Until very recently, the narrative in the tanker market went like this: The coronavirus has destroyed oil demand, excess oil will be forced into storage on tankers, a huge portion of the fleet will be tied up for an extended period, far fewer ships will be left in the spot market, ergo rates will rise.

Sure, the lengthy and inevitable storage drawdown will be painful for rates, but that’s the future. The near term looks great and tanker stocks are trading at a discount, so buy the stocks.

The new tanker story goes like this: Oil demand is coming back fast, floating storage has peaked, oil already stored on tankers will be drawn down much quicker than predicted, rate pain during the drawdown period will be less prolonged than expected, market dynamics will revert to old-fashioned supply versus demand, demand will exceed constrained supply, ergo rates will rise.

Sure, rates will be down in the near term, but the future looks great and tanker stocks are trading at a discount, so buy the stocks.

The latest evidence of this shift in viewpoint came during the quarterly conference call of tanker giant Frontline (NYSE: FRO) on Wednesday.

Destocking dead ahead

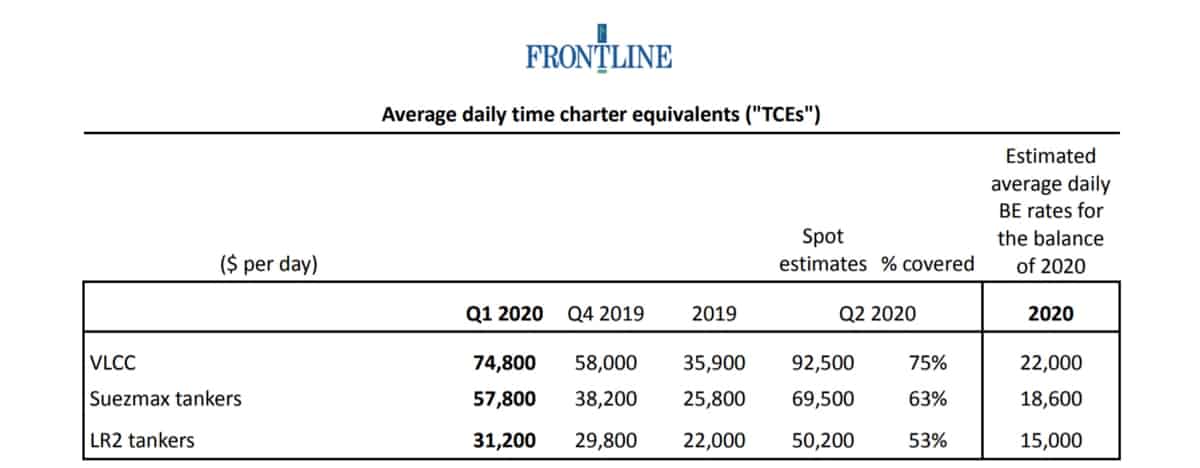

Frontline reported net income of $165.3 million for the first quarter of 2020 — its strongest performance since 2008 — versus net income of $40.1 million in the first quarter of 2019. Adjusted earnings of 95 cents per share came in just above the consensus forecast for 93 cents per share.

Frontline CEO Robert Macleod had been a particularly vocal proponent of the floating-storage investor pitch. During a Capital Link forum in March, he proclaimed that floating storage had transformed the tanker market from a “once-in-a-decade situation” to a “once-in-a-lifetime situation.”

On the latest call, however, he conceded that “we may be close to the [storage] peak.” He added, “We expect to see an unwind of floating storage during the balance of 2020, with Aframaxes [tankers that carry 750,000 barrels of crude] in Europe likely to be the first to unload — some already have.”

Unloading timing for cargoes stored aboard very large crude carriers (VLCCs; tankers that carry 2 million barrels of crude oil) remains uncertain.

According to Macleod, “Some of the VLCC cargoes are likely to be stored through the second and third quarters because some were bought by the traders at heavy discounts. I would guess that some of the traders have hedged out the front of the curve, they believe in demand really coming back, and they’re waiting for the curve to strengthen. There are people with oil in floating storage who are deep, deep ‘in the money,’ and some of them might be willing to take the risk of moving even deeper.”

Executives of Euronav (NYSE: EURN) previously maintained that most VLCCs used for floating storage are on six-month time charters, limiting negative impacts on spot rates. Macleod poked a hole in this argument.

The charterer in a six-month time-charter contract “would still have the obligation to keep the vessel on hire and pay us hire until the earliest redelivery date,” he explained. But if charterers unloaded the stored oil early, “they would then trade the ships in the spot market. Many of the guys who have put ships on storage are very familiar with the spot market, having ships themselves, so they would go from being on storage to being normal spot players.”

That transition appears to be beginning. Clarksons Platou Securities warned on Thursday morning, “Brokers said a time-chartered [VLCC] to an oil company was relet in the spot market at a lower rate than last done. At the moment rates are holding steady but if further oil company relets come to market, a strong resolve from independent ship owners may not be enough to hold the market up.”

What changed?

