Israeli ocean carrier ZIM blew away all the analyst forecasts Wednesday, posting blockbuster earnings for its second quarter and revealing a massive increase in its full-year guidance.

ZIM (NYSE: ZIM) has moved fast to squeeze the most short-term gain out of what CEO Eli Glickman described as “anarchy in the world supply chain.” And like David versus Goliath, it continues to outperform much larger ocean carriers like Maersk on several fronts.

‘Home run’ results

ZIM reported net income of $888 million for Q2 2021 compared to $25 million in Q2 2020. Earnings per share of $7.40 came in well above the consensus forecast for $6.05. Adjusted earnings before interest, taxes, depreciation and amortization of $1.34 billion far exceeded analyst expectations for $890 million. It was “a home run,” said Fearnleys Securities.

The carrier also nearly doubled its guidance for full-year earnings — an “epic increase,” said Jefferies analyst Randy Giveans.

Previous guidance was for full-year adjusted EBITDA of $2.5 billion-$2.8 billion. On Wednesday, ZIM upped its outlook to $4.8 billion-$5.2 billion. The range midpoint jumped 89% to $5 billion, far above the analyst consensus of $3.8 billion.

ZIM’s shares close at $46.73 on Wednesday. Clarksons Platou Securities analyst Omar Nokta dramatically hiked his 12-month price target for ZIM’s stock from $58 all the way to $90. Giveans raised his target from $60 to $70.

Outperforming on rates and volume growth

ZIM’s average freight rate in Q2 2021 was $2,341 per twenty-foot equivalent unit, up 119% year on year and up 22% from the first quarter. ZIM CFO Xavier Destriau said on the conference call that rates are even higher in Q3 2021 and market strength should persist through at least Chinese New Year in Q1 2022.

To put rates in context, Maersk reported an average in the second quarter of $1,519 per TEU, much lower than ZIM. Hapag-Lloyd’s rates averaged $1,714 per TEU.

Destriau attributed ZIM’s rate outperformance to “our prioritization of a better-paying cargo mix.” The carrier has more targeted services than larger players, focusing most of its tonnage on the high-paying trans-Pacific and intra-Asia trades.

ZIM carried 921,000 TEUs in Q2 2021, up 44% year on year. That was triple industrywide volume growth of 15%, said ZIM, citing numbers from Container Trade Statistics. Maersk’s Q2 2021 volume rose 15.1% year on year. Hapag-Lloyd’s rose 12%.

The reason ZIM far outpaced larger carriers in terms of volume growth: It grew its fleet size much faster off a much smaller base. Unlike other carriers that own a portion of their fleet and charter the rest, ZIM charters its entire fleet.

ZIM’s fleet hit a recent low of 59 chartered ships in Q2 2020. Today, ZIM operates 113 ships, “on the way to 120,” said Glickman. In contrast, Maersk’s fleet capacity has grown only 1.9% year on year and Hapag-Lloyd’s by 1.4%.

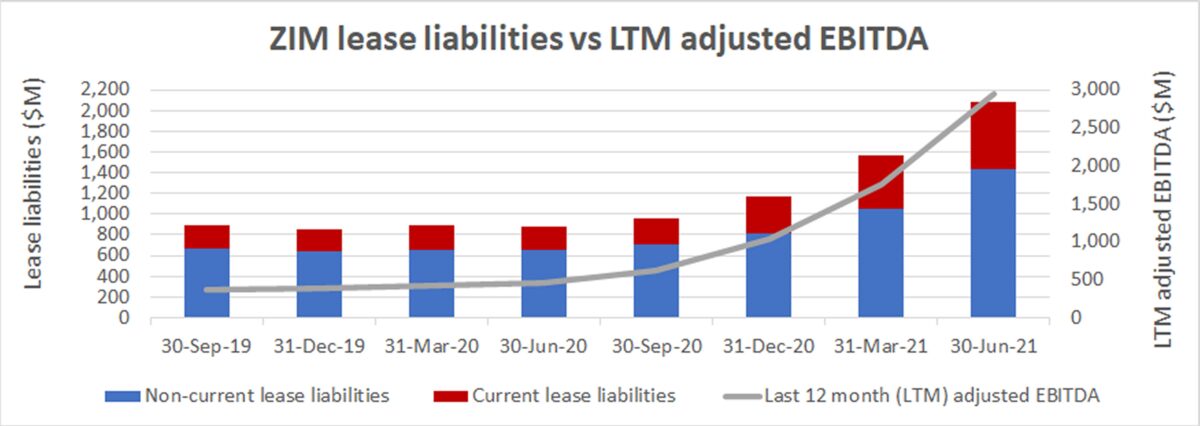

Longer-term questions

ZIM’s strategy poses two key longer-term questions. First: If profit growth hinges on more chartered ships — not just continually rising freight rates — what happens when there are no ships left to charter? That scenario is playing out now.

According to Destriau, “We note the changing face of the charter market, which is impacting the availability of charter tonnage. First, most of the fixtures concluded in the past six months have been multiyear charters. Second, a large number of small and medium-sized vessels have been sold by tonnage providers to carriers. [Both issues] have caused the non-operating-owner fleet to shrink.”

In response to this shift, ZIM is chartering the ships it can obtain for longer periods and is also seeking to grow via takeovers of regional operators.

“We are looking at options to potentially acquire smaller shipping lines that operate in regions where we already have a strong footprint and where we see significant potential for growth,” explained Destriau, highlighting opportunities in the intra-Asia market — particularly in Vietnam and Thailand — as well as in South America.

A second forward-looking question on ZIM’s strategy: What happens when spot freight rates eventually fall and the company continues to face very expensive lease obligations from multiyear charters signed at the market peak? ZIM has outperformed larger players in 2021 by trading increasingly longer-term lease obligations for higher near-term spot-rate exposure, but ship charters don’t just drive current earnings, they drive future liabilities that must be paid for with future freight-rate income.

As Vincent Clerc, Maersk’s executive vice president, warned on his company’s latest conference call: “We need to bear in mind, given the extreme levels that we see on the short-term rates, that the correction towards a more normal level could be quite rapid.”

Click for more articles by Greg Miller

Related articles:

- Global demand isn’t booming. So why are shipping rates this high?

- Maersk posts blockbuster Q2 results — and Q3 looks even better

- Container lines are poised to hit $100 billion profit jackpot

- Inside container shipping’s COVID-era money-printing machine

- Container lines set to topple quarterly profit records (again)

- How ZIM, a smaller ocean carrier, is blowing away the big boys