This week’s FreightWaves Supply Chain Pricing Power Index: 30 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 30 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 20 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is based on the following indicators:

Volumes hibernating during quiet season

Freight demand is sliding this week, with few sources of upward pressure bearing on volumes for the near future. Consumers’ appetite for discretionary spending has been usurped in favor of squirreling away income into personal savings. Given the record-high interest rates on credit cards, many consumers simply cannot afford to buy big-ticket items. Most worryingly, auto loan delinquencies are on the rise, which could lead to a wave of defaults and repossessions that would signal a total collapse of consumer demand.

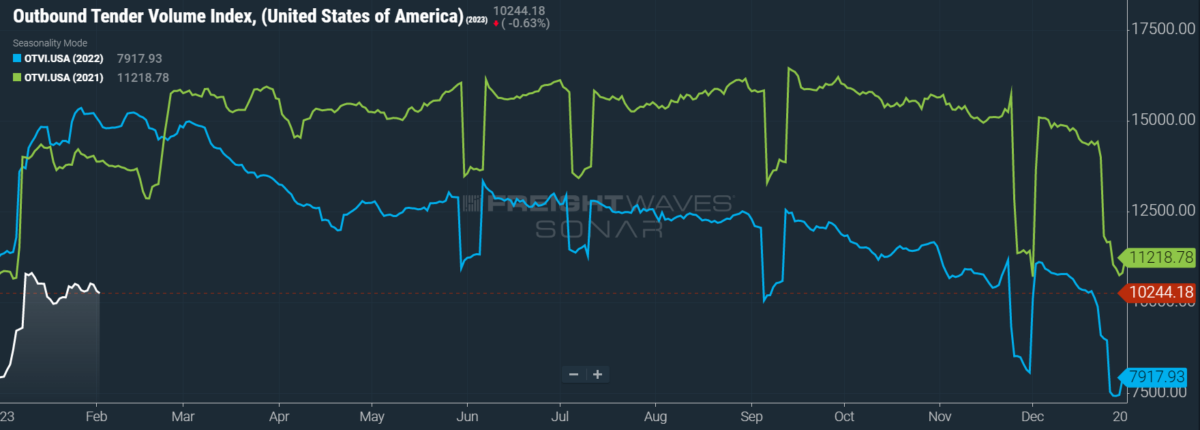

SONAR: OTVI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

This week, the Outbound Tender Volume Index (OTVI), which measures national freight demand by shippers’ request for capacity, fell 2.1% on a week-over-week (w/w) basis. On a year-over-year (y/y) basis, OTVI is down 30.1%, but such y/y comparisons can be colored by significant shifts in tender rejections. OTVI, which includes both accepted and rejected tenders, can be artificially inflated by an uptick in the Outbound Tender Reject Index (OTRI).

