In the COVID era, tanker markets change more quickly and the past is not necessarily prologue. What really matters in quarterly reports is what executives say about the present and future, not what they say about a quarter ending over a month ago.

Two of the world’s largest public tanker owners — Euronav (NYSE: EURN) and Scorpio Tankers (NYSE: STNG) — reported results on Thursday. Two key takeaways emerged from their conference calls.

First, floating storage is coming down from its peak, faster for refined products than for crude oil. Second, the medium-term vessel-supply picture looks increasingly attractive.

Crude storage unwind

Floating-storage demand spurred a rate boom in the first half. But after the party comes the hangover. When charterers unload storage, tankers reenter the spot market.

Euronav execs had expected the floating-storage party to last longer than it did.

“A number of VLCCs [very large crude carriers; tankers that carry 2 million barrels of crude] were and still are being used as storage units. But far fewer than what many analysts and we had predicted,” conceded Euronav CEO Hugo de Stoop.

According to Brian Gallagher, Euronav’s head of investor relations, crude floating storage peaked at around 200 million barrels in May. About half was aboard VLCCs, the other half on smaller tankers. Euronav had thought storage levels would rise “substantially higher,” but “this didn’t materialize” due to rapid production cuts by OPEC+, Saudi Arabia individually and the U.S., said Gallagher.

Of VLCCs tied up by floating storage, congestion or other reasons, Gallagher estimated that 60-80 would return to the trading fleet in the near term. This will happen “progressively, not immediately. But nonetheless, it does provide a headwind for owners as we move toward the latter part of the year.”

So far, crude-tanker destocking has not caused severe rate pressure. According to Clarksons Platou Securities, VLCC rates were $21,900 per day as of Thursday, roughly unchanged from $21,600 per day one year ago. Suezmax rates were $14,900 per day, not far below where they were a year ago — $15,300 per day.

Products storage unwind

There was a “surge in demand for product tankers to be used as floating storage” in the second quarter, pushing rates to “unprecedented levels,” said Lars Dencker Nielsen, commercial director of Scorpio Tankers.

“The destocking of that floating storage has occurred much faster than many anticipated,” he reported. Floating products storage peaked at 105 million barrels in May and was down to 45 million barrels last week.

The bad news is that rapid destocking and low refinery utilization push down spot tanker rates. The good news is that the floating-storage hangover for product tankers should be short.

Also, the storage-unwind headache is not as painful as predicted, said Scorpio Tankers President Robert Bugbee.

During the May conference call, “we were at peak fear related to COVID-19,” he recalled.

“There was terrible concern that in the third quarter, with destocking, demand would just completely diminish and earnings would go to zero. Rates would go negative and cash would be pouring out of the company.

“The most comforting thing for us at the moment is that we’ve got a really good start on the third quarter. And the company is cash positive so far. Ironically, we’re doing better than where we were in the last third quarter.

“The spot market is really encouraging. Look at MRs [medium-range product tankers, with capacity of 35,000-54,999 deadweight tons or DWT]. With the amount of destocking that’s happened on MRs, which have gone from something like 87 vessels [on floating storage] all the way down to the low 30s, it’s amazing that the MRs have held up in that way.”

According to Clarksons Platou Securities, rates for MRs on Thursday were $12,800 per day, not far below where they were one year ago — $13,400 per day — despite destocking.

After the storage unwind

Once the destocking phase is complete, the focus will revert to the traditional supply-demand balance.

