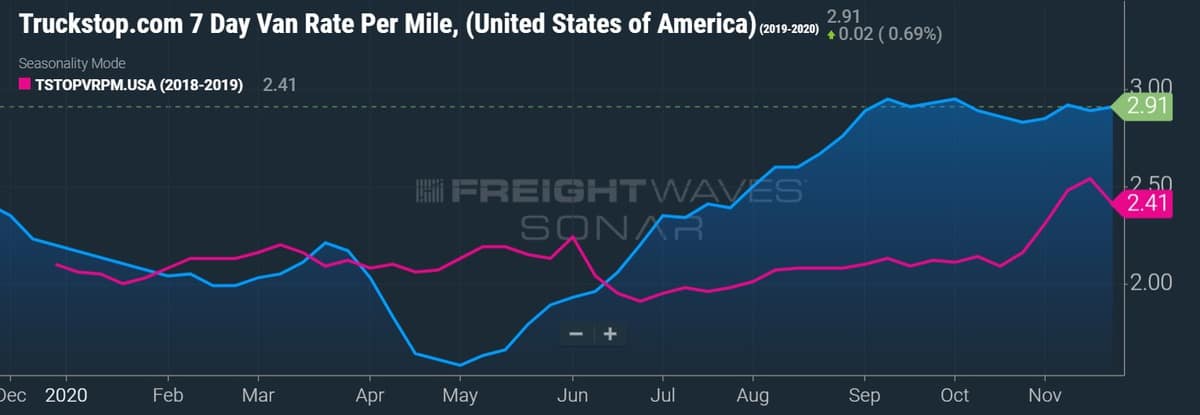

Elevated demand and tight capacity have highlighted the trucking market for a few months now. Recent data points and commentary suggest this dynamic may not abate anytime soon as most supply chains still lack adequate inventory and the trucks needed to move it.

Several of the nation’s largest retailers noted that while they have been able to modestly improve inventory positions, stock for many essential items remains below pre-pandemic levels. High demand for food and beverage items, retail consumables and home improvement goods has made it a struggle for these companies to keep product on their shelves.

Retailers’ inventories tick higher but sales soar

The October-ending fiscal third quarter provided the most recent update on how the biggest sellers of household merchandise are managing inventory shocks and their supply chains through the pandemic.

Retail inventories appear to have bottomed out during the second quarter with stock levels at some of the largest big-box chains increasing throughout the third quarter. However, inventory increases in the period remained subdued compared to surges in sales growth, leaving many still chasing merchandise.

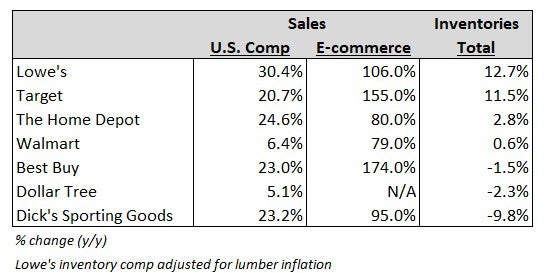

Walmart (NYSE: WMT) reported U.S. comp store inventory increased 3.6% (total inventory up only 0.6%) but comp sales climbed 6.4% year-over-year in the quarter. Further, the increase in inventory reflected an earlier inventory build ahead of the holidays. The company said its membership-only discount warehouse, Sam’s Club, saw inventory decline 8.5% as comp sales rose 7.9%.

Management noted it has been “disappointing” to see the number of stock-outs in consumables like bath tissue, cleaning supplies, bacon and breakfast items as some communities are stocking up in lockstep with rising COVID cases. They said inventory has improved from the second quarter but “we’re still below where we want to be.”

Target (NYSE: TGT) reported an 11.5% year-over-year increase in inventory, significantly better than the end of the second quarter, which concluded with supply down 3%. However, sales increased more than 20%. Management said further improvement is expected in the fourth quarter but “persistent inventory shortfalls” in electronics, home and apparel remain.

The Home Depot (NYSE: HD) saw a 2.8% year-over-year increase in inventory but U.S. sales climbed nearly 25%. The company did improve inventory positions in every week of the quarter but supply remained below pre-pandemic levels heading into the holiday season.

Lowe’s (NYSE: LOW) reported the largest increase in inventory, up 12.7% year-over-year excluding inflation in lumber prices, but sales outpaced the growth, increasing more than 30%. The company noted they have stocked up to meet “elevated customer demand.”

The seemingly endless inventory replacement cycle continues to keep demand for truck capacity elevated. Truck volumes recovered quickly as parts of the economy came back online in May and June. Demand surged through the summer, contrary to normal seasonal freight patterns, as consumers swapped summer experiences and services for hard goods requiring transport. Demand remained high through peak season and doesn’t appear to be slowing as some estimate the current inventory shock could take months to cure.

Carriers see inventory replenishment well into 2021

At investor conferences earlier in the month, management from several carriers and transportation companies commented on the low inventory levels among their customers.

Shelley Simpson, chief commercial officer at J.B. Hunt Transport Services (NASDAQ: JBHT), said its customers’ inventories remain low and that most were indicating inventory replenishment would continue through at least the first quarter.

