The highlights from Friday’s SONAR reports. For more information on SONAR — the fastest freight-forecasting platform in the industry — or to request a demo, click here. Also, be sure to check out the latest SONAR update, TRAC — the freshest spot rate data in the industry.

Lanes to watch

By Zach Strickland, director, Freight Market Intelligence

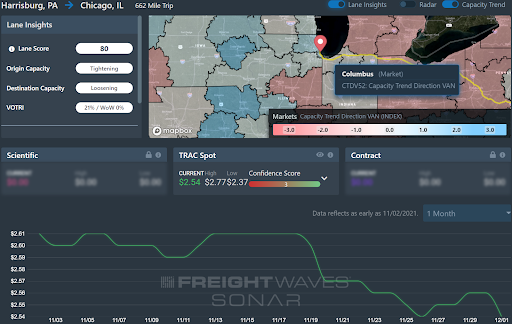

HARRISBURG (Pennsylvania) to CHICAGO

Overview: Brokers should lower their bids in light of declining dry van spot rates.

Highlights

- Typically a tighter lane than most, the van tender rejection rate in the Harrisburg to Chicago lane has been on a downward trajectory this fall from over 30% to 20.6% currently, now within 100 basis points of the national van tender rejection rate of 19.7%.

- The dry van spot rate in SONAR Market Dashboard, which reflects what brokers and 3PLs are currently paying for dry van truckload capacity, has declined in the past month from $2.61/mile, including fuel, to $2.54/mile, including fuel.

- The most recent door-to-door intermodal spot rate from nearby Chambersburg to Chicago is $2.05, including fuel, which places it 19% below the average dry van truckload rate shown in Market Dashboard.

What does this mean for you?

Brokers: Lower your bids in the lane to reflect the loosening capacity and falling dry van spot rates. When bidding for capacity, keep in mind that the spot rates paid by brokers shown in SONAR Market Dashboard for average, high (67th percentile), and low (33rd percentile) rates are $2.54/mile. $2.77/mile and $2.37/mile, respectively. All rates include fuel surcharges.

Carriers: Likely reflecting shifts in capacity following Thanksgiving, the latest SONAR stats show that Chicago is a less desirable destination for carriers than it had been in recent weeks. The Chicago outbound tender rejection rate declined from 20% to 18% and the Chicago Van Headhaul Index declined from 55 to 17 as outbound Chicago demand dropped faster than inbound Chicago demand.

Shippers: With this lane showing signs of loosening, shippers have better options than they often do. Shippers may want to explore using domestic rail intermodal for shipments that are less time-sensitive given current rates. For shipments that are more time-sensitive, keep lead times extended past the 3.2-day average for all outbound Harrisburg van loads to help secure capacity.

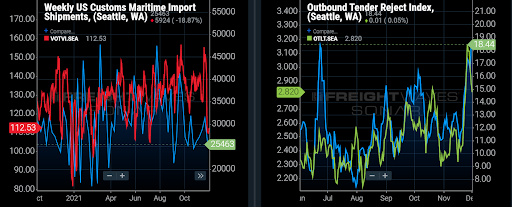

SEATTLE to CHICAGO

Overview: Rejections already up 320 bps week-over-week, as Seattle outbound volumes are positioned to retest their all time highs before the end of 2021.

Highlights

- Seattle outbound tender volumes are down 18% w/w, signaling that demand for outbound capacity is still down significantly from the lead up to “Black Friday.”

- The Headhaul Index in Seattle is up 50% w/w, signaling that capacity is likely to tighten further in the coming days.

- Seattle outbound tender rejections are up 320 bps w/w, signaling that capacity is likely already slightly tightening as a result of the rise in outbound volumes.

What does this mean for you?

Brokers: Even though Seattle outbound tender volumes have decreased 18% w/w, they are expected to rebound in the coming week. With the 50% increase in the Headhaul Index, and outbound tender rejections up 320 bps w/w, the major imbalance between inbound and outbound volumes is still likely to drive rejections even higher.

