Saia’s quarterly earnings have sent the company’s already high-flying stock into the stratosphere.

Before the LTL carrier announced its earnings Thursday morning, Saia (NASDAQ: SAIA) was already sitting on a 52-week gain of close to 100%. After closing Wednesday at just under $274, its strong earnings report for the third quarter sent it up $22.26, or roughly 8%, to a price of $296.15 at 11:30 a.m. Thursday. For the day, the high price was just over $300. The 52-week high is $316.98 and the Thursday gains put the 52-week increase at about 110%.

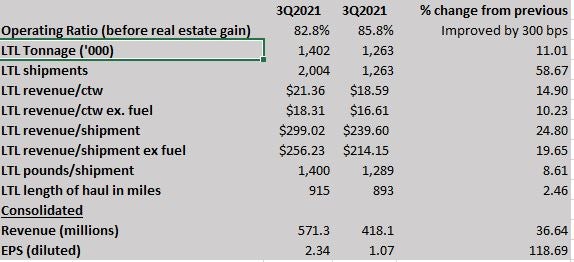

The latest surge in its stock price comes as Saia reported a 28% increase in revenue from the third quarter of last year, a 500 basis points improvement in its operating ratio, an 84.5% increase in its adjusted operating income and a big improvement in its yield.

The improvement in Saia’s operating ratio brought the OR down to 83.5% from 88.5%. Revenue per hundredweight — the figure for LTL yield, considered the most significant benchmark besides OR — rose 14.9% compared to the third quarter of last year.

And reflecting higher rates, revenue per shipment climbed 24.8% to $299.

It was that figure that led the transportation team at Deutsche Bank headed by Amit Mehrotra, in an email to clients titled “Taking our breath away,” to note that its bullish view on Saia has been driven in part by what it said was “the company’s opportunity to close the gap on revenue per shipment with peers, which we’ve said has the potential to quadruple earnings power over the midterm.”

Deutsche also noted that the company’s yield increase exceeded the gain in weight per shipment of a little less than 9%. As Deutsche noted, increases in weight per shipment dilute yield. “This implies robust price/mix, which we believe has been a hallmark of SAIA’s strategy and we think is still in its early innings.”

CEO Frederick Holzgrefe, on the company’s earnings call with analysts, discussed the challenges of managing an LTL network and the ever-present push to get the best mix of freight and revenue. There is no perfect definition for “mix,” but LTL carriers always seek what their analysis says is the preferred combination of rates, weight and mileage.

For example, Holzgrefe said, “if we have a category of freight that is excessive in length, that can be difficult for us to handle. You have to manage that.”

That sort of freight needs to be identified and a rate needs to be established that covers that cost, the CEO said. “We absolutely have to get paid for providing that capacity.”

And if Saia can’t get paid, Holzgrefe said, “you decide you’re not in that part of the market, and we’re comfortable doing that.”

On the expenses side of the ledger, salaries, wages and benefits at Saia climbed to $277 million from $252 million last year. That line item was $266.7 million in the second quarter. Purchased transportation rose to $72.1 million from $40 million a year ago; in the second quarter, it was $62.4 million.

In a report issued after the earnings were released, KeyBank’s Todd Fowler said the salaries and wages line item was 45% of expenses, compared to KeyBank’s estimate that it would come in at 47.6%. As for purchased transportation, the 11.7% share of expenses was 100 bps more than the KeyBank estimate, “likely reflecting a modest shift between company-handled linehaul and third parties.”

In the company’s prepared statement releasing the earnings, Holzgrefe said the company’s revenue, operating income, net income and earnings per share were all records for any quarter in Saia’s history.

According to Seeking Alpha, the non-GAAP EPS of $2.86 was 51 cents better than consensus, while the GAAP DPS of $2.98 was 63 cents better than consensus. Revenue of $616.2 million was almost $40 million better than consensus, according to Seeking Alpha.

Looking ahead, Saia CFO Douglas Col said on the earnings call with analysts that a 150 bps deterioration in OR in the fourth quarter is likely, as that level of decline would be in line with traditional fourth-quarter weakening.

But Holzgrefe said Saia’s target remains a 150 to 200 bps improvement in OR annually, “and we certainly now have the opportunity to push that to the top end of the range.”

Other notable discussions from the earnings call:

- Holzgrefe said the company expects to be at 176 terminals by the end of the year and will add 10 to 15 terminals in 2022. He pointed out that as terminals are added, the cost structure of opening a terminal gets softer as expertise is gained. That can be seen in the company’s Northeast operations, an expansion that Saia began in 2017. Holzgrefe said the improved cost basis for opening terminals there has enabled that region’s OR to be driven to less than 90%.

- Reacting to an analyst question about ancillary charges on top of the baseline LTL rates, Holzgrefe said about 20% of the revenue in each bill is a good estimate of the impact of accessorial charges. And the strong market is leading to those charges going up. “A charge you might have waived in the past is not the market these days,” he said. “And next year, it could be that we need to raise the charges to get them to market level.”

- Col said Saia implemented two pay raises this year, one as recently as August, but added he does not foresee two increases in 2022.

More articles by John Kingston

Another day, another record-breaking earnings report, this time at Saia

Drilling Deep: Saia, ODFL and KC Southern on Mehrotra’s mind

Saia execs not concerned about purchased transportation spend increase