U.S. Xpress broke out metrics for its Variant initiative for the first time, and one of the key selling points for Variant — lower driver turnover — deteriorated sharply over the course of the year.

In an overall fourth-quarter earnings report that had little good news, U.S. Xpress reported that its quarterly turnover for Variant had worsened to 95% by the final three months of the year. That marks a significant slide from quarterly turnover that was 58% in the first quarter, 74% in the second and 81% in the third.

In breaking out various Variant data points, U.S. Xpress (NYSE:USX) did note that the turnover for the legacy business in 2019 was 150%.

Variant also saw a yearlong decline in its average revenue per tractor per week. After recording figures of $3,764 in the first quarter, that benchmark rose to $4,000 in the second quarter. But it declined to $3,929 in the third quarter before dropping further to $3,740 in the fourth quarter. Annualized, average revenue per tractor per week was $3,861.

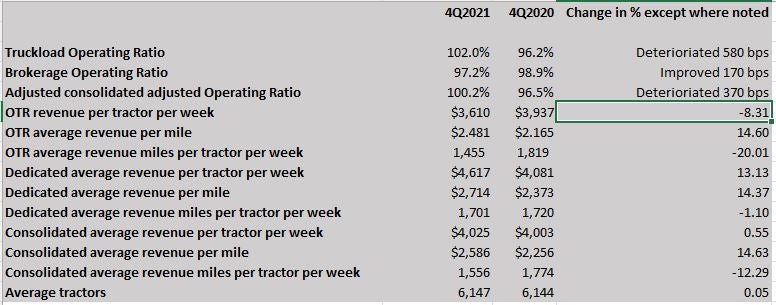

However, both the quarterly and the annual figure for Variant are better than the overall company average. The over-the-road segments posted average revenue per tractor per week of $3,610 for the quarter and $3,732 for the year, compared to the Variant-only numbers of $3,740 and $3,861.

The earnings report was already likely to have been revealing, given that U.S. Xpress announced in December that the president of Variant, Cameron Ramsdell, had been fired. No reason for his ouster was provided at the time, with the news coming in a Securities and Exchange Commission filing.

CEO Eric Fuller has touted the growth of the Variant fleet and said at a Stephens conference in early December that Variant was about to hit 1,500 trucks.

“During the second half of 2021, Variant’s turnover, utilization and revenue per tractor per week began to deteriorate, and these trends accelerated in the fourth quarter,” Fuller said in the prepared statement accompanying the earnings release. He noted that since Ramsdell’s dismissal — though he wasn’t identified by name — Variant’s team reports directly to Fuller.

On the earnings call with analysts, which had a relatively light turnout compared to recent calls, Fuller and CFO Eric Peterson both declared several times that their belief in the fundamental technology-driven model of Variant had not altered. Fuller didn’t flinch when confronting a question from Scott Group of Wolfe Research, who raised the specter of “strategic alternatives for the business,” a not-surprising scenario given that the U.S. Xpress stock price is down roughly 65% from its 52-week high of $12.33 posted March 31. U.S. Xpress stock closed Wednesday at $4.42 but at 5:30 p.m. was down more than 14% aftermarket to $3.80 following the earnings release.

“We believe in what we are doing,” Fuller said. “Things are going to look a lot better and as long as we see this we are going to be very optimistic.” He added that he expected to see sequential earnings improvements going forward.

Fuller, addressing the deterioration in Variant’s metrics over the second half of the year, focused on several issues. Among them, the “optimizer” — the technology tool that is at the core of the Variant initiative to drive freight efficiency — was not being used for all freight. Another issue Fuller said management found: The technology-focused Atlanta team “kept working on longer-term solutions but not on the short term.” The result was “an inability to resolve driver issues.”

Both Fuller and Peterson stressed several times during the call that the overall growth at U.S. Xpress’ fleet was significant. While year-over-year total tractor count was up just three, to 6,147 from 6,144, sequentially the tractor count was up from 5,944 in the third quarter.

