In an earnings season full of trucking and transport companies declaring they’ve seen a sharp falloff in volumes this month, carrying over from a late March collapse, truckload carrier U.S. Xpress is an outlier.

Given the mix of its freight, CEO Eric Fuller said April volumes have held largely steady even as some other trucking firms are reporting year-on-year declines of 20%.

“U.S. Xpress has a strong customer mix of grocery, e-commerce, consumer products, discount retail, and home improvement, with little exposure to automotive, manufacturing and restaurants,” the company said on Thursday, April 30, in announcing its first quarter earnings. “The company has not seen a drop in total load volume to date through April.”

In the company’s conference call with analysts, Fuller noted that the heavy mix of grocery, home improvement and discount store operations in the USX customer base meant that after the pandemic hit, 96% of the company’s clients stayed open. “We have almost no exposure to those areas where verticals shut down during March and into April,” he said, citing automotive and restaurants as the types of industries that closed as a result of the pandemic. Speaking of the USX base, Fuller said: “If anything, our customers increased shipments in this period so that really helped us weather through this event.”

Fuller noted that when the pandemic hit its markets, only 40 drivers in the USX fleet found themselves stuck at customer operations that had been closed.

Despite the positive mix that the company had going into the pandemic, its financial results proved to be the opposite. Wall Street reacted to the numbers with a stock price decline of approximately 6% by 11 a.m., though with the stock of USX trading near $4.50/share, it doesn’t take a major move in price to result in a significant percentage swing.

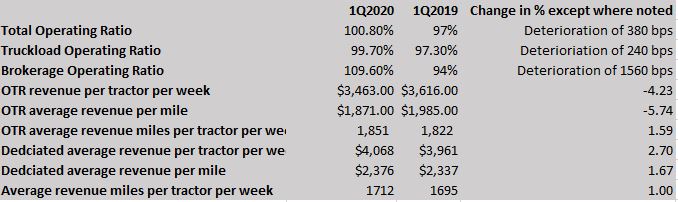

The adjusted overall operating ratio (OR) at USX came in at an unprofitable 100.9%, compared to 95.7% in the first quarter of 2019.

But truckload operations at the company, which include over-the-road (OTR) and Dedicated divisions, had an adjusted OR of 99.6%, compared to 96% in the first quarter of 2019. It was an ugly OR of 109.6% in the company’s brokerage division – down from 94% last year – that led to the total OR being on the wrong side of 100%.

In the statement announcing its earnings, USX said brokerage revenue rose to $50.47 million from $46.24 million last year, but the gross margin plummeted to 3.7% from 17.5% in 2019’s first quarter.

The fact that USX saw its volumes maintained was clear in the figure for average revenue miles per tractor per week. OTR operations posted a 1.59% gain in that area; in the Dedicated division, the gain was 1%.

But laid up against weaker rates, OTR revenue per tractor per week was down 4.2%. Dedicated’s performance in the same category rose 2.7%.

“There is increasing rate pressure from certain customers and non-traditional competition from others who have seen a drop in their core verticals,” Fuller said on the earnings call. “We expect to see rate pressure continue.”

The bottom line was a net loss of $9.232 million, compared to a first quarter 2019 net profit of just over $5 million. But total operating revenue was up to $432.5 million from $415.3 million.

Purchased transportation was one of the expenses that helped generate the ink red. It was up to $129.7 million in the quarter, from $114 million a year ago. That increase is roughly in line with changes in the company’s operating income, which went to negative $3.66 million from positive $12.6 million.

Although there were few questions about the company’s financial performance on the conference call, there was one pointed query – “Why do you have an OR of 100% when competitors have managed to stay to the positive side of that benchmark?”

Fuller said USX remains in the middle of a “significant transformation,” adopting digitization and automation as a growing part of its business. He also said the types of companies that the question implicitly compared USX to have been “operating at that for an extended period of time.”

The types of changes USX is seeking to implement “don’t happen overnight. We need to drive results by staying consistent with our plan.”

Fuller said driver turnover at USX has been a long-term factor in the company’s performance relative to its truckload peers. He said it’s been the company’s “biggest issue for a long, long time.”

“That is something we’ve put a lot of focus on,” Fuller said. “The needle has moved a lot slower than we’ve liked.” But he remained optimistic that “all the initiatives and investments will continue to drive better results in turnover and that’s where we’ll get the biggest impact.”

Turnover in the industry is at present favorable to carriers, Fuller said, but he said it is a “false positive” that he does not expect to last. “The environment has made it less likely for drivers to want to switch,” he said. Drivers are “hunkering down and staying where they are.”

Fuller added that USX “probably has the lowest number of unseated tractors in our fleet in a long time.”

One piece of the future landscape that Fuller said USX is expecting is reduced capacity. But it hasn’t happened as much as he would have expected because such financial assistance vehicles as the Paycheck Protection Program were keeping many companies alive that might have otherwise faced bankruptcy. “We do think that there is some capacity that will be propped up through government action,” he said.

In a separate part of the call, Fuller said USX’ exposure to spot rates was about 11-12% of revenue. He said the company generally targets that figure to be 10%, but that in 2019 it rose as high as 14-15%.

And while he made repeated references to the decline in spot rates, while discussing the company’s performance relative to its peers, Fuller refused to blame spot rates for the company’s first quarter performance or even for longer-term issues. The challenges Fuller said he is tackling at USX are on the cost side of the ledger.

Like other companies across the spectrum, not just in trucking, USX touted its liquidity going forward. It was noted on the call and in the earnings release that USX in late January had secured a new $250 million line of credit, part of which was used to pay earlier debt obligations; at the time of that release, the company said after the refinancing of the debt that it had more than $100 million from that line for “post-closing activities.”

Other steps the company is taking including a cut to capital expenditures. CFO Eric Peterson said on the call that capex this year will be cut to $100 million to $120 million from an earlier projection of $140-$150 million. The company already spent about $67 million of that in the first quarter, so its capex the remainder of the year might be as little as $35 million.

“We remain confident in our ability to weather a severe downturn as a result of the pandemic,” Peterson said.