Shipping busts can be even more exciting than shipping booms. When spot rates crash, debt comes due, vessels are arrested, bankruptcies pile up and vultures swoop in.

But not all shipping collapses are so action-packed. Sometimes things never devolve into total crisis mode. Sometimes the market gets stuck in limbo — like tankers are now.

Tanker rates have wallowed at or near historic lows throughout 2021, weighed by oil inventory destocking, COVID-struck demand and a stubborn aversion to scrapping older ships. The market is “the worst this business has seen for more than 30 years,” conceded Svein Harfjeld, co-CEO of DHT (NYSE: DHT) on his company’s quarterly call on Wednesday.

According to Clarksons Platou Securities, pre-2015-built very large crude carriers (VLCCs, tankers that carry 2 million barrels of oil) and Suezmaxes (tankers that carry 1 million barrels) were both earning just $6,900 per day as of Thursday. Rates for pre-2015-built LR2 product tankers (with capacity of 80,000-119,000 deadweight tons) had collapsed to $5,600 per day, down 75% month on month.

Yet there has been no wave of distress tanker sales or bankruptcies, as seen in past slumps. Tanker owners in the current downcycle had pared their financial leverage over the past decade and refilled cash cushions on strong rates in late 2019 and early 2020.

No distress yet

“We’re not seeing a distress situation. That’s for sure,” said Euronav (NYSE: EURN) CEO Hugo de Stoop on Thursday’s quarterly call. “Let’s not forget we’re just a few months past one of the best years tanker shipping has ever gone through. You cannot go from that situation to a distress situation in a few months.”

This also limits the number of secondhand ship sales compared to past rate depressions. “We, together with other people, have picked up pretty much everything that there was to pick up in the market,” said De Stoop.

He explained, “Some people who are not distressed are interested in selling their vessels simply because they look at what they’ve earned and what the prospects are and there’s this unknown factor of when the market is going to return to better territory. And they just don’t want to guess. They prefer to take their profit and leave the market.

“The problem there is that the [ship] values are going up way ahead of earnings, so it’s difficult to meet the bid-offer spread on many of those assets,” said De Stoop.

According to Harfjeld, “Values, or at least sellers’ asking prices, have moved up a bit quicker than we had hoped, leaving us in a wait-and-see mode for now.”

Limited scrapping (so far)

In addition to distress sales, tanker rate slumps usually see accelerated vessel scrapping. The current cycle is different.

If rates are as low and steel prices are as high as they are now, owners of older tankers would normally sell their ships for scrap en masse. That, in turn, would help bring vessel supply and cargo demand back toward balance.

Executives of both DHT and Euronav maintained that scrapping is being held back by lucrative rates for older tankers carrying oil for Iran and Venezuela.

Harfjeld said, “A lot of the old fleet is today engaged in trades that are sensitive in nature — with the embargoed oil. They’re getting paid quite handsomely to freight that oil and the oil is discounted, so the economics work for both the seller and the buyer of oil. We think that if some of these sanctions are lifted, you would very likely get a more normalized pricing dynamic on the oil side and that means [shippers] could not afford to pay these fantastic rates the old ships need. That would certainly leave these old ships without employment to a large degree, and then the option would be to start to scrap.”

Brian Gallagher, head of investor relations at Euronav, cited data showing that up to 54 VLCCs and 20 Suezmaxes are involved in Iranian trade, and 8% of the world’s VLCCs and 5% of Suezmaxes in the Venezuela trade.

Gallagher said the tankers in what he called the “illicit trade” all tend to be at least 17 years old, with little or no insurance or vetting, and have been sold from “reputable owners” to “private hands” since 2019. If these trades were “legitimized” through removal of sanctions, “a lucrative trade today would disappear tomorrow … and given high scrap prices, it’s a natural assumption that they would disappear.”

Container orders will block tanker orders

The low orderbook is one of the optimism drivers for tanker trades in 2022-23. Tanker tonnage on order is just 9% of the tonnage on the water.

