In a Monday note to clients, which described current truckload fundamentals as very difficult, Deutsche Bank analyst Amit Mehrotra said he doesn’t expect any “big negative surprises” when transportation companies report earnings next month.

However, he acknowledged the industry consensus formed in recent months that trucking companies would see a positive demand inflection in the back half of 2023 is becoming less certain.

“We view the upcoming earnings season as one of the most consequential in recent memory, as it will likely reflect trough or near-trough results,” Mehrotra said. “But it’s also clear that macroeconomic risks are increasing by the day, which may make outlooks more cloudy.”

He expects earnings for this cycle to trough in the first quarter with year-over-year (y/y) growth comps bottoming during the second quarter. Overall, Mehrotra’s call is for in-line reports from the companies he follows. His estimates sit 1% below consensus on average.

“We think this is a positive outcome for the group in the seasonally weakest quarter and in the context of broader volume and pricing concerns,” Mehrotra said. “Said another way, we think transportation companies are navigating the current environment remarkably well on average.”

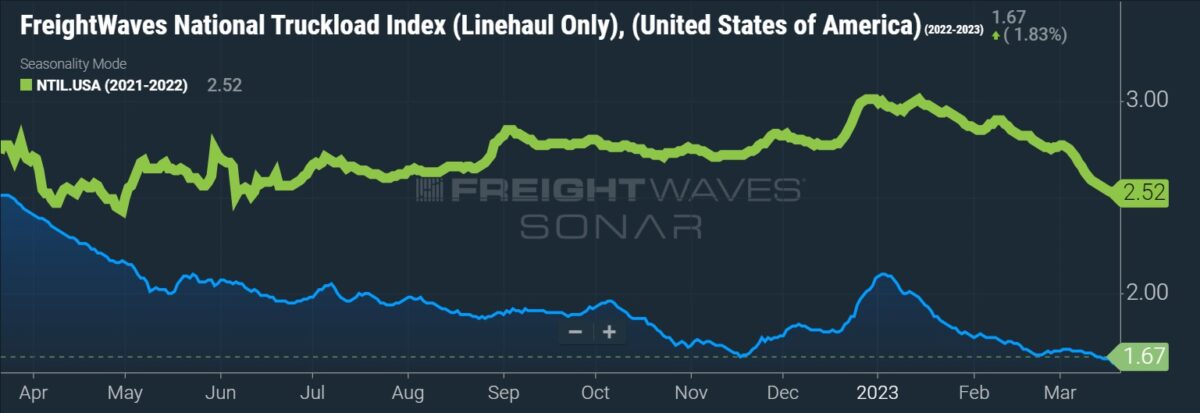

There has been a cooling in the “back half will be stronger” narrative in recent weeks as volumes have yet to step higher.

A prolonged period of retailers destocking inventories and weakness in imports showed in recent data from payment services provider Cass Information Systems. February was the first time in five months that volumes were higher than the prior month. Shipments were off only slightly y/y during the month, but total freight costs fell by 10%.

The Cass report did note a mix shift in modes from less-than-truckload and intermodal to truckload but concluded the softer freight environment will likely last several more months.

A February survey of supply chain executives also showed transportation rates fell at the fastest pace recorded by the 6.5-year-old query. The Logistics Managers’ Index showed capacity continued to expand at a near-record pace, which when combined with demand weakness, weighed on pricing.

Mehrotra previously cut his first-quarter earnings-per-share estimate for Knight-Swift (NYSE: KNX) by 9% and the full-year number by 14%. His 2023 estimate of $3.52 sits well below the company’s guidance of $4.05 to $4.25 per share.

He said Knight-Swift is seeing pressure given its “higher reliance on brokerage freight and West Coast imports.” He also said many retailers have been pulling forward bid cycles to lock in lower TL rates and pointed to Swift Transportation, which has a large concentration of retail customers, as a detractor.

He did not change his 2024 EPS estimate of $4.53.

Mehrotra maintained expectations around J.B. Hunt (NASDAQ: JBHT) and Werner Enterprises (NASDAQ: WERN) where he is 1% above the consensus estimate for the first quarter.

Last week, management from J.B. Hunt indicated a less optimistic view on volumes at J.P. Morgan’s (NYSE: JPM) Industrials Conference. The comments came after three weeks of meetings with roughly 100 of its customers. Management said it was still expecting improvement in the second half but by a lesser degree than that of its clients.

Mehrotra pointed to Werner’s large dedicated fleet composition and long-term contracts in its one-way segment as making the model more resilient when compared to irregular route carriers.

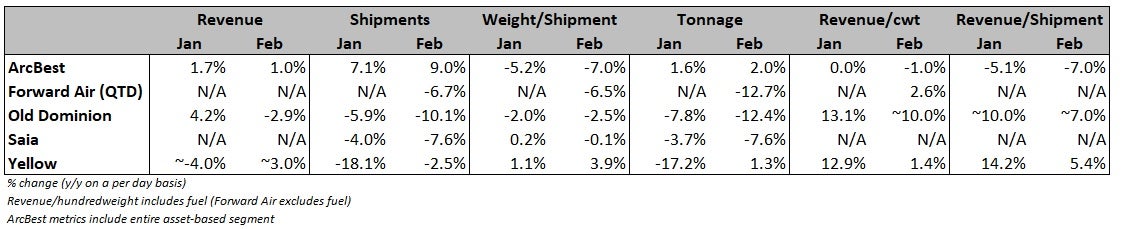

His outlook for the LTLs was basically unchanged as he believes the industry may be experiencing a seasonal uplift. He said both Old Dominion (NASDAQ: ODFL) and Saia (NASDAQ: SAIA) appear on track to hit first-quarter margin targets. Mehrotra also noted the volume comps for both get easier in the coming months, which will need “to be balanced with increasing revenue headwinds from lower fuel prices.”

The comments come after both carriers logged y/y tonnage declines in January and February.

“While 1Q results may mark the trough, there are emerging concerns on [second half] ’23 and 2024 that we need more clarity on before getting the cyclical ‘all clear,’” Mehrotra said. “In this context, real-time data in the coming weeks and months will be critical to the mid-term outlook for transportation stocks.”

More FreightWaves articles by Todd Maiden

- Weakness in freight shipments to linger, Cass says

- Yellow’s yield-at-all-cost strategy may be ending

- XPO adds former Old Dominion CFO to board