CPGs have been playing catch-up on cost recovery

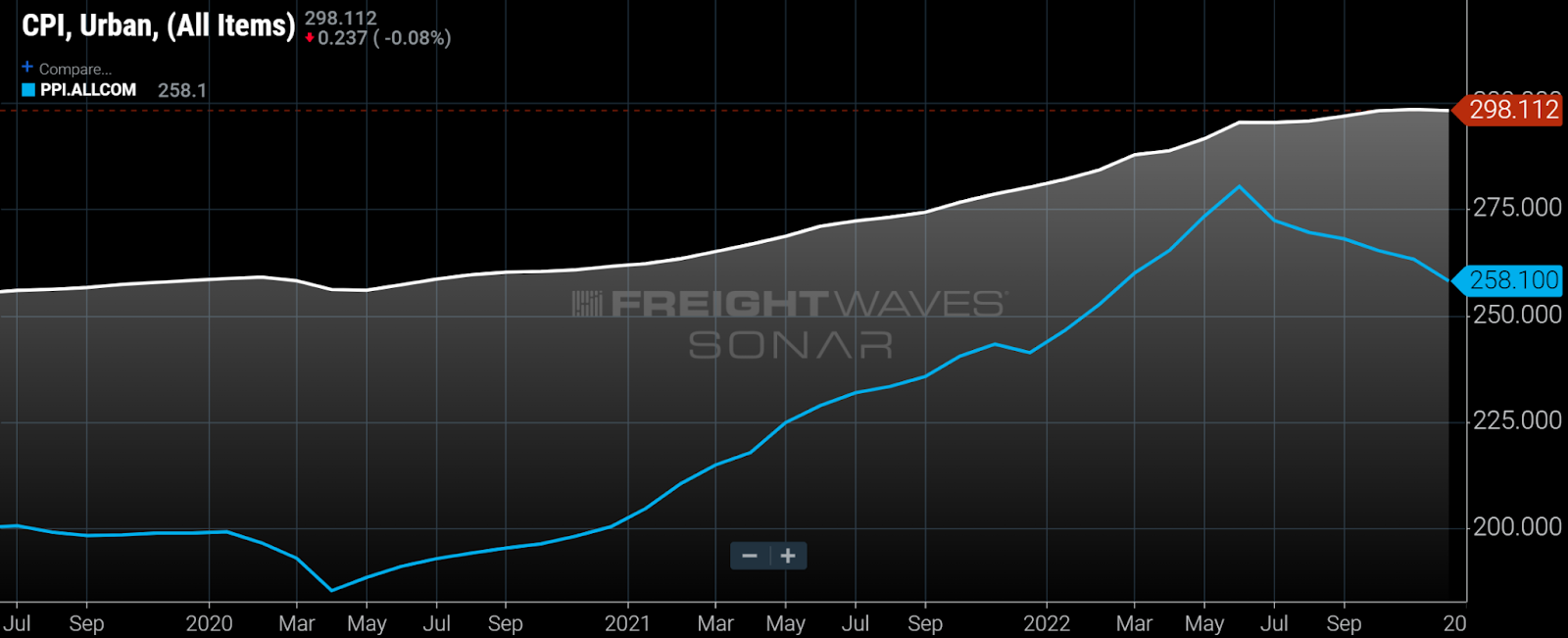

A frequent topic over the past two years has been the increasingly contentious relationship between consumer packaged goods companies and their retail partners. In that time, CPGs have gone to retailers asking for price increases more frequently in response to persistent cost increases. Even with frequent price hikes and fewer promotions that resulted in on-shelf prices up ~15% year over year (y/y) on top of near double-digit increases the year before, most CPGs experienced significant pressure on gross margins the past two years. CPGs’ costs simply change faster in response to shifts in commodity prices than retail prices do. So in a period of rising costs, they’re playing catch-up.

Retailers have responded to the frequent price increase requests by applying the old accounting adage — in God we trust; in all others we audit. At times, retailers built hypothetical CPG cost models to see if the price increases that companies were asking for were actually justified by inflation that they should be seeing in ingredients and other costs.

As the strain between the parties has grown, some CPGs’ perception was that retailers would stop accepting price increases once commodity prices retreated from their highs. That fear prompted Nestle and certain other large-scale CPGs to demand on-shelf price jumps relatively early in the process, assuming the retailers would shut the door later.

Point of greater retail pushback may be upon us

That brings us to this week and the much-discussed article from The Wall Street Journal that cites Whole Foods’ comments from a virtual summit highlighting how it is asking food suppliers to help bring down retailer food costs. According to the grocer, it has increased prices slower than competitors and cut prices on certain staples, like cereals and bread. The article also outlines the historical trend of CPG prices being stickier — not declining in response to falling commodity costs — than products where brands are less important such as meat, dairy and produce that reflect more of a pass-through of underlying commodity/ingredient costs.

It’s not a surprise that this push to lower retail prices is coming first — or at least most visibly — from a traditional grocer. While no grocer wants to admit to market share declines, and the relevance of the decline in foot traffic data cited in the article is disputed, it’s clear to me that traditional grocers have lost share to big-box, price-based options such as Walmart and Costco, as well as the private-label heavy grocers like Aldi and Trader Joe’s.

CPGs not on the same page

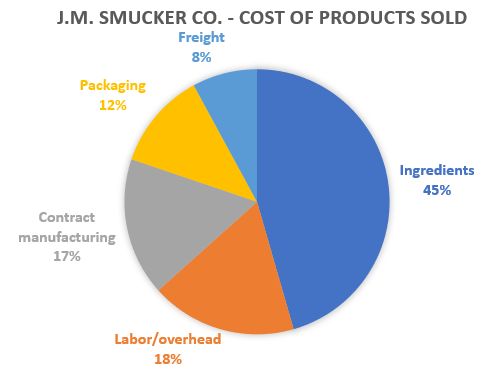

I’m not sure how much overlap there is between Whole Foods Shoppers and Oreo eaters, but in the first of presumably many similar questions on upcoming earnings calls, an analyst asked Mondelez if grocers are asking it for price cuts. The snacking giant dismissed that concern as unjustified, citing its expectation that its costs will be higher by a double-digit percentage in 2023 versus ’22, citing inflation in its particular set of ingredients, packaging materials and energy as well as the timing of its hedging programs that benefitted last year’s costs.

The other argument that I expect CPGs to make is essentially what I described in the first part of this newsletter — that most CPGs have taken price up less than their costs for the past two years and deserve a period of margin recovery to be made whole.

Black Rifle Coffee Co. on target with logistics

Ben Richey, senior director of distribution and transportation at Black Rifle Coffee, is becoming a regular on FreightWaves TV. This week Richey was featured on both WHAT THE TRUCK?!? and The Stockout and will participate in FreightWaves Global Supply Chain Week (register for the virtual conference here) CPG Day on Wednesday, Feb. 22. His comments are particularly relevant for other CPGs also experiencing fast growth, rolling out new single-serving products or participating heavily in the direct-to-consumer segment.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, click here.