The highlights from Friday’s SONAR reports are below. For more information on SONAR — the fastest freight-forecasting platform in the industry — or to request a demo, click here. Also, be sure to check out the latest SONAR update, TRAC — the freshest spot rate data in the industry.

Market watch for Sept. 23:

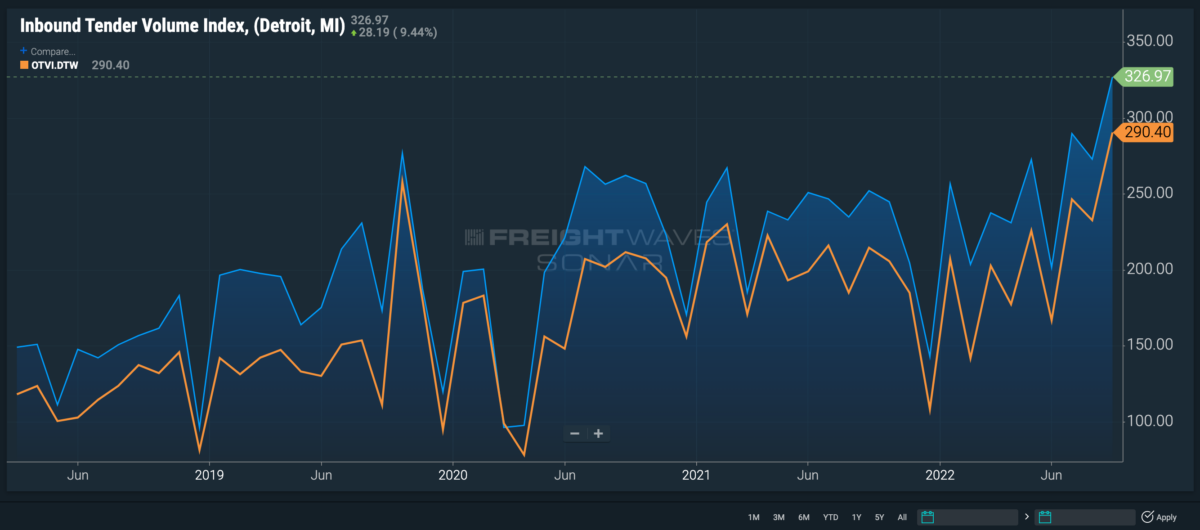

Detroit

Volumes in Detroit are continuing to roar back up to record highs.

The Outbound Tender Volume Index for Detroit is up 10.5% since Wednesday to 290.4 leading into the weekend. This marks the highest value the index has seen since FreightWaves began tracking the market in 2018.

Inbound tender volumes are also seeing a significant increase heading into the weekend. The Inbound Tender Volume Index is up 28 points, or 9.5%, in the past two days to also reach its highest value since 2018.

Inbound truckload volumes currently exceed outbound levels by 12.7%, pushing the Headhaul Index ever so slightly downward 1% to -36.5.

Given the amount of inbound capacity flooding the market, outbound tender rejection rates are down 118 basis points to 3.2%, their lowest level since 2020.