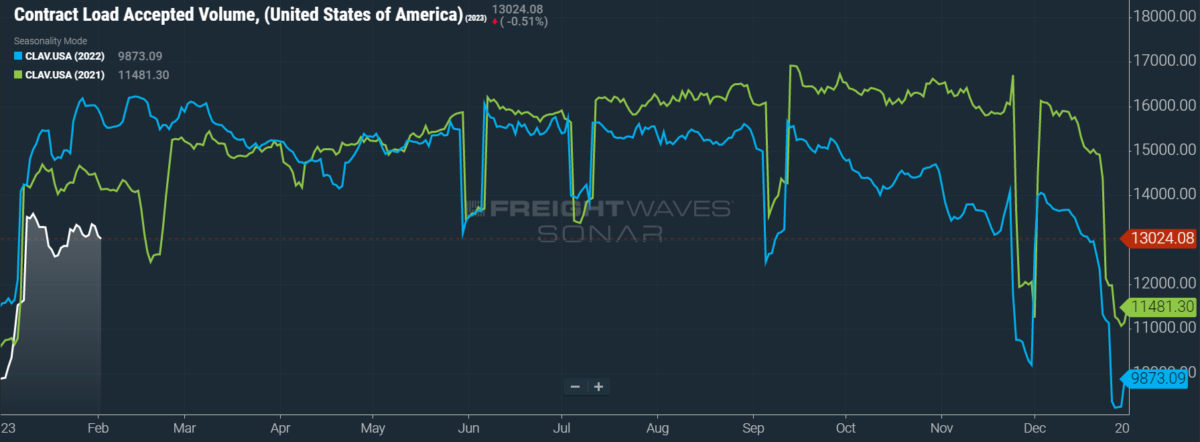

SONAR: CLAV.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Contract Load Accepted Volumes (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see a dip of 2% w/w as well as a fall of 17.5% y/y. This y/y difference confirms that actual cracks in freight demand — and not merely OTRI’s y/y decline — are driving OTVI lower.

On the heels of the Federal Open Market Committee’s (FOMC) latest meeting, at which it announced a slowdown in interest rate hikes, the economy is sending out mixed signals. On Wednesday, the FOMC raised interest rates by 25 basis points (bps) — a disruption to the string of 75 bps jumps seen in the back half of 2022 and a further reduction from December’s rise of 50 bps. Concerning the future direction of its economic intervention, the FOMC stands at a crossroads. Some officials are calling for dovishness, arguing further increases could compromise the Federal Reserve’s targeted “soft landing.” In support of their position, such doves cite the aforementioned slowdown in consumer spending and the collapse of existing home sales in 2022 — the latter of which reached its lowest level since 2014 in reaction to mortgage rates spiraling to a 20-year high.

But the opposing hawks have some data of their own. Take, for instance, January’s jobs report, which revealed that — far from the expected increase of 188,000 jobs over December — the month saw a staggering gain of 517,000 new positions on a seasonally adjusted basis. Those last five words might be the key phrase, however. Seasonal conditions for January have transformed to be quite favorable, with job growth last January negatively impacted by the surge of the COVID-19 omicron variant. Still, with the latest drop in unemployment rates from 3.6% to 3.4% taking it to levels not seen since 1969, the labor market does look extremely tight.

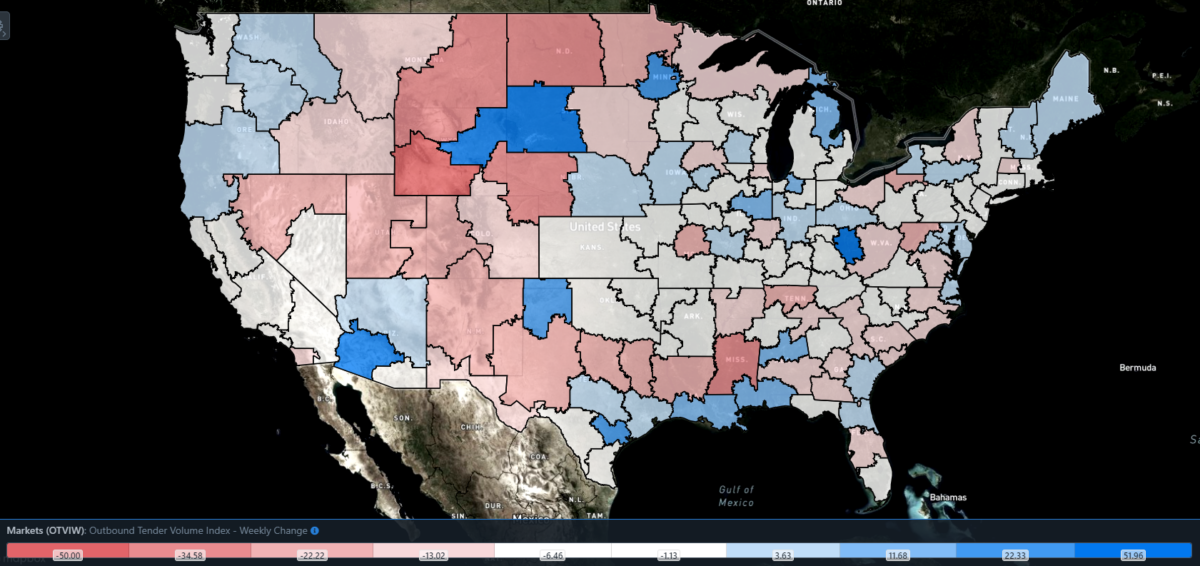

SONAR: Outbound Tender Volume Index – Weekly Change (OTVIW).