At the same conference, Schneider National (NYSE: SNDR) CEO and President Mark Rourke said none of the company’s customers “feel good” about inventory levels. This gives him confidence that the high-demand environment will last over the next couple of quarters.

Werner Enterprises (NASDAQ: WERN) CFO John Steele sees the inventory correction lasting well into 2021. “[Retailers] made progress on inventory from where they were at the end of the second [quarter] to third [quarter], but they’re still at least a couple of quarters away, based on the math, from getting back to where they need to be, in part due to their sales being so strong.”

He believes surging e-commerce sales require supply chains to have more inventory on hand. “When you’re getting more digital sales as a large brick-and-mortar retailer, that means you probably need more inventory than normal to forward deploy that inventory close to where the customer is going to make their purchase so you can get it delivered within a one- to two-day period.”

Retailers’ inventories-to-sales ratio at all-time lows

Census Bureau data shows retailers’ inventories-to-sales ratios remained depressed in September at 1.22x, flat with the August reading and the record-low first set in June. The reading was also significantly lower than 1.35x in May and 1.68x in April, a month reflective of the height of economic shutdowns. The ratio hovered between 1.43x and 1.46x in the six months leading up to the pandemic.

Retailers’ inventories declined 9% year-over-year in September compared to a nearly 9% increase in sales.

Small businesses adding inventory too

Small businesses plan to add to their inventory positions over the next three to six months. The National Federation of Independent Business (NFIB) Optimism Index for October showed that respondents’ “plans to increase inventories” climbed one point to a record high of net 12%. The number of business owners that described their inventories as “too low” remained at record levels as well.

The overall optimism index registered a reading of 104 in October, flat with September, both of which are “historically high.” However, the uncertainty component of the survey, which was taken before the election, increased six points to 98, the highest mark since November 2016.

‘Busiest peak season on record’

The National Retail Federation (NRF) said the U.S. ports potentially recorded their “busiest peak season on record” in 2020. The result followed all-time highs for imports and online sales reached this summer, the highest levels recorded since the organization started collecting the data in 2002.

The group estimates 8.1 million twenty-foot equivalent units (TEUs) moved through the ports it tracks from the July through October peak season, a 6.1% year-over-year increase and more than 5% higher than the all-time high set in 2018. The October data hasn’t been finalized but the forecast assumes a 6.5% year-over-year increase during the month, following a 12.5% jump in TEU traffic during September. The ports of Los Angeles and Long Beach combined saw inbound loaded TEUs increase 25% year-over-year in October.

Containers flowing out of the ports at a high rate have been seen on the railroads. Intermodal traffic on the U.S. Class I railroads turned positive for good in early August and is up 10% year-over-year so far in the fourth quarter, according to the Association of American Railroads.

The NRF reported “core retail” sales, excluding transactions at automobile dealers, gas stations and restaurants, grew 10.6% in October, the sixth consecutive monthly increase. The date change of Amazon’s annual Prime Day, normally held in July, contributed to the increase. The group expects holiday sales during November and December to increase 3.6% to 5.2%, ahead of the 3.5% average over the last five years.

The NRF expects the recent surge in container traffic to come out of December and January results, which are forecast to decline 8.2% and 3.7% year-over-year respectively, following a flat November. The impacts of the pandemic won’t be fully recouped during 2020 as ports are forecast to process a full-year total of only 20.9 million TEUs, 3.4% lower year-over-year and the lowest annual result since 2017. Container shipments in the first half of 2020, down 10.1% year-over-year, were severely pressured by lockdown mandates.

However, container traffic is expected to surge again in early 2021. The group forecasts a 0.9% year-over-year increase in February and a 15.7% jump in March, a favorable monthly comparison from the onset of the pandemic in the U.S. and a continuation of factory closures in China.

Lack of inventory to fuel hot trucking market in 2021?

The need for supply chains to replenish stock post the holidays may take longer than normal and provide trucking with a lengthy runway of heightened demand. Complicating matters is the lack of truck availability in the market, largely due to declines in available drivers.

Driver schools are producing less than 70% of the number of graduates they were before the pandemic, nearly 50,000 drivers have been snared by the Drug & Alcohol Clearinghouse and 100,000 fewer CDLs were issued in the first half of the year. Add in normal attrition and early retirements over COVID fears and it appears the supply side of trucking will take time to catch up to demand.

Increases in new Class 8 tractor orders suggest capacity will be entering the market in 2021. But it’s important to note that the rate of new orders over the last four months, a 27,000-unit monthly average, pales in comparison to the more than 40,000 trucks that were ordered on average every month of the 2018 capacity surge.

High demand and a slow return of capacity have many carriers setting the table for high single-digit to low double-digit contractual rate increases next year. Spot rates, the benchmark for contractual rate negotiations, have been higher on a year-over-year comparison since late June. In addition to improving their margins in 2021 through rate increases, carriers will also look to recoup inflation on key cost lines like driver pay and insurance expense.

The trucking fundamentals that have dominated the second half of 2020 – elevated demand, tight capacity and rising rates – appear likely to hang around for a while.