In past editions of The Stockout, I’ve discussed cost inflation trends, which I believe is the industry’s largest issue currently aside from pandemic-related structural changes in demand. In recent days, many of the large CPG companies provided additional detail on pending price increases to pass those costs on to consumers. While that’s not a surprise, it is notable that inflation in CPG costs is higher than we have seen recently, with companies indicating that forthcoming price increases will be among the largest since 2018. Freight costs represent one category that is difficult or impossible to hedge, as I describe below.

To sign up for The Stockout, a newsletter focused on CPG supply chains, please click here.

COVID’s legacy on consumer products includes a pet adoption boom and a baby bust. In the early days of COVID, many speculated that lockdowns would give rise to a baby boom. Now, it’s safe to say that that speculation was wrong and COVID further depressed birth rates, which seem to decline each year in the Western economies to a fresh record post-Depression-era low. In addition, COVID discouraged immigration, which further slowed the rate of population growth in the U.S. The implication is for a slower revenue growth rate for most CPG companies, which already compete in generally slow-growth markets in the developed economies.

The exception to the COVID baby bust are those “pet parents” who consider their animals their “babies.” Pet food remains one of Nestle’s fastest-growing segments. Revenue in Nestle’s pet food segment grew 9% y/y in Q1 2021, which was on top of 14% y/y growth in Q1 2020. Pet adoption was a common consumer reaction to the loneliness and lack of travel that resulted from COVID lockdowns. In addition, growth in the demographics of single urban professionals and childless couples has given rise to a related trend in consumer products — demand growth for fresh and/or premium pet food.

Will consumers still act as their own baristas after life returns to normal? In addition to pet food, coffee is one of Nestle’s fastest-growing segments through sales of its Starbucks-branded products for at-home consumption in addition to its Nespresso- and Nescafe-branded products. Nespresso, in particular, has been growing strongly, posting organic growth of 17.1% y/y in Q1 2021 on 16.3% y/y volume growth and 0.8% y/y pricing growth. Unlike pet food, an area in which demand should be sustained post-pandemic, I believe that the recent boom in sales of coffee and related products for at-home consumption appears to be, at least partially, temporary. Many consumers have invested in espresso machines or French presses in the past year and may continue to use those devices, but many others will be eager to return to their local cafe.

Nestle cautioned analysts on the company’s margin expectations in light of rising cost pressures. The company maintained its existing guidance for organic revenue growth of at least 4% for fiscal 2021 despite the latest quarter coming in better than expectations (at 7.7% y/y) due to more difficult comps in the second half. In addition, management reminded analysts that, like most other CPG companies, Nestle is facing widespread cost pressure and analysts should, therefore, not expect a lot of operating leverage to go along with this year’s revenue growth.