To learn more about FreightWaves SONAR, click here.

Of the 135 total markets, 47 reported weekly increases in tender volume as truckload markets settled into this year’s rhythm.

Freight demand is steadily rising in the Midwestern markets of Columbus, Ohio, and Indianapolis, seeing respective gains of 6.05% and 4.3% w/w. This news is a signal of health for future industrial demand, as the two markets occupy the manufacturing region of the Rust Belt. Still, there are a host of other signals that point to ailments in the sector, such as industrial production declining in December and manufacturers’ sentiment reaching abysmal lows in surveys conducted by the Fed.

By mode: Reefer volumes are shockingly weak at the moment, as the winter storms affecting Dallas (discussed below) should have driven no small surge in demand. The Reefer Outbound Tender Volume Index (ROTVI) is down 4.43% w/w. ROTVI is also down 32.6% y/y, but the gap between current reefer rejection rates and those of 2022 is vast. Accepted reefer volumes are actually down by a negligible 0.16% y/y.

Van volumes are middling, as the Van Outbound Tender Volume Index (VOTVI) is down 2% w/w. Softening retail demand from consumers, which has both seasonal as well as economic causes, is surely impacting the flow of freight, as is the dearth of maritime imports coming from China during the Lunar New Year celebrations. VOTVI is down 31% y/y, but as with reefers, van rejection rates have dropped considerably over the past year. Nevertheless, accepted van volumes have decreased 18.6% y/y.

Tender rejections depressed and depressing

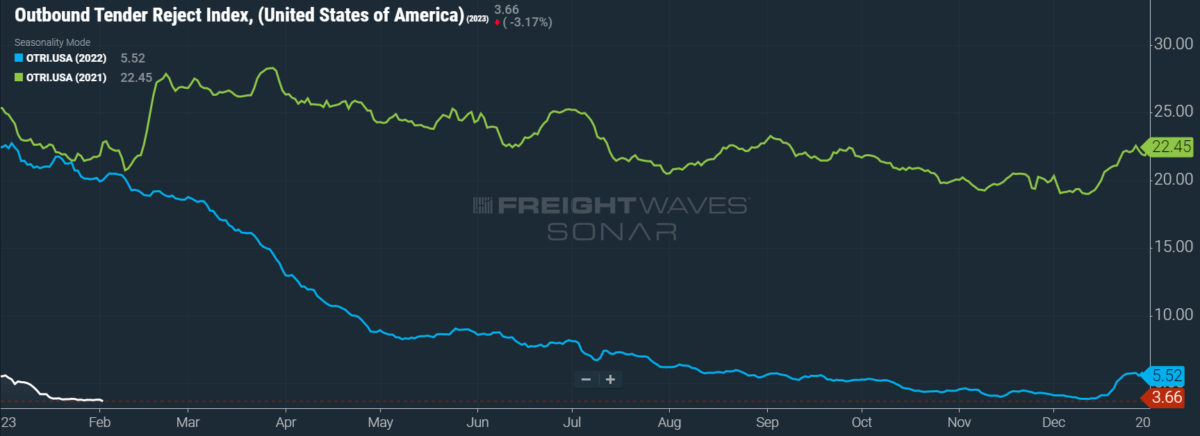

After shedding its holiday gains with unprecedented haste, OTRI has tumbled to its lowest level in the data set — excluding the pandemic-induced lows of early 2020, which stretched OTRI beyond the bounds of its usual peaks and valleys. In 2019, the year of the industry’s last recession, OTRI hit a yearly low of 3.78%. OTRI has since blazed past that low in its race to find a new floor.

SONAR: OTRI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Over the past week, OTRI, which measures relative capacity in the market, fell to 3.66%, a change of 12 bps from the week before. OTRI is now 1,637 bps below year-ago levels.