Carriers: Stay firm on your rates on outbound Seattle lanes as the decrease of 18% w/w in outbound tender volumes is likely to be short lived. Outbound volumes for dry vans could even break a new record before the end of the year, and if that is to happen, we can expect that capacity will tighten significantly since the 50% increase w/w in the Headhaul Index and 320 bps increase in outbound rejections are already signaling that capacity is highly likely to tighten further in the days ahead.

Shippers: Your shipper cohorts in Seattle are averaging 2.8 days in tender lead times, which are down from 3.1 days last week. Even though they have experienced a slight decrease w/w, with outbound tender volumes likely to move closer to an all time high in the coming weeks, it would be wise to keep your tender lead times between 3 and 4 days through the next couple of weeks to ensure you are able to secure capacity in the market.

ELIZABETH (New Jersey) to COLUMBUS (Ohio)

Overview: Elizabeth rejection rates spiking after the holiday period.

Highlights

- Elizabeth’s outbound rejection rate has jumped from 14% to near 18% over the past week.

- Have not moved much over the past month, bouncing between 23 and 25%.

- Columbus’ outbound rejection rates have increased 3 percentage points to 23.5% over the past three days.

What does this mean for you?

Brokers: Pad margins by a few cents per mile when uncertain in this lane. Rejection rates spiking out of a market are signs of strong disruption, especially in a larger market. This should be a relatively favorable lane for a carrier in terms of direction and reload potential, but traffic congestion makes this a very inefficient mileage at times.

Carriers: Watch for increasing spot market activity in this lane where spot rates are running just over $1400 per load on average. Divert capacity accordingly. Columbus activity is increasing, meaning reload potential should be on the rise as well.

Shippers: Consider increasing rates in this lane if your compliance is below 75%. Check in with your carriers for any loads scheduled for pickup out of Elizabeth today.

Watch: Carrier Update

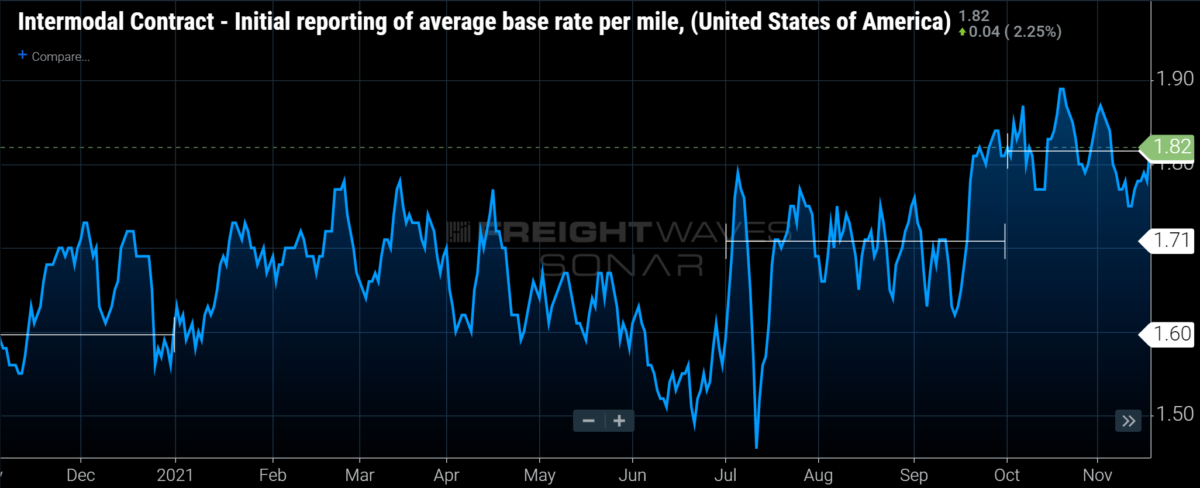

Quick look: Intermodal contract rates

By Mike Baudendistel, SONAR Market Expert

Intermodal contract rates took another 6% step up quarter-over-quarter to an average base rate (i.e., does not include fuel surcharges) of $1.82 a mile so far in the fourth quarter of 2021 (recognizing that there is nearly one month remaining) from $1.71 a mile in the third quarter 2021.

Relative to the fourth quarter of 2020, SONAR intermodal contract rates are 14% higher, reflecting the double-digit rate increases in intermodal contract rates that took hold as they were repriced earlier this year.

