Marten Transport had a record-breaking first quarter, with all-time highs in several key categories.

Operating revenue was a record at $287.3 million, up 28.8% from the first quarter of 2021, but it was boosted significantly by fuel surcharge revenue, which came in at $42 million. That was up from $24.9 million from the prior year.

Most significantly, Marten’s (NASDAQ: MRTN) operating ratio net of fuel surcharges came in at 85.4%, according to an investors slide released by the company in connection with the earnings. The company said that number was the best for any quarter since it went public in 1986.

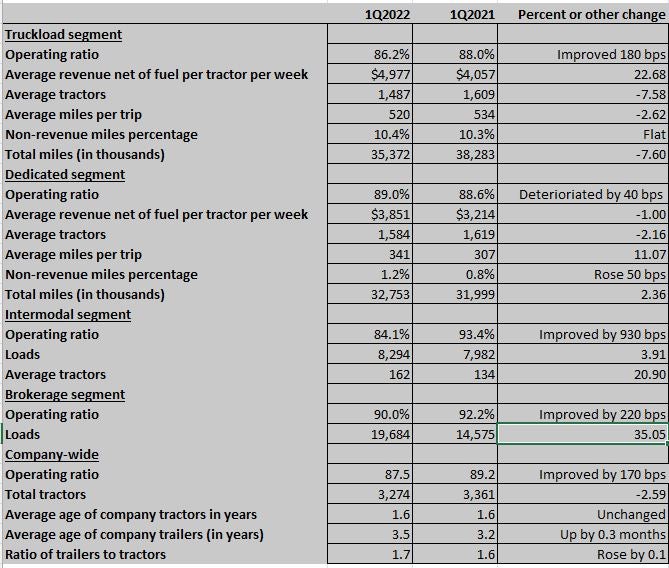

The operating ratio for the company as a whole improved to 87.5% from 89.2% in the first quarter of 2021. That figure includes the impact of fuel surcharge revenue.

Operating revenue net of fuel surcharges was not reported as a record but was still up 23.8% from the corresponding quarter of 2021.

Operating revenue as a whole was reported as a record, coming in at $287.2 million. Operating income of $35.9 million was a quarterly record, rising sharply from the previous record of $30.7 million, recorded in the final three months of 2021.

The bottom line for Marten: earnings per common share that rose by just about 50%, to 33 cents per share from 22 cents per share a year ago. Net income climbed to $27.5 million from $18 million, and operating revenue at $287.2 million was up 28.7% from a year ago and 7.6% sequentially.

Sequentially, net income was up from 30 cents per share. Net income of 33 cents per share beat consensus estimates by 7 cents, according to SeekingAlpha. The revenue figure of $287.3 million beat consensus by $25.1 million.

Marten released comparative data that reflects a strong year-on-year performance in two key metrics: operating revenue net of fuel, and operating income. But it’s not a surprising run: The data goes back to the second quarter of 2020, when after a brutal April the trucking market began to soar, showing signs of a slowdown just in the past few weeks.

But even during that run, not every company can claim quarterly improvements over the prior three months from a year earlier in operating revenue net of fuel, operating income and net income. Marten has produced year-on-year quarterly improvements in those categories for each of the past eight quarters, and most of the comparisons are in double-digit percentages.

With fuel surcharges up so substantially, it can skew some of the numbers into looking better than they might have otherwise. But the performance of Marten stripped of the fuel surcharges was still impressive.

The average revenue net of fuel per tractor per week in the truckload segment was just under $5,000, at $4,977. That was a big jump from the $4,057 recorded last year. Marten turned in that performance in the truckload segment on fewer total miles (35.3 million vs. 38.3 million), and a drop in average miles per trip, down to 520 from 534. The truckload OR was 86.2%, improved from 88% a year earlier.

The dedicated division, despite its slightly worse OR — weakening to 89% from 88.6% — also posted several sharp improvements in operating metrics. The average revenue net of fuel per tractor per week rose to $3,851 from $3,214.

The one group that did significantly better was intermodal, where OR improved to 84.1% from 93.4% a year earlier.

Brokerage OR came in at 90%, an improvement from 92.2% a year earlier.

The higher cost of labor and the tight market for capacity were clear in the quarterly report. Salaries, wages and benefits climbed 22.3% to $89.34 million, while purchased transportation rose 40.6%. The quarterly figures were higher sequentially as well: Salaries, wages and benefits were up less than 1%, but purchased transportation was higher sequentially by almost 5%.

Marten does not hold a phone call with analysts. In prepared comments accompanying the earnings release, Executive Chairman Randolph Marten disclosed several other operating statistics: The company had 128 more drivers employed at the start of the second quarter than three months earlier, and it added 95 refrigerated containers during the quarter, bringing the fleet to 729.

Marten also took two significant steps to return money to shareholders during the quarter. It repurchased 1.3 million shares of Marten stock for $25 million, and the company’s dividend was increased 2 cents per share, to 6 cents for a 50% increase during the quarter.

Marten also noted that the repurchased shares were “retired,” as opposed to being put into the company’s treasury for later disbursement.

Like most transportation companies so far in 2022, gains in the company’s stock have been tough to come by. In the past 52 weeks, Marten stock is down 6.84%. But in the past month, it’s down 16.58%.

More articles by John Kingston

XPO’s Jacobs predicts biggest transportation disruptor: 3D printing

Perry at TIA: Excess trucking demand hit 26%, returning to normal

Truck transportation jobs drop for first time in nearly 2 years