Fourth-quarter company earnings from major carriers and 3PLs were a mixed bag this week. Landstar, an asset-based brokerage, reported its revenue per load was down 7% y/y but believes markets will bounce back by summer. C.H. Robinson, a heavyweight 3PL that has undergone C-suite turbulence recently, saw a destruction of international air and ocean freight demand in Q4 that led to the company’s net income falling 58% y/y. Schneider National suffered a 6.7% y/y drop in net revenue (excluding fuel surcharges) across its truckload, intermodal and brokerage divisions that led to a 15.8% decline in earnings per share. Nevertheless, Schneider also expects market conditions to improve later in the year.

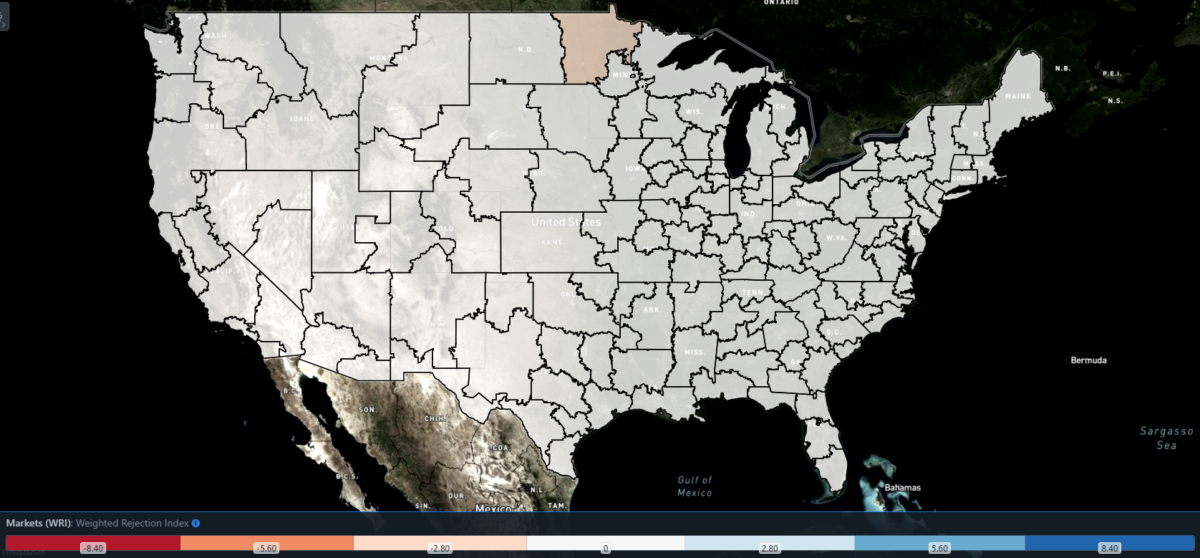

SONAR: WRI (color)

To learn more about FreightWaves SONAR, click here.

The map above shows the Weighted Rejection Index (WRI), the product of the Outbound Tender Reject Index — Weekly Change and Outbound Tender Market Share, as a way to prioritize rejection rate changes. As capacity is generally finding freight this week, no regions posted blue markets, which are usually the ones to focus on.

Of the 135 markets, 49 reported higher rejection rates over the past week, though 37 of those saw increases of only 100 or fewer bps.

The big story this week is Dallas, which was just rocked by freezing temperatures and ice storms that effectively shut down the region’s freight activity. Dallas’ local OTRI is only up 88 bps w/w at 2.94% but is coming down off Wednesday’s peak of 3.27%. Thankfully, the lasting impact of this weather appears to be minimal, especially when compared to the 2021 winter storms that led to persistent power outages — as well as soaring rejection rates — across Texas. However, freight demand in Dallas is down a considerable 15.3% w/w.

To learn more about FreightWaves SONAR, click here.

