The highlight reel from Tuesday’s SONAR reports. For more information on SONAR — the fastest freight-forecasting platform in the industry — or to request a demo, click here.

Lanes to watch

By Zach Strickland, director, Freight Market Intelligence

LOS ANGELES to DALLAS

Overview: Dry van carriers average $3.66 all-in rpm on the LAX–DAL lane as freight volumes increase.

Highlights:

- Freight volumes increase to 1195 index points on the LAX – DAL lane, pushing the average carrier rate up to $3.66 all-in rpm last week.

- Dallas’ dry van Headhaul score declines, but remains elevated at 104.35 as market conditions soften.

- Dallas shippers increase tender lead times to 2.91 days, indicating that shippers are feeling pressure from changing market conditions.

What does this mean for you?

Brokers: The Los Angeles market is arguably the tightest market in the nation as outbound rates continue to hit record highs. Brokers should search the spot market for dry van loads that run across the LAX – DAL lane, helping shippers secure capacity for their loads. Increase your bids since carrier costs continue to trend upward. Carrier rates for on-demand capacity will be extremely expensive so keep downward pressure on the rates you receive to help create margins on these loads.

Carriers: Dry van carriers averaged $3.66 all-in rpm on the LAX – DAL lane last week, and capacity continues to be an issue in the Los Angeles market. Carriers with excess capacity in the Los Angeles market should search the spot market for loads that deliver into the Dallas market, but increase your rates as shippers struggle for capacity. The Dallas market has softened, but shippers have increased tender lead times to almost 3 days as they are starting to feel pressure from shifts in market conditions.

Shippers: Keep dry van tender lead times extended, and monitor the Headhaul index, rejection rates and freight volumes. Market conditions have softened over the past week in Dallas, but a Headhaul score of 104 indicates that market conditions are still extremely tight. As we enter the holiday season, spot rates could climb back up very quickly, enticing carriers to reject their contracted freight for higher paying freight on the spot market.

SAN FRANCISCO to DALLAS

Overview: Volumes up 11% week-over-week (w/w), causing a 28% increase in the Headhaul Index.

Highlights

- San Francisco outbound tender volumes are up 11%, signaling that demand for capacity is growing, putting upward pressure on rates.

- The Headhaul Index has increased 28% w/w, and that is likely to grow as import volumes shift over into the truckload market.

- San Francisco outbound tender rejections are relatively flat w/w, but could increase in the days ahead as the imbalance in volumes grows.

What does this mean for you?

Brokers: It is important to notice the growing imbalance between outbound volumes and inbound volumes via the Headhaul Index, which is up 28% w/w. While import volumes have been limited due to the massive congestion backlog of vessels caught up in the SoCal port traffic jam, there is still likely to be a significant amount of volume being transitioned over into the truckload market. These volumes are as time sensitive as ever, and will likely cause capacity to tighten significantly this month.

Carriers: Stay firm on your rates as the increase of over 28% in the Headhaul Index w/w is likely to shift pricing power further into your favor. With import volumes expected to increase from vessels finally getting free of the traffic jam in LAX/LGB, it is likely that these new volumes will only add to the pressure on capacity and rates as we get closer to “Black Friday” and the peak of retail buying season for the holidays.

Shippers: Your shipper cohorts in San Francisco are averaging 3.1 days in tender lead times, but this may not be enough lead time to sufficiently cover your freight in the weeks ahead. There is likely a major amount of pent-up truckload demand from containers trying to get trans-loaded, so be aware that volumes could see a major boost during the next few weeks.

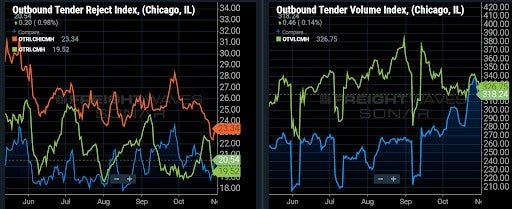

CHICAGO to COLUMBUS (Ohio)

Overview: Chicago demand hits highest level of the year.

