Smucker highlights sticky prices

With the prices of many commodities and unprocessed foods coming down, it’s natural to wonder whether CPGs would respond by reducing prices to compete for volume. In response to an analyst’s question on Tuesday’s earnings call, Mark Smucker, CEO of the J.M. Smucker Co., said that in general, he is not seeing price reductions in the packaged foods industry. The general lack of elasticity in CPG explains why — for instance, Smucker’s comparable net sales grew 6.5% in the most recent quarter despite a 4% price increase with a 2.5% sales boost from volume and mix.

Coffee futures are at their lowest levels since mid-2021, and that is being partially passed through to consumers. The price relief in that category is an exception to most other CPG items. (Chart: Barchart.com Inc.)

Packaged coffee is one exception where prices are more of a pass-through of commodity costs than other packaged consumables that require more processing. The executive noted that his company’s costs remain inflationary in total and the company is now fully offsetting cost inflation through price increases — that was reflected by the company increasing its gross profit margin guidance to the high end of its prior range (from 36.5%-37% to about 37%). Smucker, and most other CPGs, endured severe margin pressure during the pandemic and the period of heightened inflation that started in early 2021, and retail prices have finally risen to the point where inflation is being offset relative to the year-ago period.

Instacart prospectus touts benefits of targeted online advertising

Twelve percent of grocery sales now come from e-commerce, a quadrupling in share since before the pandemic and a trend that appears sticky as consumers become addicted to the convenience. So far, CPG companies have migrated about 25% of their advertising spending online, which suggests there is considerable room for growth in the space.

In addition to providing material required by the Securities and Exchange Commission for prospective initial public offering investors (such as showing that Instacart was profitable in 2022 and in the first half of 2023), Instacart’s prospectus published Friday highlights why CPG companies may want to advertise with the company. According to the grocery e-commerce enabler, CPG companies typically see a 15% increase in sales on the platform after using targeted advertisements, with some experiencing boosts twice that large. Pepsi is investing $175 million in Instacart as part of a private placement. Other major CPG brands that advertise on the platform include Nestle and Campbell’s, while emerging clients include lesser-known Banza, Whisps and Chloe’s Fruit Pops.

Going forward, Instacart says it plans to grow advertising dollars with emerging brands and nonfood categories that have higher advertising budgets, such as household products, pet items and personal care. In total, 5,500 brands have advertised on the platform for services that include display ads, sponsored products, brand pages, coupons and even options to buy in bulk at discounted prices (limited to items that Instacart is confident will be in stock).

I recommend this article from Winsight Grocery Business, which highlights risks to investing in the offering.

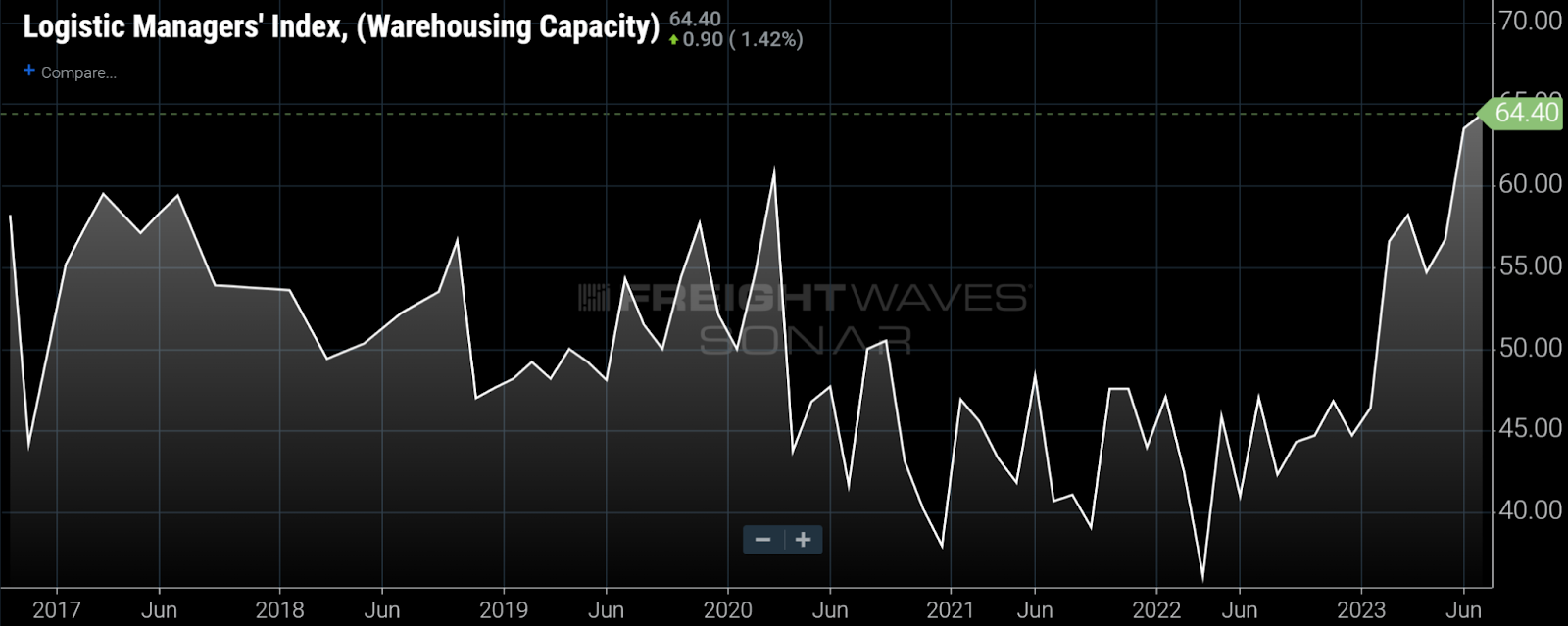

Warehousing capacity remains tight in many locations

(Chart: SONAR)