The reason the tanker story was rewritten so quickly: oil demand, which appears to be rebounding rapidly. Macleod, who stated in March that “what we’re seeing is a complete destruction of oil demand in the world” recanted and said on Wednesday that “‘suppressed’ describes the situation more accurately than ‘destroyed.’”

“There have been surprises in recent weeks. Chinese gasoline demand is now above 2019 figures and recent figures from India also show a sharp recovery in gasoline sales,” he said.

“My guess is that the demand destruction was not as deep as the analysts were projecting,” he continued. “I think the return is coming quick. It looks like Asia’s coming back. It could mean the pickup [in demand] is indeed a ‘V,’ but we’ll have to see.”

Analysts at Fearnleys made similar comments in a market outlook published Wednesday. “The quick rebalancing in the oil market has taken most by surprise. The price jump is a result of factories across Asia’s largest economy restarting and people returning to work, with some favoring their cars over taking public transport,” wrote Fearnleys, adding, “Crude processing at China’s independent refineries is now higher than pre-virus levels, while fuel demand is also starting to rebound in India.”

Recent cuts to oil production — which have been negative for tanker rates — could be reversed if demand bounces back fast enough. “This is pure speculation but given recent news on the demand side, we could see production cuts reverse as early as the second half of 2020,” said Macleod.

Ripping off the Band-Aid

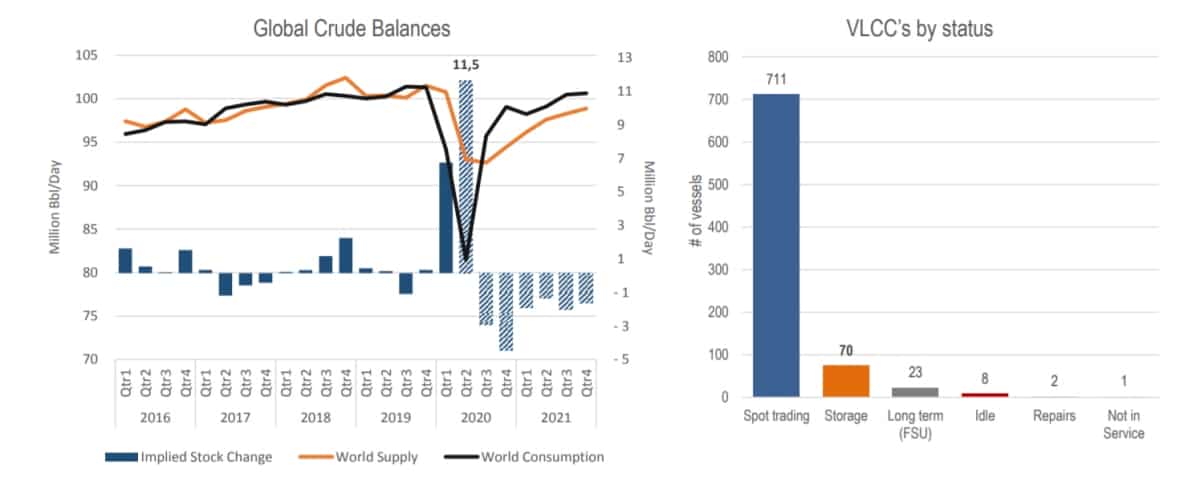

As floating crude and products are unloaded from storage, there is less need for tankers to transport oil across the oceans from producing countries to consuming countries — the consuming countries already have what they need from storage.

Weaker tanker rates are inevitable; the best-case scenario is to rip off the Band-Aid as quickly as possible.

According to Macleod, “A month ago, we thought the peak in the storage of oil was going to be at a much higher level. We expected the crude price to be low and the contango to be strong for longer, and the negative of that is that we are not enjoying the prolonged freight spike we had expected.

“But the flip side of that is that the volume of the crude inventory drawdown — which everyone has been talking about for the last month or two as a sort of big animal that would destroy the whole market — will be less. And that means it will be a shorter period until a return to a more normal freight market.”

Cross-country trek ahead?

VLCC rates have fallen from all-time highs of over $200,000 per day in early April to $49,500 per day as of Wednesday. Brokers foresee further declines.

The greatest risk to VLCC rates should come at the peak of the destocking phase, when traders are unloading the highest number of cargoes and injecting the most ships back into the spot market.

The timing of peak destocking could have personal implications for Macleod.

At the height of the rate frenzy, he bet an analyst that VLCC rates would not revert to the $20,000- to $30,000-per-day levels seen in February at any point during the second or third quarter. Macleod vowed that if he lost the bet, he would walk the entire 300 miles between Oslo and Bergen, Norway.

“To put it mildly, I’m very confident with that bet. I don’t think there will be any walking across the country,” he affirmed during a podcast on April 23 with analyst J Mintzmyer of Seeking Alpha’s Value Investor’s Edge.

Less than a month later, it looks increasingly likely that Macleod could need a new pair of Nikes. More FreightWaves/American Shipper articles by Greg Miller