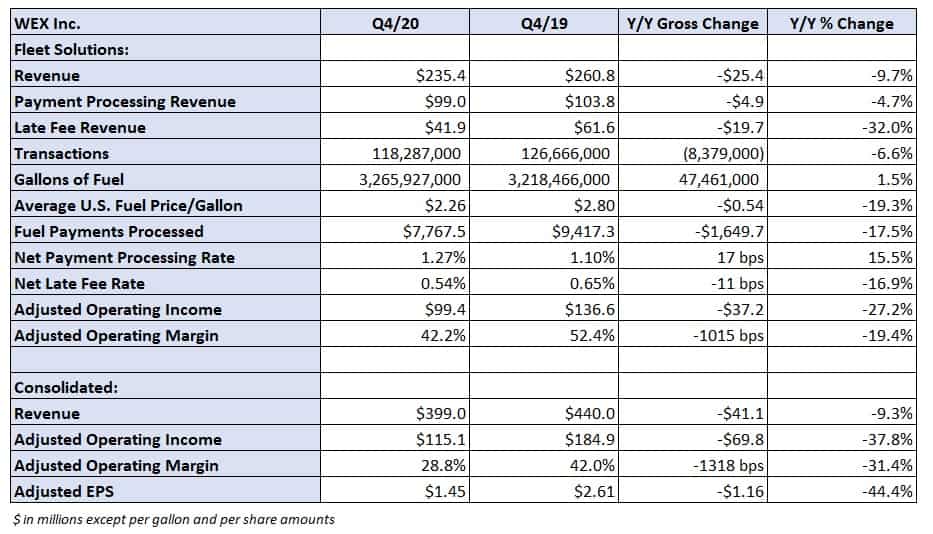

Truck fleet payments and fuel card provider WEX Inc. (NYSE: WEX) reported adjusted earnings per share of $1.45 Wednesday, 2 cents light of the consensus estimate and $1.16 lower year-over-year. The headline number was a loss of $5.30 per share, which included more than $200 million in one-off acquisition-related expenses and a goodwill impairment charge.

The Portland, Maine-based company reported a 9% year-over-year decline in consolidated revenue as activity in the company’s fleet segment declined by a similar amount and revenue in the travel and corporate segment was down 22%.

“The fourth quarter played out better than expected and we began to see some encouraging trends as customer demand slowly returned despite renewed lockdowns across many parts of the world,” said Melissa Smith, WEX’s chair and CEO.

WEX is an electronic payments provider offering fuel, corporate expense and health payments cards. The company’s fleet services include over-the-road fuel cards for trucking, fuel management, factoring, telematics and GPS fleet tracking.

Transactions in the company’s fleet segment were down 7% year-over-year with revenue down 10%. Gallons of fuel purchased increased 2% but was more than offset by a 19% decline in fuel prices during the quarter.

WEX did not provide full-year earnings expectations given “continued uncertainty related to COVID-19,” according to a press release. WEX previously withdrew earnings guidance in May.

However, on a conference call with analysts Wednesday, management said fleet volumes continue to improve sequentially and corporate payments remain strong. Those tailwinds are being offset by depressed corporate travel volumes with unemployment still weighing on payments activity in its health segment.

Over-the road transactions have continued at a positive pace with trucking volumes up 18% so far in the first quarter and gallons of fuel purchased almost 1% higher. Recent weather events resulted in some brief weakness across the network but revenue is expected to be flat to up 2% sequentially in the first quarter.

The high end of the range implies revenue of $407 million, 6% lower year-over-year and $20 million light of the current consensus estimate.

For the full year, management is expecting a “slow and steady” volume recovery in the first half with a more pronounced improvement in the back half, more notably during the fourth quarter. Wider distribution of a vaccine was noted as a catalyst along with improving fundamentals in the health payments unit as new contracts come online.

Management said the long-term revenue growth rate of 10% to 15% remains achievable in the future.

“While the pace of recovery will vary, the anticipated return of volumes from existing customers coupled with new customer additions positions us well to succeed post-pandemic,” Smith continued.

Shares of WEX were 4% lower in early trading Wednesday compared to the S&P 500, which was up slightly.