That’s a gain of $1.57, which is about 45% of the just $3.48 that Covenant shares have gained over the past 52 weeks, according to Barchart.

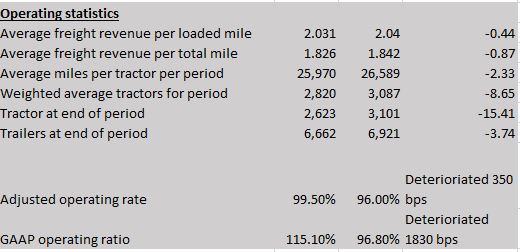

The prepared remarks section of the analysts’ call focused heavily on the restructuring steps that Covenant took, even as it posted a significant operating loss with an operating ratio of 115.1% on a GAAP basis but slightly under 100% on an adjusted basis, which led to a small adjusted net profit.

The prepared remarks in the call went right into cost-cutting measures taken by Covenant. The company sold its second-largest depot, in Texarkana, Texas, sold another facility, and consolidated staff in its headquarters city of Chattanooga, Tennessee, and its operations in Greeneville, Tennessee.

Covenant cut the size of its fleet by 10% and moved parts of its fleet into other locations, “which involved an immediate revenue loss but some ongoing expenses due to unpaid miles, a tail on fixed overhead, etc.,” CFO Paul Bunn said on the call.

Disruption pushed forward

“The sum … is that we pushed a lot of disruption and expense into a relatively weak freight quarter,” Bunn said. The earnings had net charges of $29.3 million, “but it doesn’t capture all of the related operational costs of the revenue drop-off and tail on fixed expenses.” Bunn said.

He added that there will be additional restructuring costs in the remainder of the year “but not at the level of the second quarter.”

David Parker, the company’s chairman and CEO, said on the call that the restructuring is “very close to being done.” “Where we wanted to be a year from now, we are already there,” he said.

One major piece of news about Covenant — the delay in the sale of its factoring business to Triumph Capital — was mentioned on the call, essentially a close-to-verbatim reading of what Covenant said in its earning statement a day earlier. But Hogan said Covenant management would not discuss the snag in the sale during the question-and-answer session.

One of the restructuring changes that was noted during the call was that Covenant already has taken significant depreciation charges on the restructuring of its fleet. The depreciation and amortization line item in the earnings statement of $19.6 million was actually less than the corresponding quarter of 2019, though there were equipment-related impairment charges taken by Covenant as well in the $29.3 million figure.

Lower depreciation charges going forward will save the company $1 million per month, several of Covenant’s executives pointed out on the call.

“We’re not running the business for peak season,” Hogan said, adding that the impact of peak season in the Covenant business “is getting less and less.” He said peak season this year will be “crazy” but that the company’s focus is on “long-term sustainable work systems.”

“For the balance of 2020, our main goals will be to reduce our fleet size as described above and monetize a large percentage of the assets held for sale, to allocate our fleet assets across our contract logistics, expedited and higher margin irregular route operations, to significantly lower our fixed costs and to return managed freight back to its pre-COVID margin percentage,” Hogan said in the prepared part of the analysts’ call. He said assets for sale now are valued at $66 million.

Upward pressure on driver pay

John Tweed, Covenant’s co-president and COO, replied “absolutely” when asked if he sees upward pressure on driver pay. Part of just how much pressure that involves will be determined in part by the level of unemployment pay that will come out of pandemic relief efforts by the federal government, “but I do think the quality drivers are going to cost us more money,” Tweed said.

“I don’t think we’re in an environment where we’re going to have the privilege to be able to lag on driver pay,” he said. “I don’t think the pay thing is over.”

Covenant’s adjusted operating ratio for the company as a whole, on a non-GAAP basis, was 99.5%, deteriorating from 96% in the corresponding quarter of last year.

It was noted on the call that some individual trucks, given their activity, had ORs in excess of 100% and several have been taken out of service.

But while the ORs of specific segment operations were not disclosed, management did discuss where they believed they needed to be to justify an adequate return on capital. In the managed freight segment, which includes Covenant’s brokerage and warehouse businesses, it needs to be 97% or better. That same figure is necessary on the company’s asset-heavy trucking business. The dedicated division needs to have a 92% OR, and the expedited segment requires a mid-80s OR because its capital base is higher.

More articles by John Kingston

Sale of Covenant factoring business hits a snag