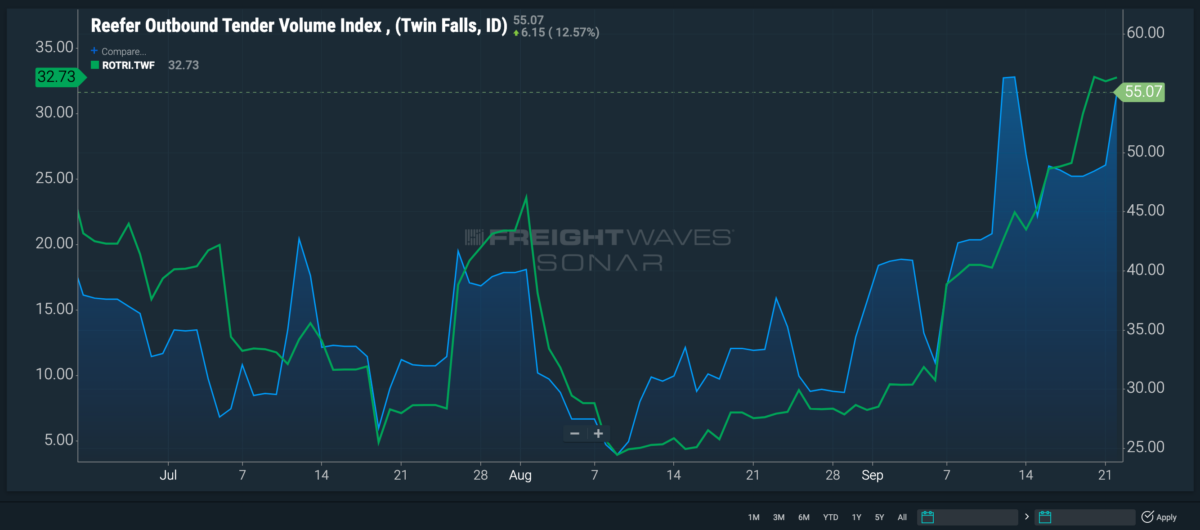

Twin Falls, Idaho

Twin Falls, Idaho, known as the Silicon Valley of food, has seen refrigerated volumes trend steadily upward to reach a six-month high.

The Reefer Outbound Tender Volume Index for Twin Falls is up 70.8% since Sept. 6 to 55 — the highest value seen since February.

Seasonally ripe fruit such as apples and peaches are in season from late August through October.

“September is the best month for peaches in Idaho,” says the co-owner of Kelley’s Canyon Orchard, Robin Kelley, in an interview with the local CBS station.

The consistent surge in volume has also launched rejection rates to six-month highs, tightening capacity and sending the Reefer Outbound Tender Reject Index up 2,300 bps to a colossal 32.7%.

NTI as a point of reference

The National Truckload Index is a daily look at how spot rates in specific lanes hold up in comparison to the national average, giving carriers and brokers an idea of which lanes to gravitate toward or avoid.

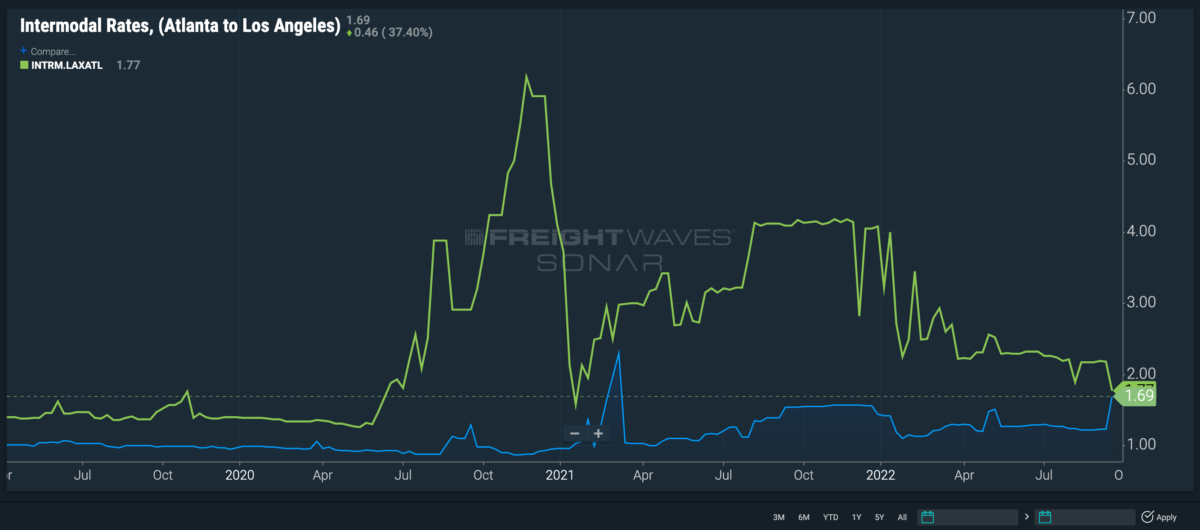

Intermodal rates

Rail protests may be averted — for now — but the repercussions of it all are being felt in spot rates.

The average weekly intermodal spot rates for a 53-foot dry van from Atlanta to Los Angeles are up 46 cents from last week to $1.69 a mile — the highest they have been since FreightWaves began tracking the rates in 2013.

Meanwhile, the weekly average from Los Angeles back to Atlanta is down 41 cents in the same time period to $1.77 a mile. This is the thinnest disparity between these two spot rates since February 2021.

