Analysts broke out the superlatives after a blockbuster plan to merge Euronav and Frontline was announced Thursday.

Evercore ISI’s Jon Chappell called it a “mega-merger” that would create a “supersized tanker behemoth.” “A crude tanker powerhouse,” wrote Clarksons Platou Securities’ Frode Mørkedal. Stifel’s Ben Nolan hailed the rise of a “tanker super major,” Deutsche Bank’s Amit Mehrotra, a “tanker juggernaut.”

The stock-for-stock transaction would produce the world’s largest tanker player. It would own or operate 146 crude and product carriers and boast a market capitalization of $4.2 billion.

It would be the highest-value consolidation deal in the history of the tanker industry, and the largest in ocean shipping overall since Cosco’s acquisition of container line OOCL in 2018.

The combined entity would retain the Frontline (NYSE: FRO) name, but “the Euronav [NYSE: EURN] platform would be leading the combined group,” Euronav CEO Hugo De Stoop said in a letter to his shareholders.

Euronav would own 59% and De Stoop would take the helm. Euronav would get three of the seven seats. Hemen Holdings — controlled by shipping tycoon John Fredriksen, Frontline’s founder — would get two (the final two would be neutral). Fredriksen entities would own 21% of the combined group.

Euronav’s shares rose 6.8% in triple average volume on the day of the merger announcement. Frontline’s shares fell 7.7%.

World-leading market share

Clarksons estimated that the combined entity would control 5% of global tanker capacity. That includes 8.1% of the world’s VLCCs (very large crude carriers; tankers that carry 2 million barrels), 9.3% of Suezmaxes (crude tankers carrying 1 million barrels) and 4.9% of coated LR2 product tankers.

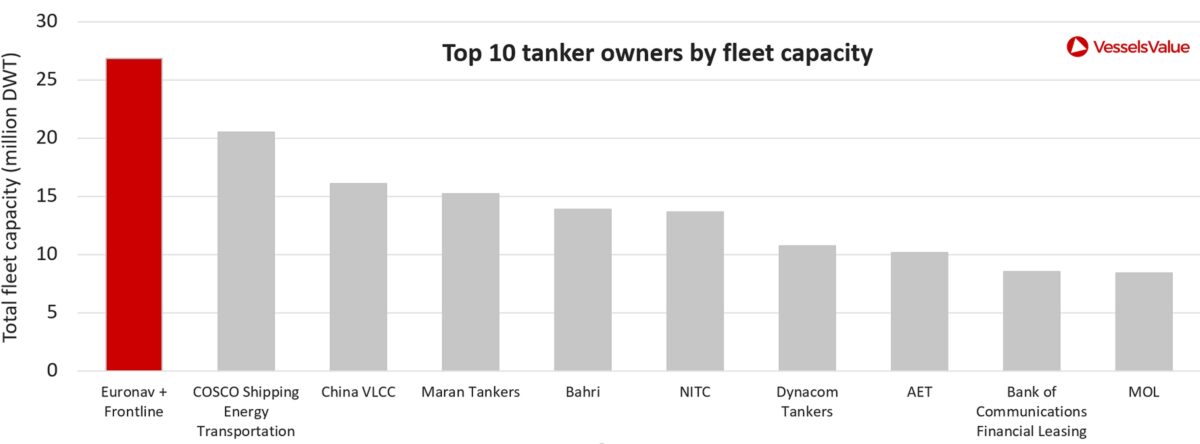

U.K.-based VesselsValue provided American Shipper with its latest data on the top tanker owners. The Euronav-Frontline combo would top the world rankings with 26.8 million deadweight tons (DWT) in owned capacity.

No other top-10 tanker owner is listed in the U.S. The other nine are either private or Asian-listed. In second is China’s Cosco Shipping Energy Transportation with 20.5 million DWT. Third is China VLCC (16.1 million DWT). In fourth is Greece’s Maran Tankers (15.2 million DWT) and in fifth is Saudi Arabia’s Bahri (13.9 million DWT).

Tanker market to remain highly fragmented

Container shipping is vastly more consolidated than tanker shipping. Analysts and consultants generally agree that container liner companies gained pricing power as a result of consolidation. Tanker owners have no pricing power — nor would the Euronav-Frontline entity.

“The spot tanker market is hugely competitive. It is hard to argue for any market power with 8% ownership of the [VLCC] fleet,” said Mørkedal.

The top 10 tanker players own 20% of global capacity, according to VesselsValue. In sharp contrast, the top 10 container liner groups own or operate 85% of global capacity, according to Alphaliner statistics.

Spot tanker rates are driven lower by smaller owners, not those at the top of the rankings, De Stoop said during Euronav’s Q3 2021 conference call. (At the time of that call in early November, Fredriksen had recently acquired a 9.8% stake in Euronav, prompting consolidation chatter that turned out to be correct.)

According to De Stoop, “We were on a panel with Frontline the other night and we both said that what needs to be considered a priority is [consolidating] the smaller players. Those are really the people that are hurting the market. Simply because they don’t have the capacity to gather the information that we do by being present in the market all of the time.

“We think the market will consolidate further. We would like to be a participant. And the priority would be to consolidate the smaller players.”

The proposed mega-merger of Euronav and Frontline — two larger owners that already have high information-gathering abilities — doesn’t do anything to solve the problem of the smaller players. Tanker shipping “will remain fragmented as this merger will not offer material consolidation given the litany of smaller private and public competitors,” said Chappell.

Positives of Euronav-Frontline merger

Nevertheless, analysts highlighted several positives from the proposed mega-deal.

“For tanker investors and for the general investor base globally, the potential combination would create a truly investible tanker company with a meaningful and liquid market cap,” affirmed Chappell. He believes the company “would effectively become a bellwether for not just tanker equities, but maritime transportation as a whole, due to its enhanced scale.”

According to Nolan, “While a combined market capitalization north of $4 billion is still not large, it does help out.” The consolidated entity “will likely have the best share liquidity in the tanker space.”

Mørkedal said that “a larger size should attract larger, long-only funds” and that “larger market capitalization and trading liquidity should improve the cost of equity. But probably more important is improved cost of debt.” Frontline gets loan margins of around 170 basis points over Libor, Euronav 220. “The combined company should likely be able to improve these numbers further.”

Yet despite such “bigger is better” advantages, tanker performance always comes back to how supply and demand affect rates. In tanker shipping — highly fragmented, exceptionally commoditized, heavily reliant on spot business — profits and losses are primarily driven by the vagaries of global market forces outside of management’s control.

“The most important factor, of course, still remains market rates,” said Nolan.

Click for more articles by Greg Miller

Related articles:

- Why Russia-Ukraine war has not ignited crude tanker rates (yet)

- ‘Tricky time’ for shipping stocks: Course corrections ahead?

- How low can tankers go? Analysts slash rate forecasts (again)

- Shipping on Wall Street: Is it better to be a pure play or jack-of-all-trades?

- ‘Gobbling up’ cargo: How crude tankers cannibalized product tankers

- As shipping prospects rise, field of shipping stocks shrinks