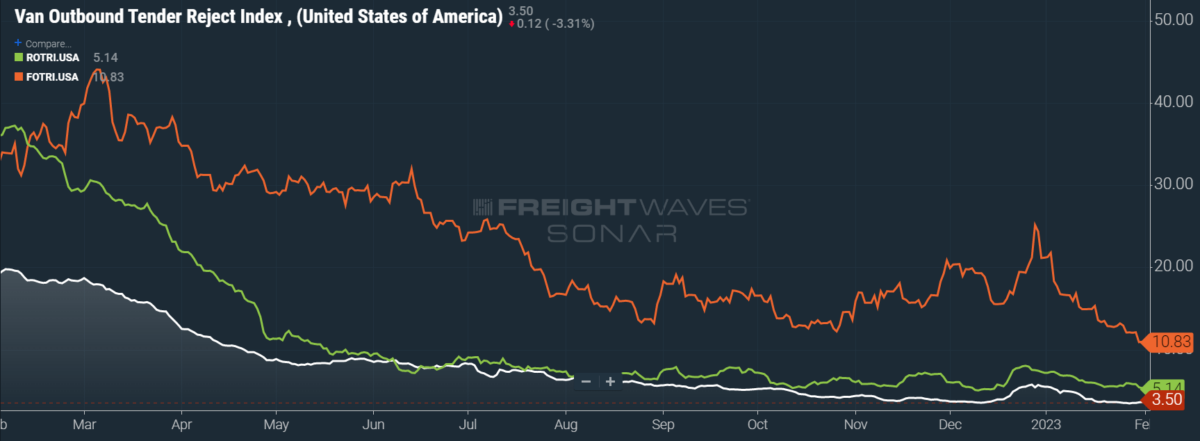

By mode: Flatbed rejection rates have been falling stepwise since the beginning of the year, when the Flatbed Outbound Tender Reject Index (FOTRI) was above 20%. As stated last week, the manufacturing and construction sectors have essentially rebuilt their inventories amid weakened demand, taking a considerable amount of flatbed freight off the table. Moreover, the housing market has been viciously bruised by 2022’s spike in interest rates, further reducing flatbed volumes. For the time being, FOTRI is down 124 bps w/w at 10.83%.

Van rejections are in a similarly bad way, though they are much nearer to their floor than any other mode. In August 2019, the Van Outbound Tender Reject Index (VOTRI) bottomed out at 3.29% — again, excepting pandemic-induced lows. After dipping to 3.44% on Jan. 27, VOTRI has recovered enough to remain unchanged w/w at 3.5%. The Reefer Outbound Tender Reject Index (ROTRI) lost last week’s gain of 46 bps w/w and then some, falling 77 bps w/w to 5.14%. Unlike VOTRI, reefer rejections are now much lower than they ever were in 2019, when ROTRI reached a yearly low of 8.61%.

Carrier rates continue steady decline

The one-two punch of OTRI falling to new floors and the deterioration of spot rates is the reason behind this column’s headline for the week. Contract rates are no better, though I still feel it is a bit early to take a victory lap. Since contract rates, which are reported on a two-week delay, are only showing data from the third week of January, they have some time to reverse their downward trend.

