Forward Air closed 2021 with better-than-expected financial results. The company achieved a “double-double” — double-digit revenue growth (31%) with an adjusted operating margin in the double digits (10%). The first full-year double-double wasn’t expected until 2022.

The Greeneville, Tennessee-based asset-light trucking company has used a tight freight market to swap out lower-yielding e-commerce shipments for heavier loads tied to the industrial tech sector, such as medical devices. “We’ve made a big, big step and we’re not done yet,” Tom Schmitt, chairman, president and CEO, told analysts on a Thursday call.

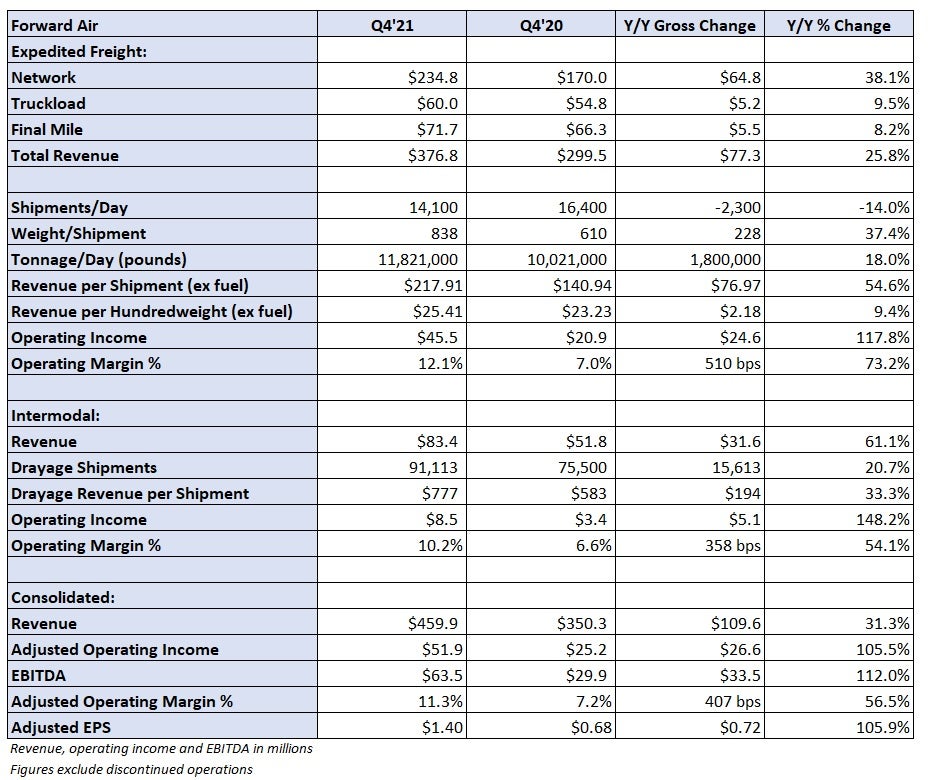

Forward (NASDAQ: FWRD) reported fourth-quarter adjusted earnings per share of $1.40, 11 cents better than the consensus estimate and ahead of management’s guidance range of $1.25 to $1.29. Consolidated revenue of $460 million in the quarter was also 31% higher year-over-year, outpacing guidance for growth between 23% and 27%.

Management said the company is operating ahead of schedule to meet 2023 financial targets, which were just issued on the third-quarter call. The outlook calls for revenue between $2 billion and $2.6 billion (compared to $1.66 billion in 2021) and EPS of $6.30 to $6.70 ($4.43 in 2021). The high end of the range is dependent on M&A deal flow as well as above-plan terminal additions. Forward has completed 14 acquisitions in the past couple of years.

“Based on the continued precision execution of our strategic priorities, at this moment, we are ahead of pace toward our previously announced full year 2023 targets,” Schmitt stated in the press release.

Schmitt said the company is focused on a $10 billion “high-valued freight” subset of the $50 billion less-than-truckload market. Forward’s LTL unit is just shy of $1 billion in revenue or roughly 9% of this subsegment. “If there’s no increase in the pie … then we just need to win the slice-of-pie game.

“When we have a 9% market share, I believe we have a lot of untapped upside, whether there’s economy tailwind as there was in the last year or year and a half or economy headwind. If we can play a slice-of-pie game, we’ll win a slice-of-pie game.”

Q4 results and segment expectations

During the quarter, LTL revenue increased 38% year-over-year to $235 million even as shipments per day declined 14%. Revenue per shipment (ex-fuel) increased 55% as weight per shipment (838 pounds) jumped 37%. Higher shipment weights and a 9% increase in yields, or revenue per hundredweight (ex-fuel), more than offset the lower shipment count. Daily tonnage was 18% higher in the period.

In January, revenue per shipment increased 55% year-over-year with weight per shipment up 33% and tonnage 11% higher.

Total expedited revenue, which includes truckload and final mile in addition to LTL, increased 26% year-over-year to $377 million. The improved revenue metrics and higher pricing drove operating leverage as most expense lines came in lower year-over-year as a percentage of revenue. Purchased transportation (down 150 basis points) and salaries, wages and benefits (down 190 bps) were the biggest movers.

The expedited division posted a 12.1% operating margin, 510 bps better year-over-year.

Looking forward, management expects the LTL margin to improve 150-200 bps this year and next. Improved pricing and full-scale implementation of visibility technology systems and rationalization tools will continue to improve efficiency and reduce operating costs.

Pressed on why the anticipated margin improvement wasn’t higher, Schmitt noted “a pretty good chance” that the freight market will cool in the back half of 2022.

The intermodal segment reported a 61% year-over-year increase in revenue to $83 million as shipments increased 21% and revenue per shipment was up 33%. Higher pricing led the unit to a 10.2% operating margin, 360 bps better year-over-year. Purchased transportation was down 760 bps as a percentage of revenue, with the wages expense line moving 270 bps lower.

Forward issued first-quarter guidance for year-over-year revenue growth in the 18% to 22% range, implying revenue of $435 million at the midpoint, which was in line with the consensus estimate at the time of the print. Management’s adjusted EPS forecast calls for $1.15 to $1.19, which was ahead of the $1.07 consensus estimate and 80 cents reported in the first quarter of 2021.

On Tuesday, the board raised the quarterly dividend by 14% to 24 cents per share.

“So, if you look at all of this together [pursuit of higher-valued LTL freight, onboarding small to midsize shipper customers, cost and tech initiatives, terminal additions, M&A prospects, etc.], we’ve got a ton of untapped upside. We’re on it. I feel extremely confident about the performance potential and I’m very grateful about the performance reality that our teammates and independent contractors made possible,” Schmitt added.

The FREIGHTWAVES TOP 500 For-Hire Carriers list includes Forward Air (No. 37).

Click for more FreightWaves articles by Todd Maiden.

- Maersk adds US final-mile network in $1.8B deal

- Schneider raises margin targets; Q4 ahead of expectations

- Economics 101: Driver pay will keep moving higher