Predicting tanker rates has always been part science, part art, part wild guess. This year calls for even more artistry and wild guessing than usual.

Rates for very large crude carriers (VLCCs, tankers that carry 2 million barrels of crude oil) currently average $32,800 per day, up 130% year-on-year, according to Clarksons Platou Securities data. VLCC rates are averaging more than 3.5 times higher year-to-date than during the same period last year.

But where do they go next? On one hand, more production from the OPEC+ coalition could push more oil to sea. Ships available for spot deals could remain constrained by floating storage and Chinese congestion. If so, rates would rise.

On the other hand, OPEC+ export volumes could remain effectively unchanged. Congestion and storage could ease, pushing more ships into the spot trade. If so, rates would decline. Or it could be some combination of the above and rates would end up somewhere in between.

OPEC+ cuts: headline vs actual numbers

The OPEC+ coalition has targeted production cuts of 9.7 million barrels per day (b/d) since June. It confirmed last week that cuts would be pared to 7.7 million b/d starting in August.

The agreement “to bring back 2 million b/d of production … is expected to bring more seaborne cargoes to market, which we view as a positive,” Clarksons Platou Securities Managing Director of Research Frode Mørkedal said on Monday.

This assumes additional production will in fact go to sea. It may not.

According to Argus Media, Saudi Arabian oil minister Prince Abdulaziz bin Salman said that most of the extra 2 million b/d would either be used domestically, and not exported, or be counterbalanced by the compensation mechanism.

Coalition members that overproduced in May would theoretically compensate for doing so by cutting their production by the same amount in August. Due to compensation agreements, bin Salman estimated that actual cuts in August would be 8.1-8.3 million b/d, not 7.7 million b/d.

That would imply an extra 1.4-1.6 million b/d in August over July. However, the Saudi oil minister maintained that most of this will be used to cover seasonally higher power demand in the Middle East, for air conditioning, etc. In other words, it wouldn’t be loaded on tankers en route to Asia.

“Mark my words: Not a single barrel will be additionally exported than what we are exporting in July,” bin Salman affirmed.

How much does OPEC matter?

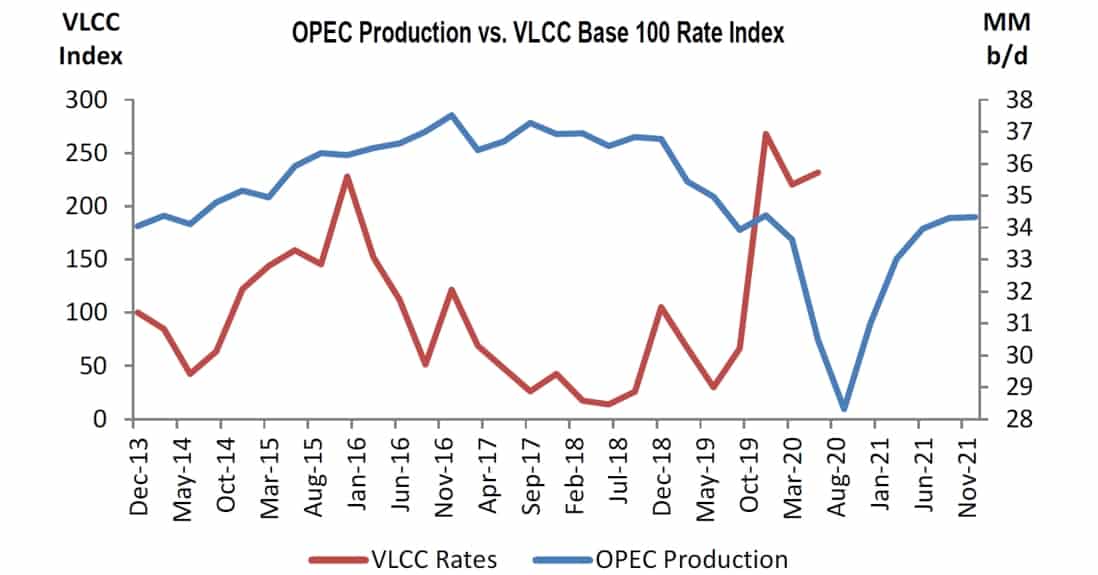

The current focus on OPEC production may actually be misplaced, said Evercore ISI analyst Jon Chappell on Monday.

“‘Tankers 101’ would tell you that OPEC production has the greatest correlation with tanker rates of any macro point. And history would provide that out — until the last few years,” he said.