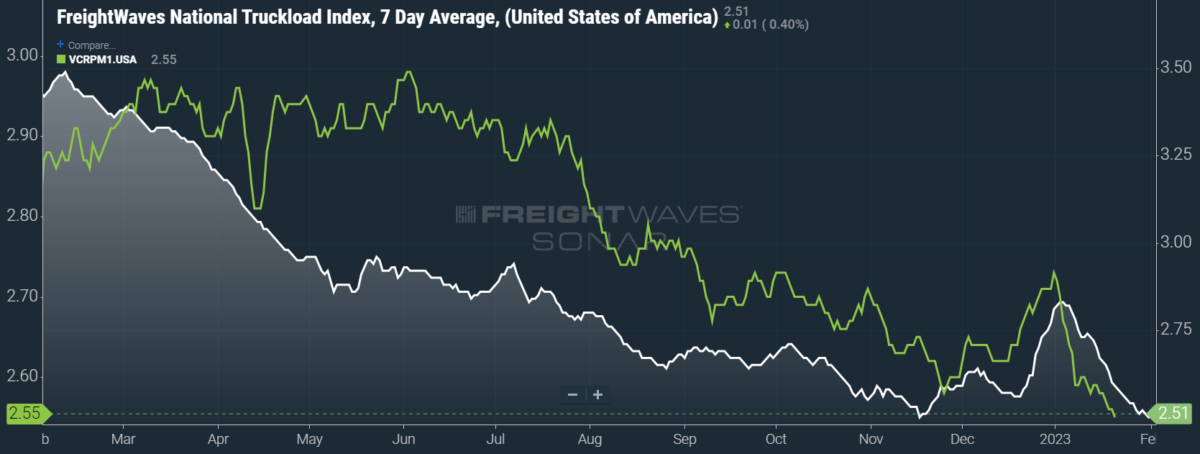

SONAR: National Truckload Index, 7-day average (white; right axis) and dry van contract rate (green; left axis).

To learn more about FreightWaves SONAR, click here.

In January 2022, for instance, contract rates — which exclude fuel surcharges and other accessorials — fell from a monthly peak of $2.89 per mile to $2.74 in under two weeks. But that massive dip did not stop rates from recovering to $2.88 per mile in just over a week. Although I don’t believe that contract rates will see such a dramatic resurrection this year, there is a precedent. As of Jan. 20, however, contract rates have fallen 4 cents per mile w/w to $2.55.

This week, the National Truckload Index (NTI), which includes fuel surcharges and other accessorials, fell 3 cents per mile w/w to $2.51. Even though retail diesel prices have declined 2.5 cents per gallon w/w, the linehaul variant of the NTI (NTIL) — which excludes fuel surcharges and other accessorials like contract rates — actually saw a greater drop of 4 cents per mile w/w to $1.78. This disparity could suggest larger carriers are benefiting from the gap between wholesale and retail diesel prices, as seen in the portion of their Q4 profits driven by fuel surcharges.

To learn more about FreightWaves SONAR, click here.

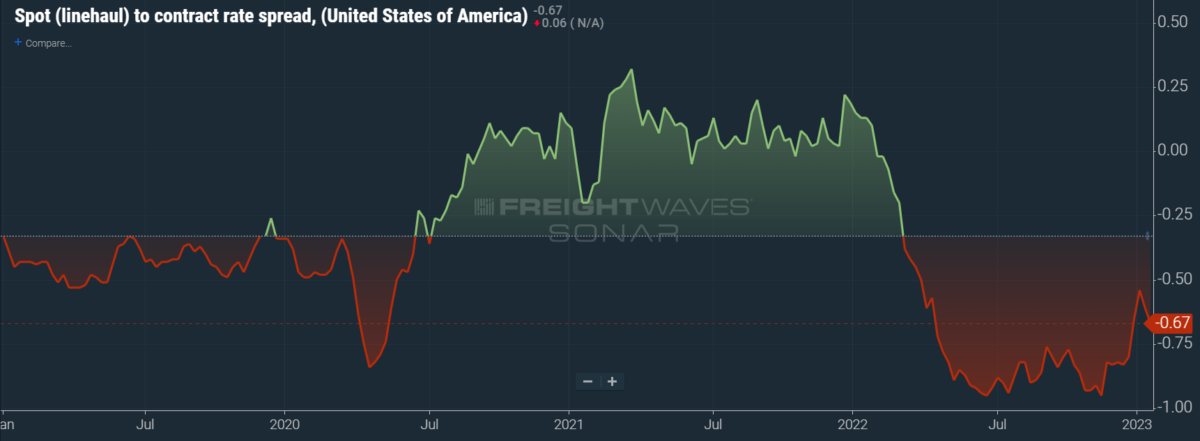

The chart above shows the spread between the NTIL and dry van contract rates, revealing the index has fallen to all-time lows in the data set, which dates to early 2019. Throughout that year, contract rates exceeded spot rates, leading to a record number of bankruptcies in the space. Once COVID-19 spread, spot rates reacted quickly, rising to record highs on a seemingly weekly basis, while contract rates slowly crept higher throughout 2021.

