Editor’s note: This story has been updated throughout to reflect President Trump’s announcement of new tariffs against China.

With August now beginning, it is reasonable to ask, given air cargo’s soft performance this year, what is the outlook? Does the new month bring any month-to-month seasonal improvement in either U.S. import or export volumes compared to what we have just seen for July air cargo levels?

While we are facing unique global trade and tariff pressures this year with various U.S. trade negotiations underway, up until today (August 1), no specific tariff actions or threats were on the immediate horizon that would drive air cargo one way or another appear imminent for August. However, President Trump’s August 1 announcement of a 10 percent additional tariff on the remaining $300 billion of Chinese imports, effective September 1, potentially changes the dynamics for air cargo, at least in one major air cargo market. A “beat the tariff” surge in air freight shipments from China and Hong Kong to the U.S. towards the end of August could well boost air cargo volumes and pricing in the short-term, but make for a slower fourth quarter peak season.

Normally August is a slower air cargo month for the trans-Atlantic trade, with many European companies in particular reducing operations for summer holidays. Much of the U.S. produce export season from the West Coast is completed or winding up, and it’s early for Asian markets to be upgrading to air freight to North America for new products or major releases. No major port slowdowns or major airline labor actions are occurring that would cause buy-up to air cargo or tighten capacity.

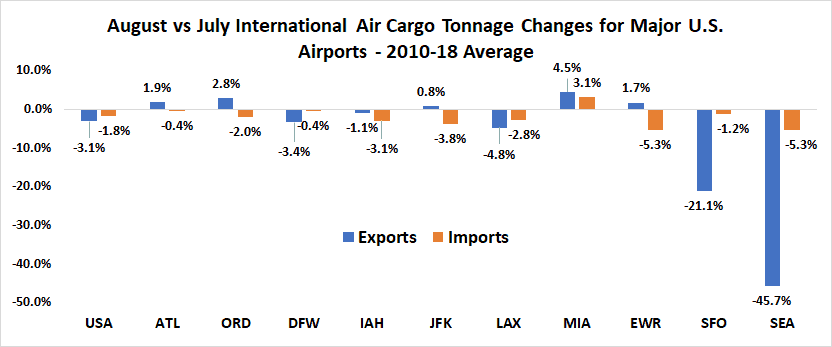

We still have many years of history for both July and August air cargo traffic history to fall back on and use for initial guidance. The chart below reflects U.S.-wide figures for international air cargo and helps simplify the answer. U.S. export volumes by air have slipped in August compared to July in eight of the last nine years, averaging 3.1 percent lower each year, and increasing only once six years ago. Imports have shown a bit more volatility with sharper lows and higher highs. Still, seven of the nine years saw imports fall off in August, averaging 1.8 percent lower each year. But in two of the last three years, we did see an increase, though 2018 was only 0.5 percent higher than July during a strong inventory stocking phase.

While U.S. overall averages suggest slightly less cargo and opportunities for the trucking industry, individual airports can and do vary a bit. The lower chart compares these U.S. averages since 2010 along with those for 10 major U.S. airports. For Seattle (SEA) and San Francisco (SFO), the end of the primary produce shipping season in July and early August triggers the most dramatic export falloffs shown, but five other U.S. airports (Atlanta-ATL, Chicago-ORD, New York-JFK, Miami-MIA, and Newark-EWR) actually average very small August export increases compared with July. For imports though, all of the top airports shown, excluding Miami, align with the overall U.S. pattern, averaging low-to-middle single-digit August international cargo decreases.

The major airport bucking the overall U.S. trend for August has been Miami, which not only shows August growth on both air exports and air imports, but has improved month-over-month in all nine years reviewed, except 2011. Miami’s Latin hub focus gives it a different traffic mix, with far less dependency than other U.S. airports on China air cargo. Miami’s August import increases averaged 3.1 percent, driven largely between ever-growing demand for flowers, seafood, produce and asparagus, or perishables such as berries coming into season. Export increases averaging 4.5 percent cover a full spectrum – parts for aircraft, computers, automobiles, cell phones, medical equipment and machinery. Miami acts as the primary air gateway for the growing Latin American region.

Given today’s global economy and trade outlook under a higher stress level we would expect under normal conditions that August 2019 U.S. overall performance to be at or below historic averages shown above. That means on balance less traffic to truck to and from most airports compared with July, and more open space opportunities on airlines.

However, any accelerated inventory stocking of Chinese products by air this month could push import tonnage into positive growth territory for some big China-cargo gateways such as Chicago, Los Angeles, New York and San Francisco. Miami stands out as the airport most likely to grow on its own over July without a push because of higher China tariffs. Getting past the summer holidays, Labor Day and potential short-term demand surges is key for any real sustained air cargo recovery this year.