“A perpetual period of [fleet] overbuilding, coupled with the emergence of the Atlantic Basin — primarily the U.S. — as a source of oil exports, has lessened the dependence of the VLCC market on the Middle East output.”

Chappell plotted OPEC production against an index of VLCC rates. The resultant chart shows the correlation between the two breaking down starting in late 2015 and early 2016.

Floating storage falling, but slowly

OPEC+ is one puzzle piece for tanker-rate forecasters. COVID-19 demand fallout is a second. Geopolitics a third. A fourth is floating storage and congestion.

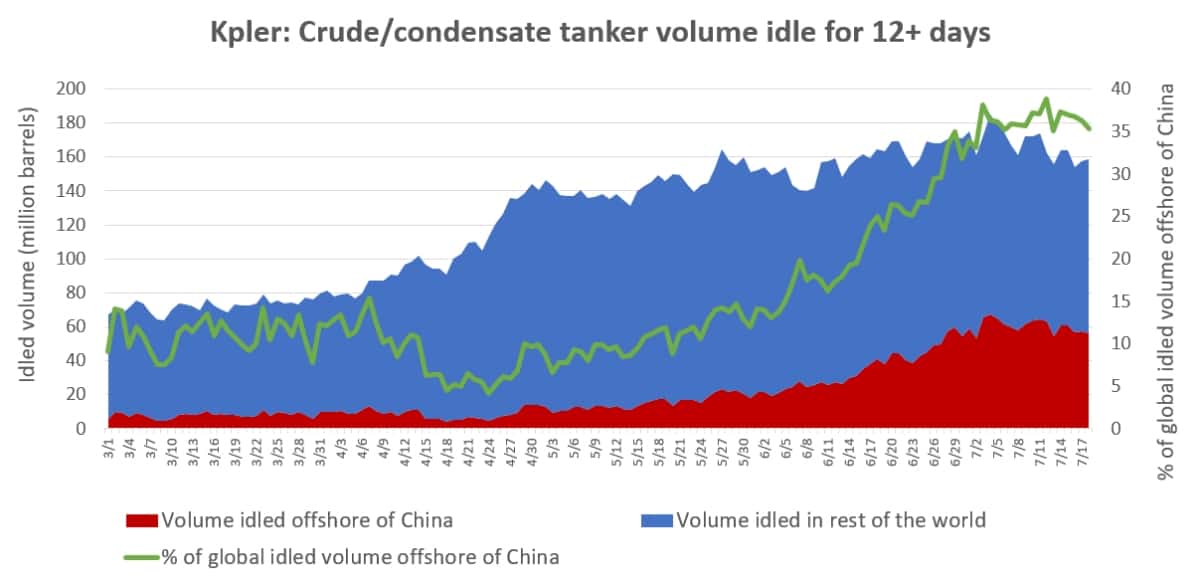

Mørkedal said, “The number of floating-storage vessels has remained generally unchanged over the past three weeks, with roughly 100 VLCCs still tied up, representing 11-12% of fleet capacity.”

FreightWaves was provided with the latest data on floating storage by Kpler. It shows crude tanker capacity, in million barrels, that has been idle for 12 or more days, both globally and offshore of China.

The Kpler data shows a peak of 184.9 million barrels on July 4. By Saturday, it was down to 158.7 million barrels, a decline of 14%. However, the volume of floating storage volume remains extremely high and China congestion — a key variable for vessel supply — is still near peak levels.

To the extent floating storage declines in the months ahead, more tankers would reenter the spot market. This would counterbalance some or all of the positive rate effects of more OPEC+ oil going to sea — assuming more does go to sea.

“The return of floating storage vessels to normal trading patterns may act as an offset,” acknowledged Mørkedal.

Second-half rate outlook

According to Randy Giveans, analyst at Jefferies, “We believe tanker rates will remain volatile and subdued this summer as the demand for floating storage unwinds and crude-oil inventories are destocked.”

He expects rates to be “relatively soft but stable” in the third quarter, although improved in September. He then expects rates to remain strong through year-end.

Mørkedal believes rates will “remain at low levels for the next few months.” After that, he sees OPEC+ cuts and inventory drawdowns precipitating “a major improvement in tanker demand and charter rates as we approach 2021.” Click for more FreightWaves/American Shipper articles by Greg Miller

MORE ON TANKERS: For more data on floating storage and Chinese congestion from Kpler and VesselsValue: see story here. How badly did tanker stocks perform in the first half? See story here. For a look at the rate bounce in early July, see story here.