On this week’s The Stockout show, I interviewed Joe Oliaro, chief real estate officer at Wagner Logistics. Wagner Logistics is heavily involved in warehousing and works on behalf of manufacturers in a wide range of industries, including CPG and automotive. While many industry players have speculated that the extremely tight market for warehousing space during the pandemic would give rise to an overbuilding of warehouses, sharp increases in interest rates and building material prices have kept the warehousing market tight in many locations, such as California’s Inland Empire. Meanwhile, shippers’ perceptions of their own inventory levels are mixed: Some are satisfied while others say their inventories remain elevated.

Warehouses are being automated at a breakneck pace, which, for Wagner, has led to incredible improvement in picking efficiency. Still, not all processes can be automated, and the availability of needed warehouse workers remains tight, as it has always been. Wagner has been able to fill in the gaps with some creative solutions, such as leveraging the gig economy for part-time forklift operators after a certain amount of vetting.

See the full interview here.

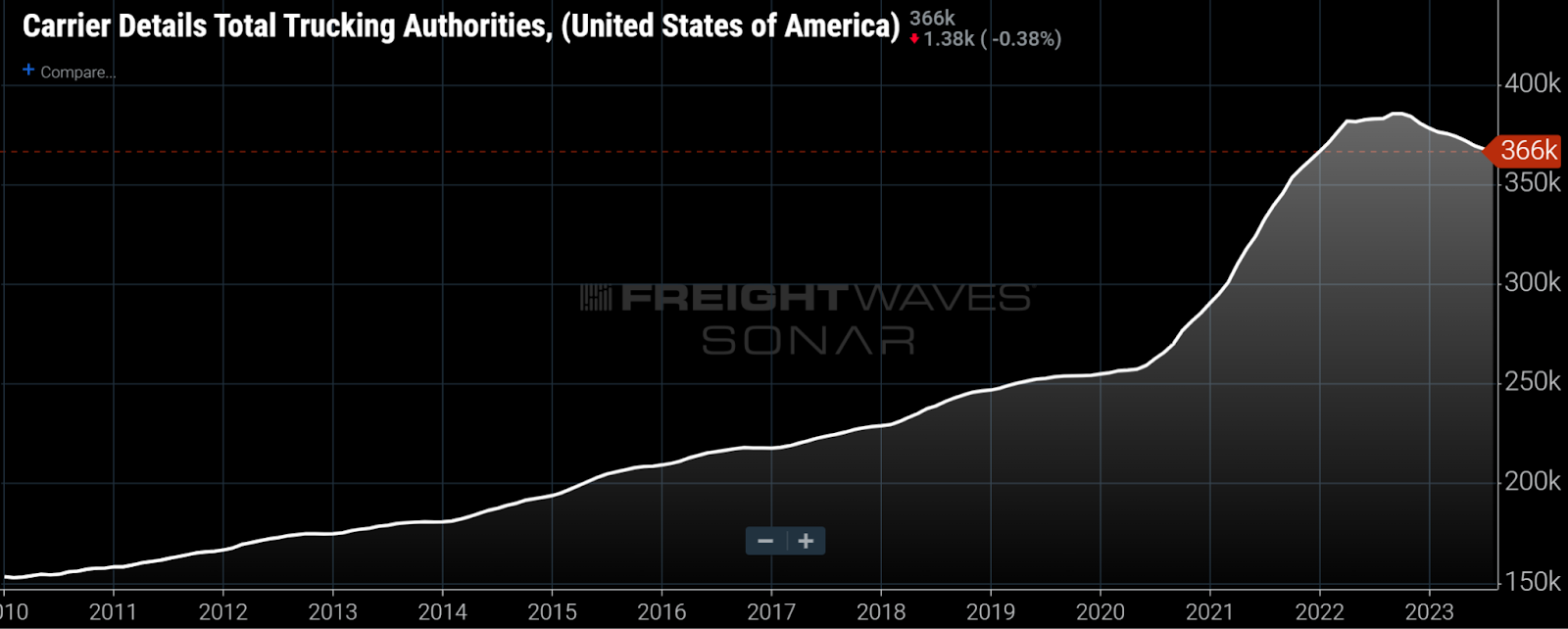

New SONAR data highlights excess truck capacity

Earlier this week, FreightWaves SONAR announced three new data sets on truck capacity in partnership with Carrier Details: Net Revocations (CDNR.USA), Total Authorities (CDTTA.USA) and Net Changes in Authorities (CDNCA.USA). Our article on the release can be found here.

My favorite is the above chart on Total Trucking Authorities in the U.S. While a count of trucking authorities doesn’t tell you how many trucks are in the fleets, most of the new entrants were very small fleets or even previous company drivers who recently got their operating authority. In short, the chart suggests that lots of capacity still needs to come out of the market for it to be a healthy market for small carriers that rely on the spot market.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, click here.