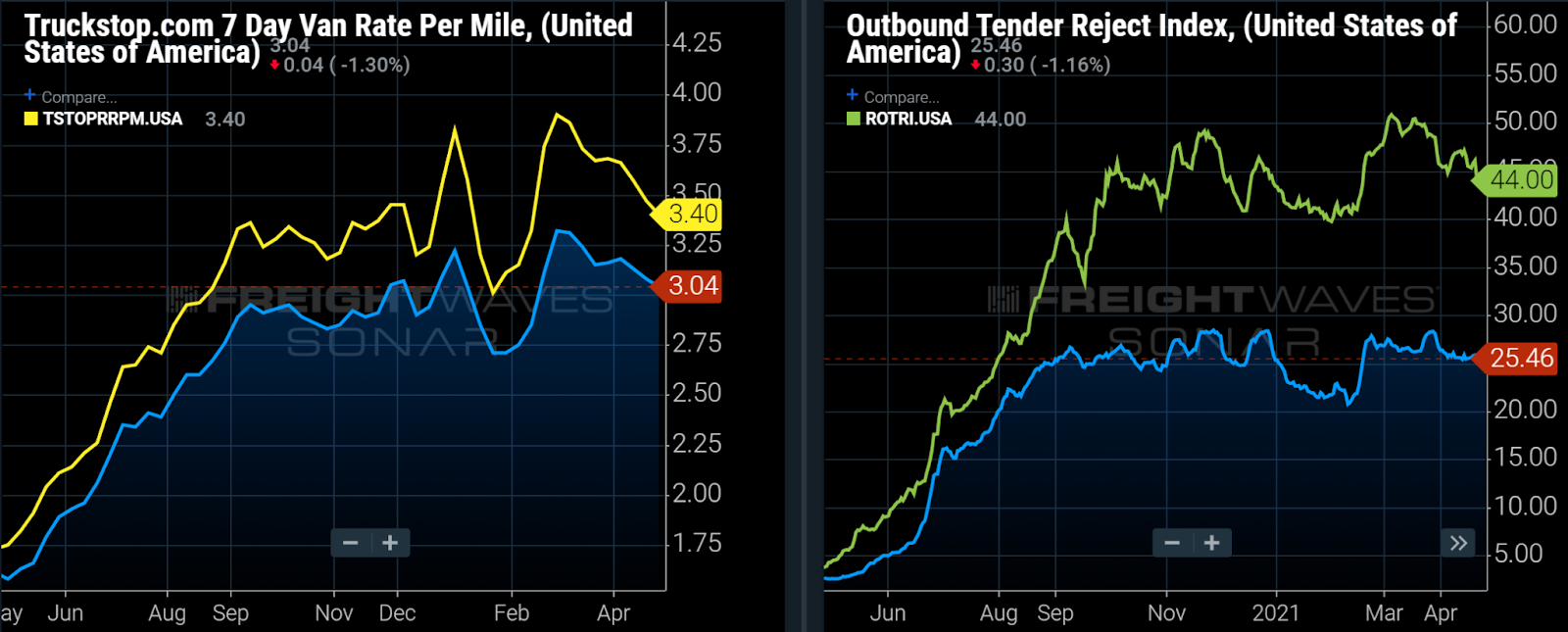

Some of the specific food segments where input costs are rising include dairy and cereals. While the company has cost hedges in place, they cover only a portion of the company’s costs and last only a few months. The company is able to hedge major agricultural inputs but is unable to hedge cost items such as packaging material and transportation costs. Despite the rising transportation costs in North America across modes, Nestle says that isn’t hasn’t had major disruption, but describes its U.S. supply chain teams as involved in a “daily fight” to supply the products.

Nestle is one of many CPG companies grappling with rising freight rates.

To learn more about FreightWaves SONAR, click here.

Oatmilk maker Oatley Group filed a prospectus to go public after more than doubling its revenue in 2020. One of the major trends in consumer products is the substitution of animal-based products with plant-based ones. Oatley is a Swedish company founded in the early 1990s that participates in that trend through the production of Oatmilk, which represents about 90% of its ~$400 million revenue. Other oat-based dairy substitutes in the company’s portfolio include oat-based ice cream and creamer for coffee. The company entered into an agreement with Starbucks to have its products at Starbucks locations nationwide, and former CEO Howard Shultz is one of the company’s famous backers, in addition to Oprah Winfrey and Natalie Portman.

Oatley appears to be a company that will be worth following in the CPG space, with implications throughout the supply chain. Currently, plant-based milk alternatives have a 14% share of the milk category, with share growth expected in the coming years. Plant-based milk has been growing ~5%/year while dairy milk has been flattish. So far, among milk alternatives, almond milk has the largest market share with 63%, but that could change as consumers are introduced to oat milk at their local Starbucks.

Procter & Gamble (P&G) will implement price increases in the mid- to high-single-digit range in a number of product categories starting in mid-September. The increases will be on baby products and a range of personal care products. While input costs have been rising across the board, the company cited rising input costs for resin and pulp as being a driver of the price increases for absorbent products. One of the company’s strategies is to introduce product innovations at the same time as price increases to mask the price increases to a degree.

Another interesting comment from P&G is that the company’s objective with its price increases is to offset cost increases rather than fully restore its margin percentage. So, the combination of higher input costs and higher prices likely will be margin-dilutive. The company is taking that approach to help preserve some of the share that the company gained in the past year (the largest national brands, in general, gained share from smaller brands and private-label brands last year). P&G’s price increases should not have been a surprise given rising input costs and since price increases of similar magnitude had already been announced by competitor Kimberly-Clark that will take effect in late June.

To receive The Stockout, FreightWaves’ CPG-focused newsletter, please click here.