New data shows the decline in air cargo business slowed in August, traditionally the weakest month for international carriage of goods by air, raising hopes the upcoming pre-holiday season will be busier than some previously expected amid external forces that are pulling the market in different directions.

The airfreight market last month contracted 5% year over year, and 4% compared to pre-pandemic levels, and shipping rates continued to float downward, following demand drops of 8% in June and 9% in July, according to Xeneta, an ocean and air freight rate benchmarking and data analytics firm. The downturn in air cargo began five months ago, following Russia’s invasion of Ukraine.

Reduced consumer expenditures due to the rising cost of living, slower global economic growth, a continued deceleration in new export orders, airport congestion, and high inventories in some categories for some large retailers are weighing on air cargo activity, analysts and economists say. At the same time, employment rates and wages remain high, U.S. industrial production and consumer demand are still solid, smaller retailers and industrial companies are still rebuilding inventories, and supply chain disruptions are still slowing shipments.

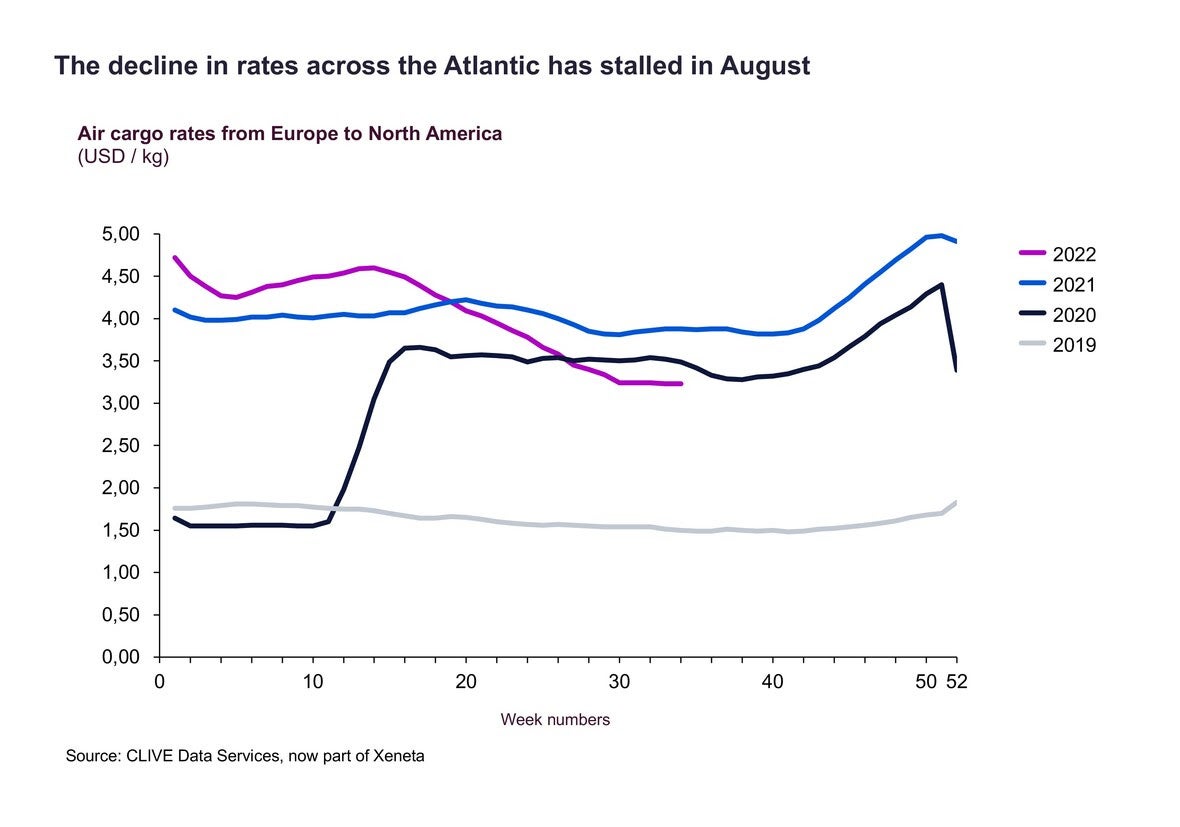

The unexpected bump in August cargo performance can partly be explained by the new parity of the strong dollar with the euro boosting demand from Europe to North America, said Niall van de Wouw, Xeneta’s chief airfreight officer, in his monthly update.

WorldACD, another provider of airfreight data, reported that worldwide tonnage during the past two weeks is slightly above their levels in mid-August, suggesting a possible stabilization of demand – below last year’s elevated levels. Year over year, the market is 9% smaller, it said.

Lagging data on Wednesday from the International Air Transport Association (IATA), which waits for member airlines to report monthly traffic figures and uses a different methodology, confirmed July’s pullback. The trade association said demand fell 9.7% — more than the 6.7% negative growth in June — and that international volume was down 10.2% versus 2021. Compared to pre-pandemic 2019, cargo throughput shrank 3.5%.

On a seasonally adjusted basis, volume measured in cargo ton-kilometers slipped 2.3% in July compared to June, which was flat from May.