Despite this spread narrowing significantly over the first few weeks of the year, tightening by 20 cents per mile since mid-December, it has started to widen again. Since linehaul spot rates remain 67 cents below contract rates, there is still runway for contract rates to decline over the coming months.

To learn more about FreightWaves TRAC, click here.

The FreightWaves TRAC spot rate from Los Angeles to Dallas, arguably one of the densest freight lanes in the country, is quickly reaching new lows in the data set. Over the past week, the TRAC rate fell 5 cents per mile to $2.22. The daily NTI (NTID), which has risen to $2.62, continues to outpace rates from Los Angeles to Dallas.

To learn more about FreightWaves TRAC, click here.

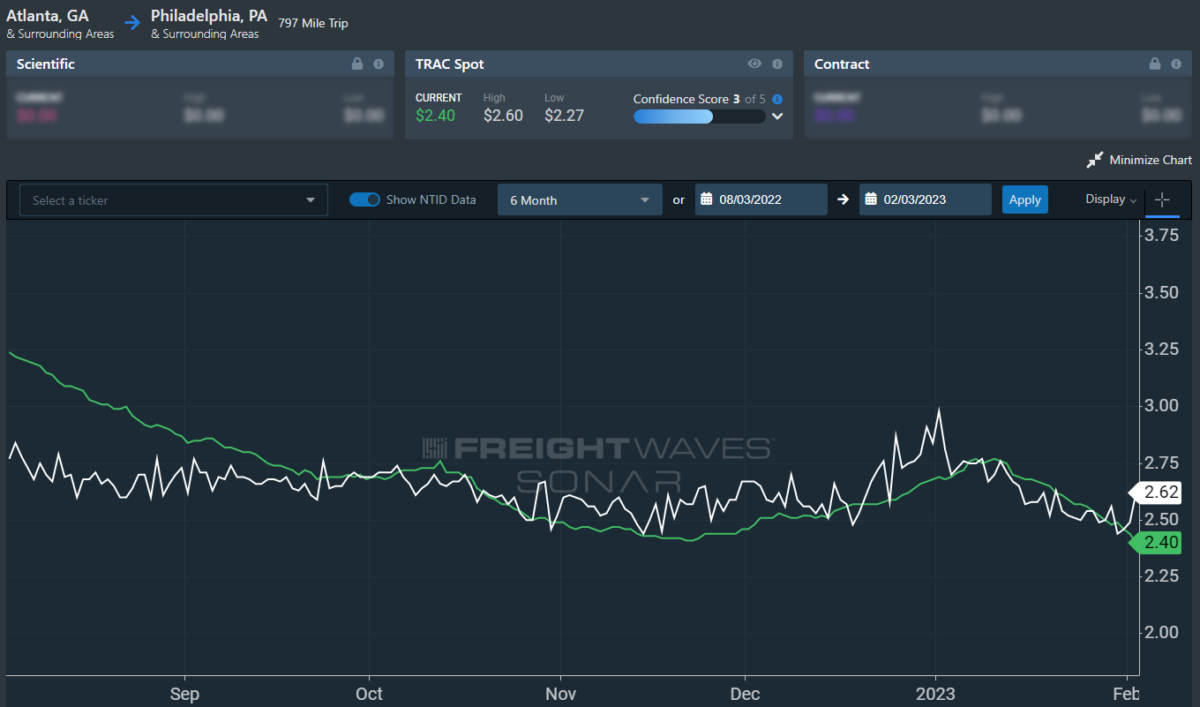

On the East Coast, especially out of Atlanta, rates are declining even more quickly and are separating from the NTID. The FreightWaves TRAC rate from Atlanta to Philadelphia fell 14 cents per mile this week to reach $2.40, compounding last week’s loss of 11 cents w/w. Except for the recent holiday run, rates along this lane have been dropping stepwise since mid-July, when the TRAC rate was $3.48 per mile.

For more information on the FreightWaves Passport, please contact Michael Rudolph at mrudolph@freightwaves.com or Tony Mulvey at tmulvey@freightwaves.com.