Highlights

- Chicago’s tender volumes have jumped nearly 15% month-over-month, which is starting to put increased pressure on capacity in the market.

- Rejection rates to Columbus hit a floor late last week around 22.2% but have bounced back over 23%.

- Columbus’ outbound rejection rates have recovered after spiking above 22% a week and a half ago. Outbound demand remains consistent over the past month with low volatility.

What does this mean for you?

Brokers: Keep an eye on Chicago capacity as most of the outbound demand growth has come from loads moving more than 450 miles. Carriers compliance has improved over the past month, but increasing demand will limit the recovery. Expect upward pressure on rates to persist.

Carriers: Accept more loads into the Chicago market with demand on the rise. Columbus is prone to sharp changes in capacity conditions, but appears to be stabilizing for now with rejection rates falling below the national average.

Shippers: Keep lead times between three and seven days if possible in this lane. Rate increases may have improved compliance in this lane, but increasing demand pressure will keep capacity at-risk throughout the week.

Shipper Update

Focus on … Dry Van Index

By Zach Strickland

The national average for dry van outbound tender rejection rates rebounded slightly over the weekend to 19.35%, stopping the downward trend that began in early September.

Freight volumes have declined over the past few days, but remain elevated at 11,329.60 index points, indicating that the demand for dry van equipment remains elevated.

Shippers in the Cape Girardeau, Cedar Rapids, Des Moines, Omaha, Sioux Falls and Dubuque markets are struggling with rejection rates over 40%, and rejection rates are over 25% in the Memphis, Rock Island, Jefferson City, Augusta, Duluth, Evansville, Mobile, Birmingham, Grand Rapids, Nashville, Montgomery, Denver, Louisville, and Tifton markets as capacity shifts just before the holiday season.

Carriers will find the most opportunities for dry van freight in the Ontario, Atlanta, Harrisburg, Dallas, Elizabeth, Los Angeles, Allentown, Joliet, Columbus, Indianapolis, Houston, Charlotte and Chicago markets, which are the largest dry van markets by volume in the nation.

Carrier Update

Spot rates in California

By Mike Baudendistel, SONAR Market Expert

Spot rates to move produce from central California have been highly inflationary.

In traditional farming methods, lettuce requires very specific growing conditions and must be hauled in temperature-controlled trailers. The limited areas where it can grow include the Salinas Valley (included as part of the San Francisco metro area in SONAR) in the spring and summer and Yuma, Arizona (part of the Phoenix market in SONAR data).

The chart below shows that, in the past five years, the all-inclusive truckload costs to move produce from central California to Chicago have been as low as $4,000 a load but reached a high of $8,550 this year. With vertical farming, that cost and volatility could be reduced by growing lettuce closer to consumption centers.

Diesel wholesale and retail prices

TravelCenters of America’s total revenue figures are not a good indicator of how the company is doing financially, given that it is heavily influenced by the cost of fuel. The company’s fuel revenue was up almost 80% compared to the third quarter a year ago, not surprising given that the average retail diesel price, according to the Department of Energy, was about 90 cents more in the third quarter of this year than in Q3 2020.

But the company made more on its fuel sales, with the fuel gross margin rising to $106 million from $80 million a year ago. Nonfuel revenues also were up, rising 7.8%.

However, the market swings were beneficial to TA, as its fuel gross margin was 18.1 cents a gallon, compared to 14.4 cents a gallon in the third quarter of last year. This was accomplished even as the margin between diesel wholesale and retail prices, as seen in the FUELS.USA data series in SONAR, showed a weakening number as the quarter wore on.

Maritime import shipments at Port of LA

Cargo sitting on marine terminals over nine days amounts to 47% of all containers in the Los Angeles port, or 38,000 shipping boxes. About 36% of all cargo has been in terminals one to four days, but it represents 52% of the cargo exiting through the gate, demonstrating that the longer cargo sits the less likely it is to be retrieved.

Before the pandemic-led import surge that began last year, containers for local delivery remained on container terminals under four days, on average, while containers designated for trains dwelled less than two days.