Latin America was the lone bright spot for air cargo, continuing a positive trend this year after missing out on the broader market recovery in 2021 because of lower capacity. Latin American carriers reported a 9.2% increase in year-over-year cargo volumes in July. Airlines in the region have responded to the wave of business with new services and equipment, with capacity up 21.4%.

Latam Cargo, for example, recently added its sixteenth 767-300 freighter, a factory-built edition from Boeing, and this summer began flying three new freighter services between Latin America and Europe via the United States.

European carriers, coping with the additional burden of the war in Ukraine and closed airspace in Russia, saw a decrease of 17% in cargo volumes. Cargo demand in North America was 5.7% less versus 2021, but that was an improvement from the 13.5% decline in June, according to IATA.

Middle Eastern carriers have not experienced an expected bump in business following Russia’s closure of its airspace to Western airlines, forcing carriers to take longer detours and light load aircraft to carry more fuel. Air cargo volumes in the region decreased 10.9%, while capacity increased nearly 5%.

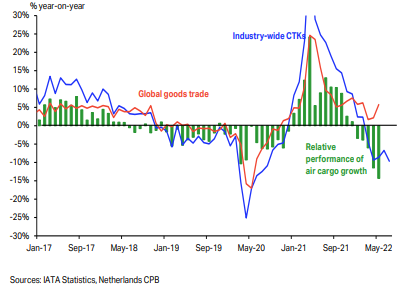

International merchandise trade has increased a few points in recent months to 5% over 2021 levels, but ocean shipping has been the primary beneficiary, IATA said.

The Purchasing Managers Index, a measure of the prevailing economic direction for manufacturing, has shown softening in new export orders — historically a leading indicator for air cargo shipments — for the first half of the year. Export manufacturing is decreasing. Chinese factory production in August shrank for the second consecutive month, partially due to power shortages that forced factories to shut down or cut back production.

Meanwhile, renewed COVID-19 lockdowns in major Chinese cities are casting a shadow on a potential manufacturing and air cargo upturn during the normally busy pre-holiday rush. Hong Kong’s Cathay Pacific, a major cargo carrier, issued informal guidance last week for softer demand this year after record 2021 volumes, citing concerns about inflation and supply chain disruptions such as airport congestion and COVID lockdowns in China.

More capacity stabilizes prices

Global air cargo capacity in August recovered 7% from the same period in 2021 primarily due to the reintroduction of widebody passenger aircraft as airlines responded to a spike in travel interest between Europe and North America, Xeneta’s air cargo unit, Clive Data Services, said. According to WorldACD, year-over-year capacity in Europe is up 19%/.

IATA reported that international travel is catching up to 2019 levels as border controls for COVID are relaxed. Total global passenger traffic rose 60% in July and is now three-quarters recovered, with Asia finally beginning to reopen more. International passenger traffic in July improved to 68% of 2019 levels, and available capacity on a per-seat basis is still down 32%.

The additional aircraft in the skies narrowed the capacity deficit relative to 2019 to 9%. IATA said the shortfall in air transport supply narrowed this summer but remains at 7.8%.

And the gap could widen as soon as October if passenger airlines begin to reduce schedules in anticipation of slower demand during the winter season.

Trans-Pacific cargo could also face a dip in capacity during September because the U.S. has suspended 26 China-bound flights by Chinese carriers in retaliation for China suspending American Airlines, Delta Air Lines and United Airlines flights under newly revised COVID resrictions. The suspensions affect seven flights from New York to China and 19 China-bound flights from Los Angeles. The airlines include Xiamen, Air China, China Southern Airlines and China Eastern Airlines.

With cargo space increasing and traffic going down, planes are less full. Xeneta said load factors in August fell seven points from a year ago to 58%, similar to the fill rate for the past three months. IATA said cargo holds were only 47% full in July.

The sluggish demand and less severe fuel prices are gradually pushing down shipping prices, although various indices show they have stayed quite stable since mid-July. Average global rates for immediate bookings were $3.61 per kilogram in August, the lowest since September last year, according to Xeneta. Still, rates are 4% higher than a year ago and 113% above the 2019 level, although that is 43 points lower than in January.

“If the fall in demand is easing, as August indicates, that capacity shift could see a return to a seller’s market again and load factors return to the mid-70%-80% range. It is fair to assume volumes will be higher in November than in August,” van de Wuow said.

Other wild cards that could drive more air cargo traffic in the coming months include a looming dockworker strike at the Port of Felixstowe in the U.K., a rupture in unresolved labor negotiations for U.S. West Coast dockworkers, and rail and trucking supply challenges in the U.S. and Europe.

But Peter Stallion, who heads the air and container freight desk at London-based Freight Investor Services, said in his latest monthly commentary that inflation, the threat of recession and households in Europe paying significantly more to cover utility costs will severely dampen demand.

“As a predicator for Q4, air freight needs to take a look at the collapse of spot rates on the container freight markets. The seasonal demand peak for ocean freight is typically in Q3, but this seasonal peak has all but evaporated,” he wrote.

Click here for more FreightWaves/American Shipper stories by Eric Kulisch.

RECOMMENDED READING:

Cathay Pacific predicts weak peak for cargo as China output slumps

DB Schenker taps Latam Cargo for dedicated S. America air service

Lufthansa cargo shipments slowed by ground staff strike in Germany