J.M. Smucker Co.’s results highlight margin pressure even as CPG companies raise prices and continue to post strong sales. Overall, Smucker reported strong results as its earnings easily beat analysts’ expectations, mainly on better-than-expected sales in segments such as coffee, pet food and Uncrustables.

The company’s results give a glimpse into the continued margin pressure that CPG companies are facing even as their recently implemented price increases are passed through to consumers. In Smucker’s just-reported fiscal Q2 2022, pricing was up 3% year-over-year, from flat in Q1 2022. The company’s gross margin improved 90 basis points sequentially from Q1 but was still 300 basis points lower year-over-year. In fact, the company lowered its gross margin guidance for fiscal 2022 from a decline of 200 basis points to a decline of 280 basis points.

Those results highlight the current trend in which many CPG companies are raising prices to offset a portion, but not all, of the inflation in their costs. In so doing, CPG companies are looking to balance margin preservation and customer retention. Also, in an attempt to avoid customer backlash, CPG companies are using a number of strategies to make price increases less noticeable, such as reducing quantities and offering fewer promotions.

General Mills notified retailers that it’s raising prices in mid-January on hundreds of items, with prices on some items rising by as much as 20%. The direction of the prices will surprise exactly no one, but hearing about 20% increases is still eye-opening given that, so far, meat has been the main food product category in which prices have risen 20% or more.

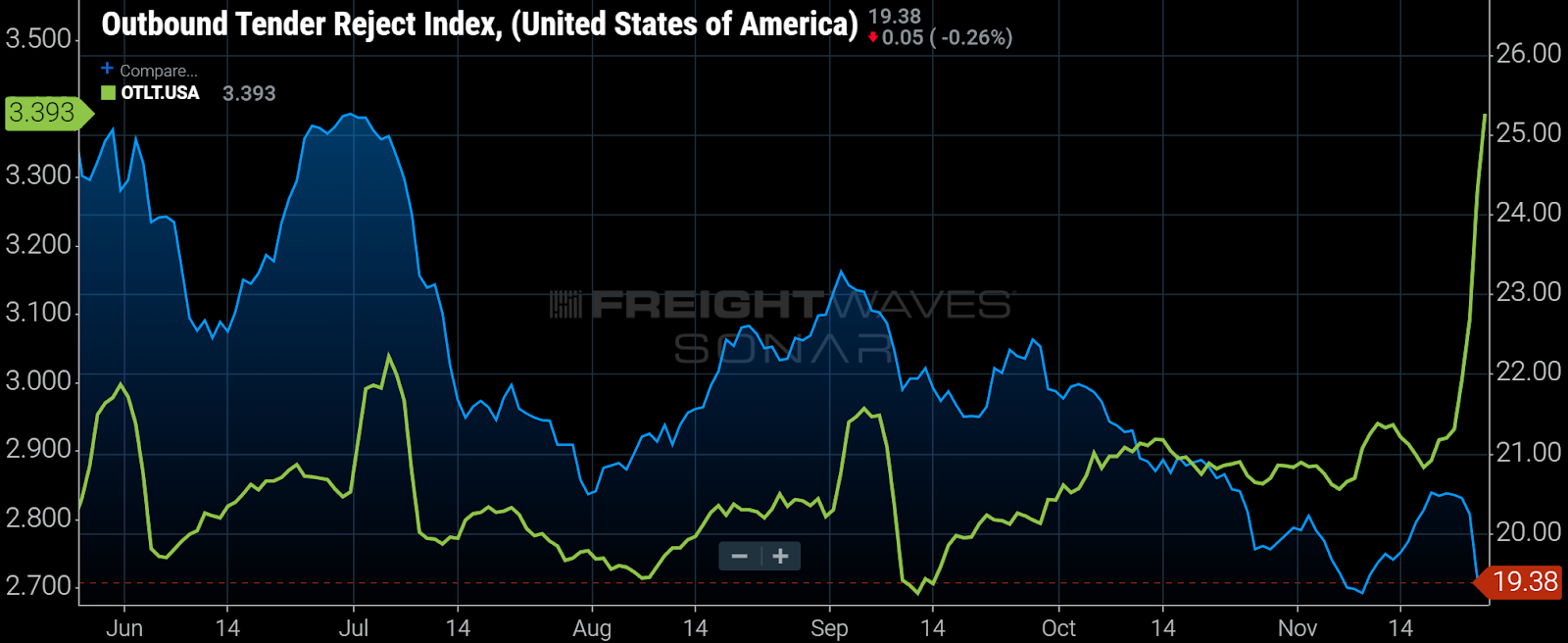

Most shippers are waiting until after the holiday weekend to move their loads. Accordingly, the national tender lead times (green line below) is at its highest level since last Christmas at 3.4 days. Meanwhile, the national tender rejection rate is near the low end of the past year’s range, indicating that shippers are finding truckload capacity more attainable than they did in recent months.

Out of fear of weight gain, many consumers eschew pasta, perhaps after taking their cue from Portlandia. The food industry has responded by producing pasta products made from alternative ingredients, such as cauliflower, chickpea, lupin, brown rice and brewer’s spent grain. This week, Food Business News provided a slideshow of those products. If they gain enough traction, traditional pasta supply chains could be disrupted. Alternative ingredients could also diversify pasta supply chains; in recent months, pasta availability was negatively impacted by a drought that affected the output of durum wheat in Canada which has contributed to higher pasta prices.

Impossible Foods raised approximately $500 million in its most recent funding round to bring its total funding since its 2011 founding to $2 billion. In previous editions of The Stockout, I discussed the recent results of Impossible’s competitor, Beyond Meat, and those disappointing results caused some analysts to question the future of plant-based meat products. Some analysts speculated that the number of consumers interested in plant-based meat alternatives was overestimated while others questioned whether the market had become oversaturated.

However, the latest results posted by Impossible’s competitors does not appear to be impairing the company’s ability to raise capital. Impossible has perhaps the best brand in the plant-based space, and its new products include plant-based alternatives for sausage, chicken nuggets, pork and meatballs.

JBS is investing $100 million to diversify into cultured meat. JBS reached an agreement to acquire BioTech Foods. I consider this to be part of a larger trend of the largest traditional food companies starting to hedge against changing food consumption patterns by investing in alternative foods. Another example is Tyson, which has started producing plant-based alternative meat products.

Finally, as I highlighted in earlier newsletters, here’s something for your calendar: I host the next quarterly The Stockout webinar on Dec. 6 at 2 p.m. ET. Here’s the link to register. Last quarter, there was a great turnout, and the discussion was enhanced by the many participants who asked thoughtful and pertinent questions. My hope for the upcoming webinar is the same.

To sign up for The Stockout, a free newsletter focused on CPG supply chains, please click here.