Two more strong reports are in from a fourth quarter that brushed aside concerns of a significant downward trend in freight markets.

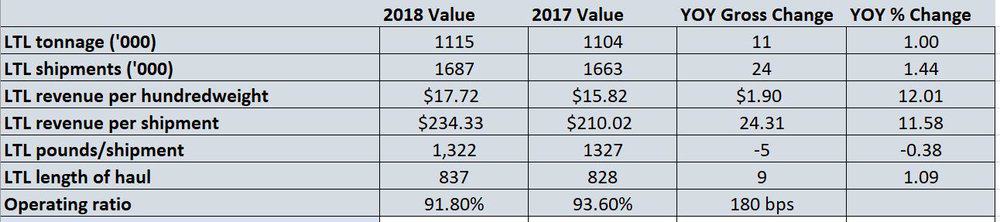

– Less than truckload (LTL) carrier Saia (NASDAQ: SAIA) reported a 12.9 percent increase in revenue, a 45.4 percent increase in operating income and a 180 basis points (bps) rise in operating ratio to 91.8 percent. LTL revenue per hundredweight was up 12 percent and LTL revenue per shipment was up 11.6 percent. The fourth quarter results capped off full-year results that featured a revenue jump of 17 percent, a 49.1 percent increase in operating income and a 180 bps improvement in operating ratio to 91 percent, the same increase in bps as in the quarter. Saia cut its total debt to $122.9 million at the end of 2018 from $132.9 million at the end of 2017 and capital expenditures (capex) jumped to $251.7 million from $217 million. Saia announced that capex is going to take a big jump in 2019 to $300 million.

In the company’s prepared earnings statement, CEO Rick O’Dell cited Saia’s Northeast operations in what it described as “new markets” in that region in touting the performance. He said business in the Northeast was running at an annualized rate of $150 million as 2018 ended and there are four to six new terminals to be opened in the region in 2019. “Approximately 75 percent of the freight moves we are handling in the Northeast are for customers who were already using Saia in other markets and understand the value proposition we offer.”

In a note to investors, the Deutsche Bank transportation team led by Amit Mehortra described the results as “good” and said the underlying earnings per share of 90 cents were two cents more than consensus. “Revenue growth remained strong in the quarter at +15 percent amidst continued strength in yield trends (revenue per pound +12 percent year-over-year), which partially offset the deceleration in tonnage trends (+1 percent vs. +7 percent in full-year 2018), though we believe the slowdown reflects a more strategic approach to freight selection rather than a meaningful decline in demand trends,” the Deutsche Bank team wrote. “Looking forward, the outlook for tonnage growth in 2019 is somewhat mixed as the impact from six new terminals opening in 2019 is expected to be somewhat mitigated by tough comps and reduced demand for TL spillover.”

The Saia numbers got a warm reception on Wall Street, where at approximately 1:00 p.m. Eastern time the stock was trading at $63.18, a gain of 3.93 percent on the day. The stock is down approximately 18.4 percent in the last 12 months, according to Barchart.

– Bank of America Merrill Lynch likes the stock of Schneider National (NYSE: SNDR) so much that it gave a two-step increase in its recommendation for the truckload carrier, boosting it to “Buy” from “Underperform.” In a report, the team led by Ken Hoexter noted that the company’s forward price/earnings multiple has been pushed down to 12 times earnings from 17 times earnings, “a level we believe accounts for a more bearish market.” Part of the basis for the increase was the performance of the Schneider intermodal division released last week as part of the company’s fourth quarter earnings. Schneider’s operating ratio in that sector was in the mid 80s, “besting J.B. Hunt for the fifth consecutive quarter.” As the largest intermodal operator, the performance at Hunt tends to be the benchmark by which other intermodal operations compare themselves to.”

But Merrill Lynch also noted that Schneider had said in its earnings release last week that the operating revenue (OR) improvement in intermodal, which is 23 percent of all Schneider revenue, was probably the peak that could be expected for now. The rest of the Merrill Lynch report was not overly effusive in its praise of Schneider but was mostly a caution that things aren’t all that bad. Rather, Merill sees a company that has had significant stock weakness that is not justified by its earnings or the state of the freight market. “Its Truck segment posted an 86.8 percent operating ratio, and while still well off best-in-class Knight-Swift’s Truckload segments which are in the 70s, it is still 400-900 bps better than the average truck operator,” the report said. As the title of the report says, the rating of the company was raised to Buy “as fears of market compression recedes.”

Schneider’s stock price at approximately 1:00 p.m. Eastern time was up 1.51 percent, leading other truckload carriers except Heartland Express, which was up slightly more percentage-wise.