This entry appeared in Mike Baudendistel’s newsletter, The Stockout. To subscribe, click here.

Watch: Shipper Update

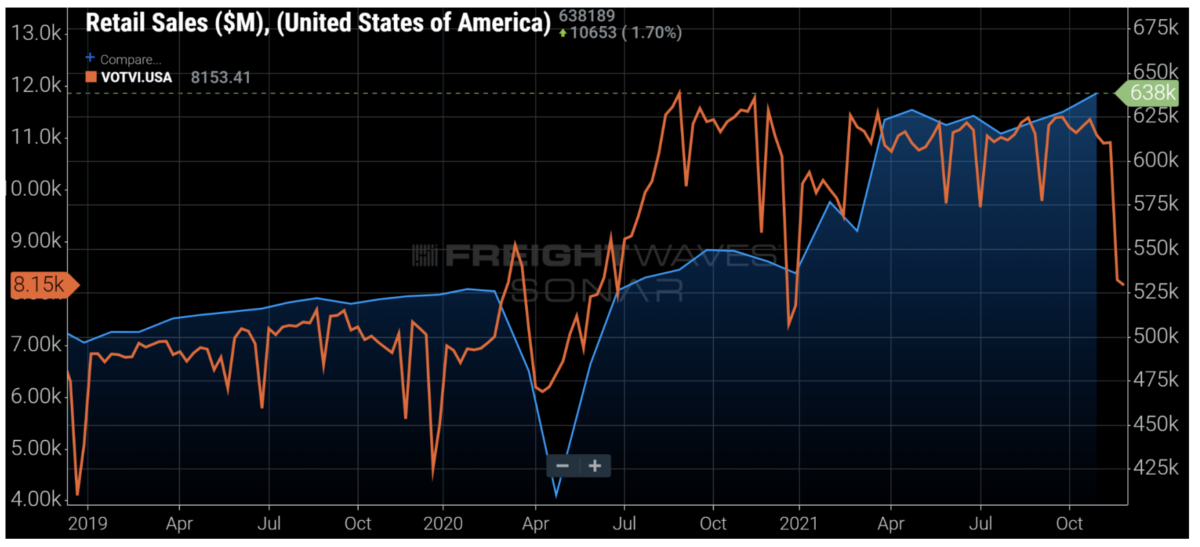

November 2021: Consumer conditions and retail

Inflation is the biggest headwind facing consumers. Consumer sentiment/confidence indices are reflecting growing concern over the increasing inflationary pressures.

However, the actions of consumers have yet to ease. The jobs market is favoring employees in a big way and Americans are still quitting their jobs at a record rate with an overwhelming amount of openings to choose from.

Diminished demand is coming, but at a much slower pace than what many were expecting. Consumer stamina is holding up so far this peak season as many Americans got an earlier start to holiday shopping this year. Inflationary pressures will set in for consumers in 2022.

The savings rate is back to pre-pandemic levels although revolving credit is still low, signalling that Americans are not over-encumbered at the moment, but big ticket items are starting to build up with expensive used car prices and housing trends.

The diminished demand expected in 2022 will ease slowly without hitting recessionary levels – much like manufacturing.

This analysis originally appeared in the SONAR Monthly Market Update. For more information and to download the complete report, click here.

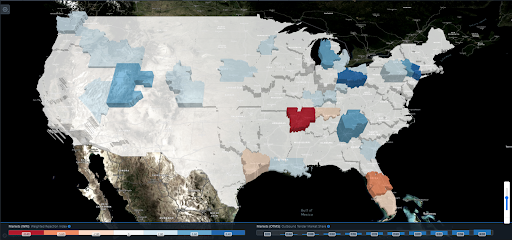

Focus on … Weighted Rejection Index

By Zach Strickland

The weighted tender rejection index map shows strong increases in rejection rates out of three of the nation’s largest outbound markets.

Elizabeth, Columbus and Atlanta all have had big jumps in outbound rejection rates over the past week, indicating the increased potential for higher spot volumes and rates out of these markets.

The Weighted Rejection Index (WRI) multiplies weekly change in outbound rejection rates by outbound market share value.

This index helps identify which markets in the U.S. are having the most significant impact on weekly fluctuations in national capacity.