Tanker rate recoveries precipitated a surge in new orders in past cycles. Assuming tanker demand recovers from COVID in 2H 2021 and 2022 (which remains hypothetical), this cycle should look different. Yard slots are filling up with orders for new container ships as that market booms. This will sharply limit ability to place future tanker orders.

According to De Stoop, “Only a handful of yards can build VLCCs and those are the same yards that build container ships and gas carriers. With profitability surging, we’ve seen the container segment order more than 10% of the world fleet [tonnage] in the last five months. That’s very impressive. That means the yards you would order VLCCs from are extremely busy.

“Also, we’ve already seen the first wave of LNG [liquefied natural gas] carrier orders and there’s another wave coming. Especially the Qataris, who are going ahead with the idea of building 50 option 50 [50 firm orders plus 50 options]. You can understand what that does to the orderbooks of the yards.

“But let’s not forget that yards need to retain the capability of building different types of vessels. If you have no tankers in your orderbook, you lose your know-how and some of the workers will leave. So, they will always have some slots available for building tankers.

“I’m not saying that the orderbook is full off container ships through 2025 so therefore it’s full for everybody. That’s wrong. But the number of tankers you can build [will go down]. I’m not saying you’re not going to see orders placed [for tankers] for late 2023 or 2024 for delivery. But I am saying that the capacity to overbuild is very much impaired because they’re receiving so many orders — and will likely be receiving many more orders — for the container and LNG sectors.”

Tanker earnings roundup

On Wednesday, VLCC owner DHT reported net income of $11.6 million for Q1 2021, down from $72.2 million in Q1 2020. Earnings per share of 5 cents came in above the consensus forecast for 3 cents. Of all the tanker companies, DHT had the most time-charter protection from depressed spot rates. Harfjeld stressed on the call, “You should not expect us to contract newbuildings.”

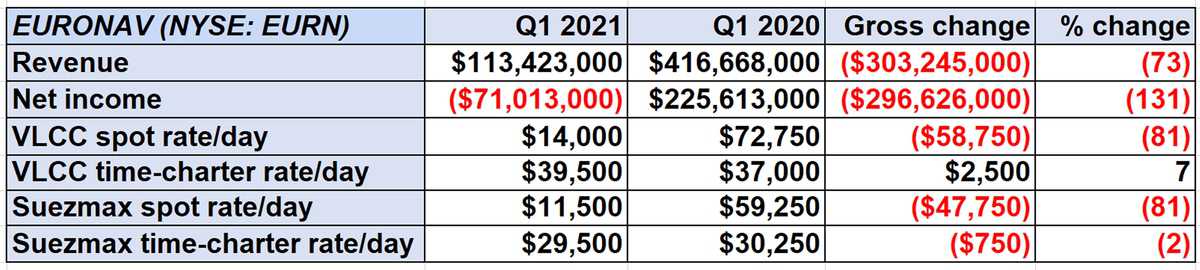

On Thursday, VLCC and Suezmax owner Euronav reported a net loss of $71 million for Q1 2021 compared to net income of $225.6 million in Q1 2020. The loss per share of 36 cents matched the consensus forecast.

Last month, Euronav ordered two VLCC newbuildings (with an option for a third) for deliveries in Q4 2022 through Q2 2023. It acquired two Suezmax resales in February for deliveries in January 2022.

Also on Thursday, crude and product tanker owner International Seaways (NYSE: INSW) — which recently announced a merger agreement with Diamond S Shipping (NYSE: DSSI) — reported a net loss of $13.4 million for Q1 2021 versus net income of $33 million in the same period last year. The loss per share of 48 cents was significantly better than the consensus forecast for a loss of 62 cents.

International Seaways signed contracts in March for three dual-fuel VLCC newbuilds that will be chartered to Shell for seven years after deliveries in 2023.

Click for more articles by Greg Miller