Heartland’s driver pay guarantee aids retention

At the recent UBS Global Industrial and Transportation Conference, Heartland CEO Mike Gerdin and Vice President of Finance Josh Helmich highlighted freight market weakness and outlined the retention impact of their driver minimum pay program. The executives noted that at the freight market’s peak, Heartland was rejecting 10,000 to 20,000 loads per week but as the market downturn continues, they now reject closer to 1,000 loads per week. For drivers, a lack of freight to haul typically impacts their take-home pay, as many large carriers use a pay-per-mile basis.

Freightwaves’ John Kingston writes, “Helmich said the 2-year-old program works as a ‘supplement to a minimum level on the low end.’ A driver covered by it is guaranteed pay of at least $900 and up to $1,200 per week. The level of supplement would be impacted by such things as whether a driver is normally home at night or on the road for several days.”

Another challenge for driver pay is breakdowns. If a driver’s truck is in a shop, the driver often is paid only a fraction of normal daily earnings. Helmich noted, “In the old days, they would have maybe taken home a check for $300,” Guaranteed minimum pay can be beneficial when the average cost to hire and reseat a new driver can hover around $4,500 to $5,500 once you include all the costs associated with orientation, background checks, transportation, lodging and recruiter wages. Regarding the financial impact of the driver pay structure, Heartland noted the program might result in a reduction of 1 percentage point from the company’s operating ratio.

From driver to CEO with Brittany Traylor

On Tuesday, FreightWaves spoke with Brittany Traylor, CEO and founder of TraylorTranspo LLC, about her experiences as an owner-operator-turned-asset-based freight brokerage CEO. TraylorTranspo has specialized capabilities in power-only and open-deck shipments. Before founding the company in 2020, Traylor was an owner-operator for over five years. She talks about the early days of her company and what made her decide to buy assets in addition to running her own brokerage. When building her asset-based fleet, Traylor noted leasing assets compared to buying them remained favorable due to the additional back-office assistance that large, nationwide leasing companies provide for roadside events. Typically, only large, asset-based fleets have the staff and capabilities to handle multiple roadside and maintenance events, so in spite of the higher upcharge for a lease, there was greater cost savings in time and labor due to leasing companies’ large nationwide roadside network capabilities.

An important topic Traylor highlighted was the value of specialization and the business opportunities that come with it. Many fleets typically stick to dry van freight, and a smaller segment will venture into power-only or open-deck modes of truckload transport. For those that entered the market over the past three years, this lack of specialization can put them at a severe disadvantage. Traylor noted that a key goal for her asset side was specialization to open the door for relationship-building, as the transactional nature of freight broker negotiations can become a risk when the market turns and rates fall. Traylor also says trade events and conferences are a great way to discover additional technology platforms and ways to automate time-consuming back-office tasks.

You can find the entire interview here.

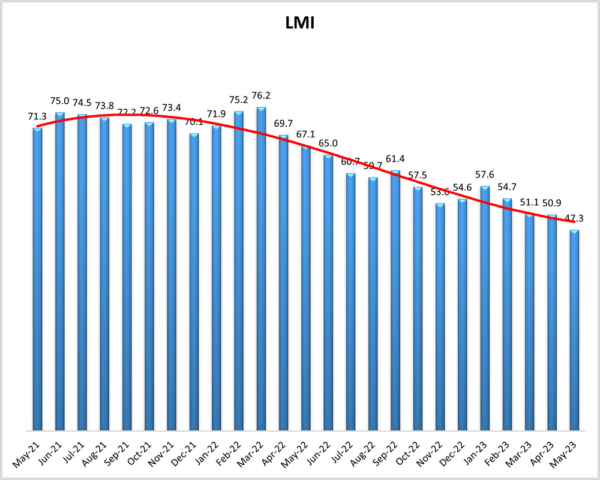

Market update: LMI May data signals logistics contraction

On Tuesday, the Logistics Managers’ Index (LMI) released May data showing supply chain activity continued to decline for the third month in a row. The May reading of 47.3 is down 3.6 points from April’s 50.9, marking the first time in the six-and-a-half-year history that the index has moved into contraction territory. A reading above 50 indicates expansion while a reading below that signals contraction. The report notes that continued softening in the freight market had a large impact on the contraction.

Regarding the truckload capacity and a reprieve from softer freight volumes, the report notes that “it would appear that the glut of available capacity has driven down utilization and prices. There is little hope of a reprieve for carriers in the form of restocking inventories. Inventory Levels dropped (-1.5) to 49.5 which is the first time inventories have been in contraction territory since February of 2020. It should be noted however that downstream retail inventories do continue to grow at a rate of 54.4, it is the upstream manufacturer and wholesaler inventories that are contracting (46.7) and bringing the overall number down.”

One concern the report noted is whether there will be a large influx of inventory during the fourth quarter. The report adds, “Without an influx of inventory for the holiday season, the freight market will continue to struggle. Whether or not a new wave of inventory is coming is unclear, with different groups holding different opinions.”

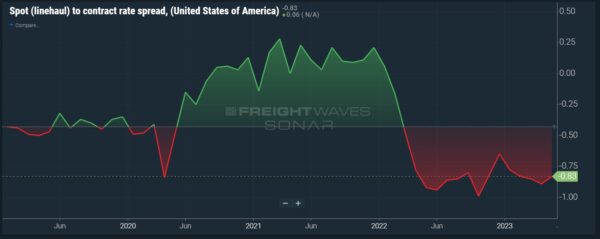

FreightWaves SONAR spotlight: Spot to contract rate spread narrows slightly

Summary: The spot (linehaul) to contract rate spread (RATES.USA) showed signs of narrowing as falling contract rates moved toward spot market linehaul rates that have rebounded since bottoming out around May 12. The current spread between contract and spot market linehaul rates hovers around 83 cents per mile with expectations for further narrowing due to the 14-day delay from the initial van contracted reported rates data (VCRPM1.USA). Spot market linehaul rates excluding fuel rose 6 cents per mile, or 3.8%, in the past 14 days from $1.58 on May 22 to $1.64.

Challenging consumer demand predictions coupled with continued excess truckload capacity continue to create a difficult freight environment for carriers heavily exposed to spot market transactions. A lingering gulf between contract and spot rates continues to incentivize shippers to strategically push down rates on high-volume lanes for transportation cost savings. The next macro freight event potentially impacting truckload capacity will be the July Fourth holiday weekend, when drivers may take extended time off and fleet availability degrades.

The Routing Guide: Links from around the web

Truckload market shrugs off Roadcheck and Memorial Day (FreightWaves)

Renewable diesel future mixed over subsidy challenges (Commercial Carrier Journal)

Study unable to firmly connect legal pot and truck safety (FreightWaves)

Next Trucking eyes possible sale; FreightTech experts weigh in (FreightWaves)

Rising May Class 8 truck orders less telling than backlog burn (FreightWaves)

19 states target EPA waiver for California’s Advanced Clean Trucks rule (FreightWaves)