The multiyear loss in tractor count that U.S. Xpress has experienced, Peterson said, was to be expected, given the decision to stop investing in the legacy truckload business and instead make Variant the focus of the company. The problem is that the fixed cost structure at the company then was supported by a smaller number of tractors. But Peterson added that various fixed cost metrics will decrease as the company grows its fleet.

U.S. Xpress’ base of technology and other systems has the ability to take on an additional 2,400 tractors, Peterson added.

Several times during the earnings call, Fuller and Peterson said that results at Variant improved in January following the management team’s immersion in its operations.

“Since the change, Variant’s key metrics have improved, including revenue per tractor per week which averaged approximately $4,100 over the last four weeks, an improvement relative to third and fourth quarter results,”Fuller said in the statement, also noting cost reductions at Variant of more than $10 million on an annualized basis.

Overall, it was not a good quarter financially for U.S. Xpress. In a quarter during which several truckload companies reported strong earnings, U.S. Xpress had an operating loss of $5.11 million, compared to an operating profit in the fourth quarter of 2020 of $15 million. For the year, operating income at the company fell to $18.4 million, down from $43.55 million a year ago.

And where some truckload companies were able to report operating ratios in the low 80s or even high 70s, U.S. Xpress’ truckload OR was 102%, a significant deterioration from the 96.2% OR of a year ago. For the full year, U.S. Xpress’ truckload operations just managed to turn in a positive OR of 99%, but that is down from 96.5% a year ago.

The brokerage group’s OR, which has been a focus of Fuller and U.S. Xpress management, improved compared to last year, moving up to 97.2% from 98.9% a year ago. It was also a sequential improvement from the 101.6% posted in the third quarter.

Costs at U.S. Xpress overall surged in several categories. In the key metric of salaries, wages and benefits, costs rose to $174.53 million, up 21.5% year over year. Purchased transportation also climbed, rising 23% to $175.97 million from $143 million.

The overall rise in expenses was 21.8%, to $536 million. The fourth-quarter increase was of a far greater percentage than the 13.6% increase posted for the entire year.

And in an industry where several truckload carriers posted big increases in their cash on hand over the course of 2021, cash at U.S. Xpress rose to just $5.69 million from $5.5 million over the 12 months. By contrast, Marten (NASDAQ: MRTN) rose to $83.9 million from $66.1 million, and PAM Transportation (NASDAQ: PTSI), which has always had an unusual balance sheet that held little cash, went from under $1 million to more than $18.5 million.

Variant also has been cited as leading to fewer accidents, but that benchmark got worse over the course of the year. Fuller said the company had two serious accidents in the quarter, but he did not specify on the earnings call whether they were Variant trucks.

However, the Variant accident performance is still far improved over the legacy business. Preventable accidents per million miles was 5.56 in the fourth quarter, improved sequentially to 5.44 but worsened to 6.82 by the fourth quarter. But the 2019 legacy business was 12.1.

Ramsdell’s name did not come up on the call. In response to a question from Stevens analyst Jack Atkins, Fuller said he and Peterson have been working almost full time with the Variant technology and development team in Atlanta. And he said while keeping the team in Atlanta is planned, further integration with the rest of the U.S. Xpress team will be required.

Variant was producing solid numbers until the summer, Fuller said, and he expressed the possibility that Variant had matured enough that greater integration within U.S. Xpress might have been called for earlier. “In hindsight, maybe we should have gotten down here quicker,” Fuller said of Atlanta.

Peterson, responding to a question about getting the company’s OR down toward the 90% level, said the Variant initiative has had “hurdles along the way and it has made our timeline go out a little longer.”

“But we still believe that longer term this is going to get us into the lower 90s and then into the 80s,” Peterson said. But he added that he could not give a “good timeline” on when that might occur.

U.S. Xpress ranks 13th on the FreightWaves 500.

Disclosure: FreightWaves founder and CEO Craig Fuller retains ownership of U.S. Xpress shares through his family trust.

More articles by John Kingston

CEO predicts Variant will drive USX sequential financial growth by Q1

USX’s 3Q was weak but analysts appear open to CEO’s long-term view

U.S. Xpress inflection points reached with over 900 carriers carrying Variant brand