Image: Jim Allen/FreightWaves

by Todd Maiden, FreightWaves

During question and answer sessions at the Stifel 2020 Transportation and Logistics Conference, several truckload (TL) carriers said that they expect to see an improving TL market this year.

Current volumes

On the current environment, Heartland Express Inc. (NASDAQ: HTLD) CEO Michael Gerdin said he’s expecting a “flattish environment” in 2020. He said volumes have been “OK” in part due to favorable weather compared to the 2019 winter. He said most of the company’s customers expect to move more shipments year-over-year in 2020, but noted that the bulk of the increase will come in the back half of year.

Outbound Tender Volume Index (USA) – SONAR: OTVI.USA

Werner Enterprises Inc. (NASDAQ: WERN) President and CEO Derek Leathers said commentary from retailers, who provide approximately half of the company’s revenue, has been “pretty bullish.” He said favorable factors like strength in the housing sector, a consumer with money to spend and an improved trade environment are reasons to be more constructive on demand in 2020.

Leathers said the company’s dedicated pipeline is stronger than it was a year ago, but he noted that there are more carriers vying for dedicated freight currently. He said the increased competition will probably result in a lower dedicated contract win rate in 2020 as some of the new participants don’t understand the complexity of running dedicated freight and ultimately underprice their contracts. Leathers said Werner will remain disciplined as it pursues new dedicated contracts, but the environment could yield a lower win rate in the year.

Werner has guided to a truck count that will be down 3% to up 1% year-over-year in 2020.

U.S. Xpress (NYSE: USX) President & CEO Eric Fuller said the market was a little better. He said demand has improved and that while the company is seeing the typical sequential decline in freight moved from the fourth quarter to the first quarter, the drop-off isn’t as severe this year.

Rates and negotiations

Gerdin said shippers are still trying to get the lowest rate while carriers are trying to pass through cost inflation like insurance premium increases, soaring claims, higher health benefits expenses, etc. He said Heartland has completed roughly one-third of its 2020 bid process and contractual rate bid negotiations are running level with last year so far. The company expects rates to be flat or minimally higher in 2020.

Werner CFO John Steele said the company is seeing spot miles higher than normal, currently in the 13% range as Werner has walked away from some business where the freight rates weren’t adequate. As such, he expects contract rates to be flat to slightly lower as the company has more spot miles in the first half of the year.

The company’s official guidance calls for or a 5-7% decline in revenue per mile in its one-way TL segment in 2020 given the elevated spot exposure, less surge freight activity and slightly lower overall volumes. The lower revenue-per-mile guidance does not include the company’s dedicated freight division, which accounts for 58% of its truck revenue.

On Werner’s Feb. 5 earnings call, management said contract renewals in one-way TL have been flat to down a couple of percentage points so far in 2020. They expect spot rates to be down 15% in the first quarter and 5% in the second quarter. Approximately 70% of the company’s contractual bid season will occur in the first half of 2020.

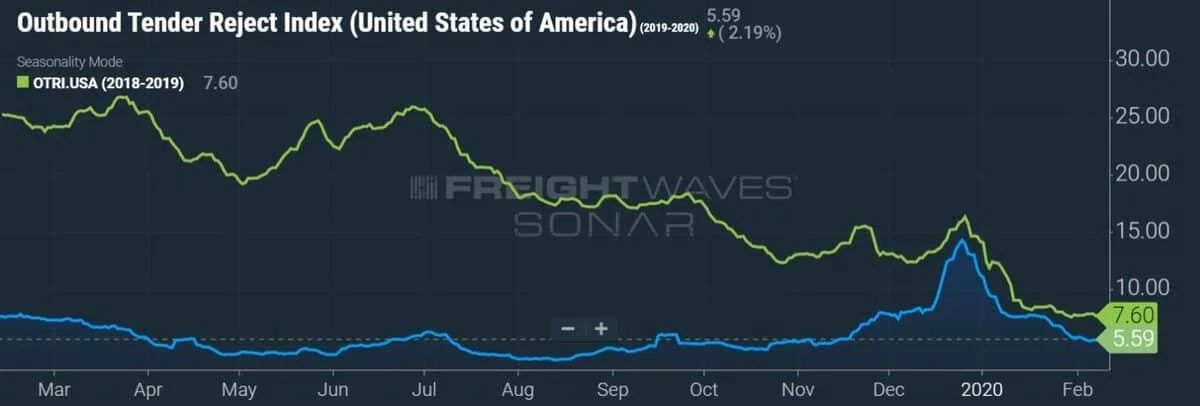

After firming to close the year, the Outbound Tender Reject Index remains under 2019 levels. Recent readings suggest that capacity is still too loose to push spot rates higher in the immediate near term.

Outbound Tender Reject Index (USA) – SONAR: OTRI.USA

Capacity leaving the market

Every management team mentioned truck capacity coming out of the market, referencing lower Class 8 truck orders, last year’s mandate for full compliance on electronic logging devices (ELDs), the Drug & Alcohol Clearinghouse, and rising insurance premiums and claims expense.

Gerdin said Heartland is seeing more carriers putting themselves on the market to be acquired, a trend he expects to grow as TL fundamentals remain tough.

Freight volumes remain steady, but TL rates have been under pressure for some time. While many analysts expect volumes and price to inflect positively at some point in 2020, a large number of carriers are being squeezed by higher costs including insurance, health and benefits expenses. Additionally, gains on the sale of used equipment, as carriers trade in or sell older truck models, have been declining as overall truck demand has fallen in the past year.

Gerdin said the used truck market wasn’t terrible, but he noted that it has clearly softened.

As such, carriers’ margins are thinning. Operating ratios – the ratio measuring the percentage of operating expenses for each dollar of revenue – are back to unsustainable levels. The concern of not being able to recoup cost inflation through rate increases in the future is prompting some carriers to exit the market while they can.

Operating Ratio (Company Fleet – Dry Van) – SONAR: OPRAT.VCF

Fuller said that anecdotally he is hearing that several carriers are not renewing tags on some of their equipment, which he believes will lead to more capacity coming out of the market.

U.S. Xpress CFO Eric Peterson also sees rising insurance costs as a likely capacity-limiting factor in 2020. He said some of the smaller carriers that don’t have the balance sheet to self-insure any portion of their liability exposure are seeing premiums double and triple compared to their year-ago renewals. He said he spoke with a smaller carrier recently that was very excited that its insurance premium only rose by 50% compared to the year prior.

U.S. Xpress self-insures the first $3 million per occurrence for vehicular bodily injury and property damage.

U.S. Xpress has made several moves to lower its total insurance expense, which Peterson believes is 100 to 150 basis points as a percentage of revenue higher than that of its peers. The company has implemented initiatives like a new driver training program, requiring hair follicle testing on all of its drivers and outfitting its trucks with forward-facing event recorders.

On the insurance front, Gerdin said it’s not just increases in insurance premiums, but many providers are limiting the amount of exposure they are willing to carry for any one TL carrier.

Leathers said he has seen carriers shrink their fleets as TL costs have risen. He said lower used truck prices have impeded smaller fleets from buying new and specifically said insurance renewals and nuclear verdicts have been reducing industry capacity.

“A third of the truckload group either lost money or made 1% or less last quarter. So, if one-third of the publicly traded group is in that kind of shape, imagine what small to midsize carriers across America look like today,” Leathers said.