ArcBest saw continued volume pressure in the fourth quarter as it transitions its less-than-truckload business away from transactional shipments to loads from its core customers following Yellow’s shutdown. The mix change has been a headwind to revenue but supportive of margins.

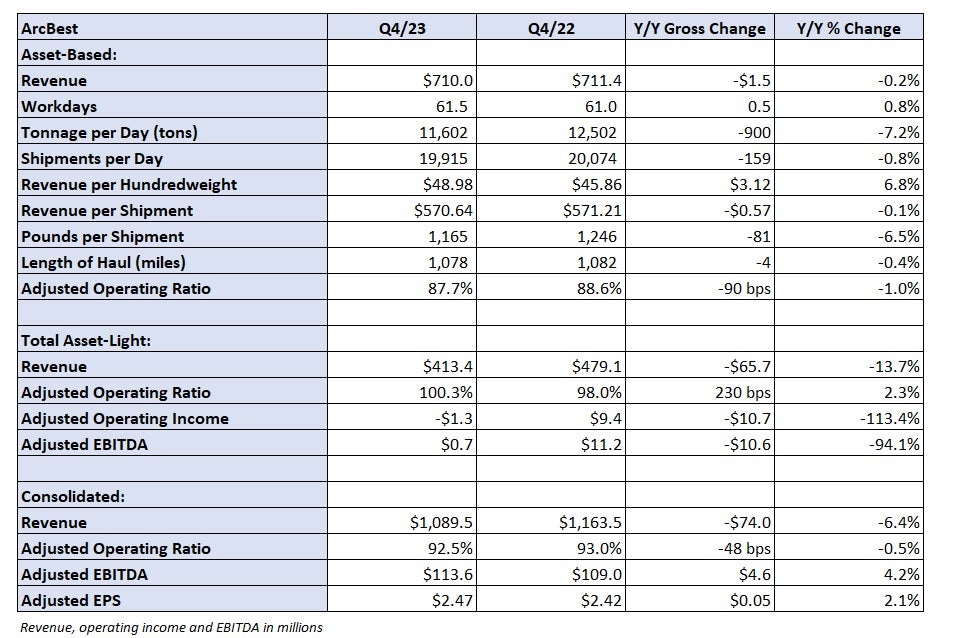

ArcBest (NASDAQ: ARCB) reported adjusted earnings per share of $2.47 on Tuesday ahead of the market open, which was 26 cents better than the consensus estimate and 5 cents higher year over year (y/y). The number excluded some nonrecurring items like costs from a freight handling pilot, acquisition-related expenses and settlement charges from a worker classification lawsuit.

The company leaned more heavily on a dynamic pricing model amid sagging industrial demand last year. The tech-based strategy identifies available network capacity on a daily basis and prices those lanes to attract incremental shipments through spot transactions.

However, Yellow’s departure took out roughly 7% of the industry’s capacity (closer to 9% share before its customers began seeking other carrier options early last summer). Its shutdown has allowed carriers to capture more higher-margin freight from core customers.

During the fourth quarter, ArcBest reported that tonnage per day in its asset-based segment, which includes less-than-truckload operations, fell 7.2% y/y as shipments were off 0.8% and weight per shipment was down 6.5%. By month, tonnage was down 4% y/y in October, 9.6% in November and 8.3% in December.

In January, ArcBest’s tonnage declined 18%, but the company said inclement weather was more impactful this year than in the past. The carrier had 130 terminal closures during the month compared to a 10-year average of 57. It normally sees 174 closures in total during the first quarter.

When stacking the change rates from the past two years, January tonnage was down 16.4%, a modest improvement from a 17.7% decline in December. The slight improvement in the face of more severe weather trends may indicate that the worst of the declines have passed. Shipments per day were roughly 19,000 in both months.

Shipments and tonnage from its core customers were up 8% and 6% y/y, respectively, in January.

The freight transition helped push revenue per hundredweight, or yield, 6.8% higher including fuel surcharges during the quarter. The metric was nearly 4% higher sequentially from the third quarter. The company said yields on LTL-rated shipments increased by double-digit percentages excluding fuel.

ArcBest will continue to pursue a long-term growth strategy, but it isn’t taking the big capacity leap like some peers. The company said it has roughly 15% to 20% latent capacity in the network and plans to add 347 doors in 2024 after adding 299 last year. It recently acquired four terminals with 77 doors for $38 million from Yellow’s estate. ArcBest has increased door count by 9% since 2021.

Between the new sites and operating efficiencies gained from the mix shift back to core accounts, the goal is to achieve a mid-single-digit annual growth rate moving forward. The current real estate plan can accommodate 25% growth longer term, the company said.

Saia (NASDAQ: SAIA) said last week it was more than doubling capital expenditures in 2024 after recently inking deals to acquire 28 terminals from Yellow’s estate. Those sites were acquired for $244 million, which is just half of what the carrier plans to spend on real estate projects this year. In total, the company expects to expand its door count by 12% to 14% this year. It has 20% excess capacity currently.

Old Dominion Freight Line (NASDAQ: ODFL) reported it has 30% available door space in the network. It plans just four or five additions this year but will leverage $2 billion in real estate investments over the past decade to onboard more shipments.

During 2023, ArcBest participated in 90% more LTL bids and its win rate increased by 150%. Yield was down 2.2% y/y during the year, but included a roughly 15% reduction in diesel prices as well as the shift in mix.

“I’m really pleased with the strength of our core business, the opportunities that we’re seeing in terms of bids and our win rates,” said Judy McReynolds, chairman, president and CEO, on a Tuesday call with analysts. “That’s helpful as we think about the rest of 2024.”

Q4 by the numbers

Consolidated revenue of $1.09 billion was 6.4% lower y/y.

The asset-based segment reported $710 million in revenue, which was down 0.2% y/y. The declines in tonnage were largely offset by higher yields. Pricing on contract renewals and deferred agreements increased 5.6% y/y on average in the quarter.

The asset-based unit recorded an 87.7% adjusted operating ratio, which was 90 basis points better y/y and 110 bps better than in the third quarter. The sequential improvement was driven by a variety of cost initiatives and in line with management’s expectations (100 bps to 200 bps of improvement) compared to normal sequential deterioration of 100 bps to 300 bps.

Rents and purchased transportation expenses were down 370 bps as a percentage of revenue. The salaries, wages and benefits line was up 330 bps largely due to a new labor contract with its union workforce.

Asset-based revenue per day was 7% lower in January given the large, weather-induced tonnage decline, which was only partially offset by a 13% increase in yield. Daily shipments and weight per shipment were both down 9% in the month.

The asset-light unit, which includes truck brokerage, reported a 13.7% y/y revenue decline to $414 million. Daily shipments increased 12.4% y/y, but revenue per load was off, in the mid-20% range. The unit reported an adjusted operating loss of $1.3 million.

January revenue in the segment was down 15% y/y, with an 11% increase in shipments being offset by a 23% decline in revenue per load.

The company expects net capital expenditures of $325 million to $375 million in 2024 compared to $245 million last year. The new capex budget includes $155 million in rolling stock and $130 million in real estate projects. The company will also invest in technology and upgrade dock equipment.

Shares of ARCB were up 9.8% Tuesday at 1:35 p.m. EST compared to the S&P 500, which was up 0.1%.