Regarding such a different change in rates, FreightWaves’ head of intermodal solutions, Mike Baudendistel, had this to say: “These rates moved to being a lot closer to parity than they typically are, particularly for the time of the year. The increase from Atlanta seems related to protecting capacity for contractual shippers moving loads out — we saw the same increase from Atlanta to Chicago.”

“The outbound LA spot rate weakness may be related to carriers less concerned about protecting capacity for contractual shippers on outbound LA loads than they typically are this time of year.”

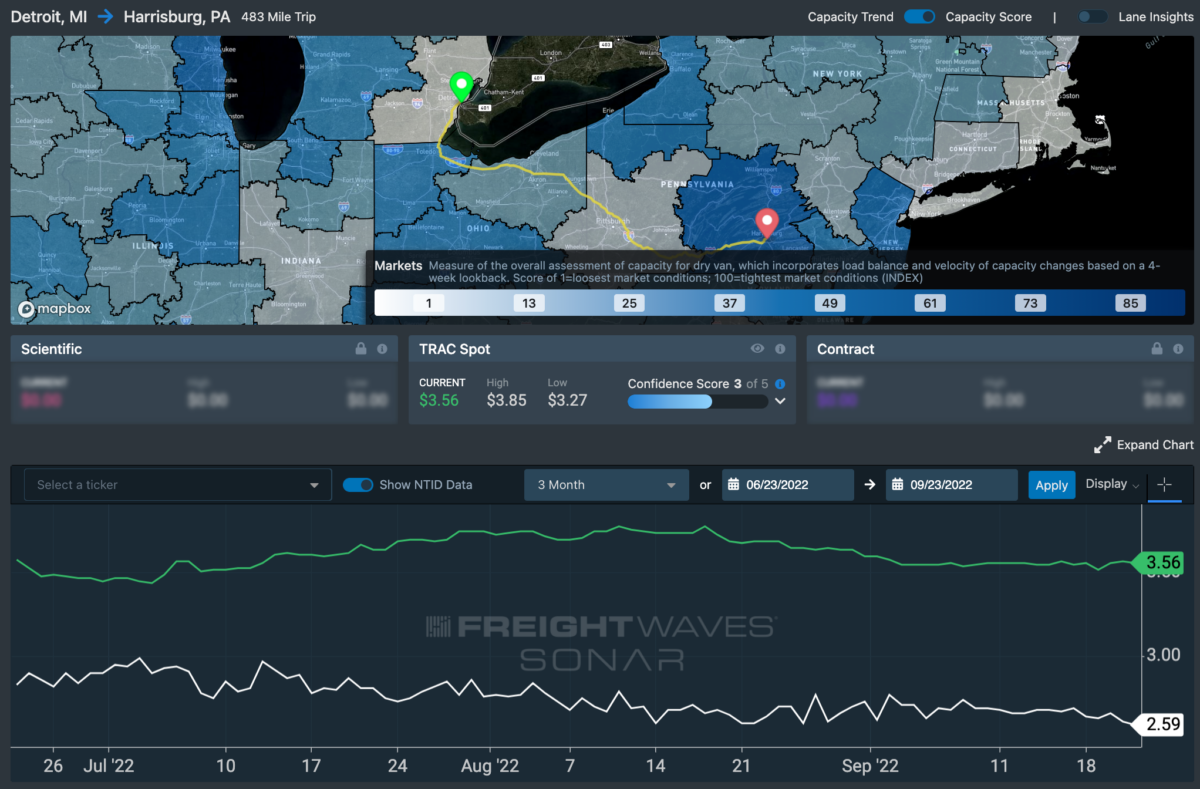

Lane to watch: Detroit to Harrisburg, Pennsylvania

Spot market rates from Detroit to Harrisburg have remained consistent for the past two months at or around their current value of $3.56 a mile — 98 cents above the national average.

A return trip, however, drops the rate considerably to $2.60 a mile. Even though rejections were trending down Thursday, in the past 24 hours they have ticked up 37 bps to 6.9%. It is also important to note that the return rates only have a confidence score of 1, providing a great amount of volatility.

Worst case, a trip from Harrisburg to Chicago is currently paying $2.30 a mile and with a confidence score of 3, providing significantly less volatility in rates being offered.