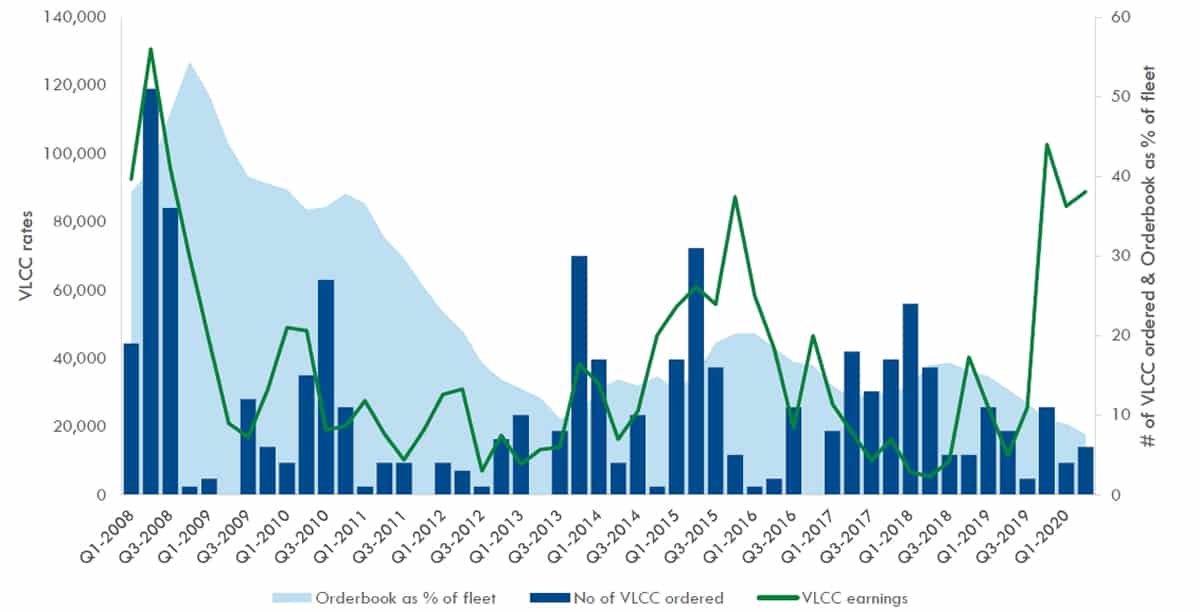

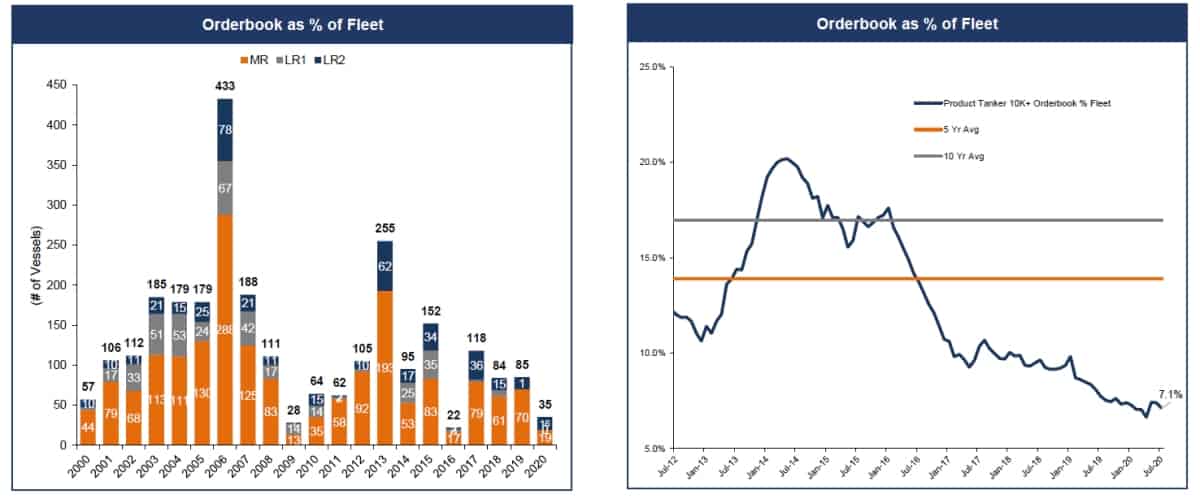

Cargo demand will remain a wild card due to the coronavirus. Vessel supply is more of a known quantity. As previously reported by FreightWaves, orderbooks are near historic lows — a positive indicator on future rates.

“The past three quarters have been the best three quarters for VLCCs from an earnings perspective and yet this has not triggered a rush to the shipyards,” said Gallagher. “This reflects a potent mix of structural, regulatory, financial and environmental factors that, in our view, will continue to keep new ordering at low levels.”

Regarding the on-the-water fleet, Gallagher pointed out that “for both the VLCCs and Suemaxes [tankers that carry 1 million barrels of oil], the average age is at [high] levels not seen in 18 years.” If older ships are scrapped and there are not enough newbuildings to replace them, rates will rise, assuming demand holds.

In the product-tanker market, Nielsen explained, “Fundamentals are extremely strong. There is record low fleet growth of 2% per year or less over the next three years.”

Like Gallagher, Nielsen highlighted the ageing fleet. Including newbuilds on orders, Nielsen said that the share of the product-tanker fleet turning 15 years or older will go from 46% today to 69% in three years for Handymaxes (10,000-24,999 DWT), from 22% to 40% for MRs, from 23% to 51% for LR1s (55,000-79,999 DWT) and from 15% to 29% to LR2s (80,000-119,999 DWT).

Bugbee maintained that in the premium product-tanker sector, it’s not about older ships being scrapped. It’s about older ships being unemployable with top charterers.

“This is something that has been so overlooked. After 15 years, these ships are removed from the premium trade. No other market has a commercial guillotine for 15-year-old ships like the product market,” asserted Bugbee.

Looking back at Q2

Scorpio Tankers reported the best quarterly results of its history on Thursday. Despite this, its share price fell 3% by the closing bell.

It posted net income of $143.9 million for the second quarter of 2020 compared to a net loss of $29.7 million in the same period last year. Adjusted earnings of $2.63 per share were well above the consensus estimate of $2.27.

Scorpio’s MRs earned $21,508 per day in the second quarter, up from $13,436 per day in the second quarter of 2019. It has 45% of its MR available days in the third quarter booked at $15,300 per day.

Euronav reported net income of $259.6 million for the second quarter of 2020 compared to a net loss of $38.6 million in the same period last year. Adjusted earnings were $1.14 per share, matching the consensus estimate.

Euronav’s spot VLCC fleet earned an average of $81,500 per day in the second quarter of 2020, up from $23,218 per day in the second quarter of 2019. The company has 48% of its available third-quarter days for spot VLCCs currently locked in at an average of $60,250 per day.

Given the third-quarter rates booked by both Euronav and Scorpio Tankers, the floating-storage hangover does not appear excessively painful. At least, not yet. Click for more FreightWaves/American Shipper articles by Greg Miller

MORE ON TANKERS: Tanker rate puzzle gets even harder to solve: see story here. How badly did tanker stocks perform in the first half? See story here. “Robinhood effect” spread unevenly across tanker stocks: see story here.