Once again, the dichotomy between retail diesel direction and that of the futures and wholesale markets is kicking off another week.

The Department of Energy/Energy Information Administration retail diesel price fell 9.5 cents a gallon Tuesday to $4.498. The release of the price, the basis for most fuel surcharges, was delayed one day because of the Columbus Day holiday.

A year ago, the DOE/EIA price was $5.224 a gallon.

The decline in the DOE/EIA price comes after two days in which the price of ultra low sulfur diesel on the CME commodity exchange rose a combined 11.93 cents a gallon: 6.58 cents on Monday and 5.35 cents on Tuesday. Those upward moves were seen as a reaction to the Hamas attack in Israel and the fierce Israeli retaliation that has begun but is expected to last for weeks or months.

However, the movement in diesel did not follow those in crude markets step for step. When oil markets react quickly to international incidents that might not necessarily have a direct, clear impact on oil supplies but nonetheless create a nervous reaction, trading activity as a result tends to be seen quickly in crude markets and less in product markets.

That was visible Monday when West Texas Intermediate and Brent crude both rose either side of 4.3% while ULSD climbed 2.27% and RBOB gasoline, an unfinished product that is the trading vehicle for gasoline, climbed just over 2%.

But on Tuesday, that trend reversed itself. A late sell-off ended up taking crude down for the day, with WTI dropping 0.47% to $85.97 a barrel and Brent falling 0.57% to $87.65 a barrel. ULSD rose 5.35 cents a gallon to $3.0201, up 1.8%.

The more than 9-cent decline in retail prices reported by the DOE/EIA follows a week in which ULSD declined to a Friday settlement of $2.9008 a gallon from $3.2225 on Monday, Oct. 2.

There is no immediate impact on oil supply from the conflict in Israel. The scenarios that have been discussed as potential market disruptions generally involve some kind of Israeli attack on Iran or military action that escalates to the point of a shutdown of the Strait of Hormuz, the passage for oil into the market from several Middle Eastern countries. It is a doomsday scenario that has been feared for more than 50 years and has never occurred.

That scenario, if it played out, would be coming at a time when rising Iranian production is viewed as undermining the recent run-up in oil prices. That surge took Brent as high as $96.55 a barrel on Sept. 27, less than two weeks ago, before it plummeted to $84.07 last Thursday.

The monthly survey of production from OPEC and OPEC+ members published Tuesday by S&P Global Commodities Insights said output from the members of the group had climbed 330,000 barrels a day in September compared to August. And one of the reasons for that was that Iran production rose to 3.01 million barrels a day, the highest level since 2018 and a gain of 60,000 barrels a day from August.

Led by bearish forecasts from the commodities research unit of Citi, the recent decline in price has been fueled in part by the market’s view that while Saudi Arabia and Russia were holding the line on increases in output and were mostly sticking to their promised cuts, increases from other countries — like Iran and Nigeria, where SPGCI said production rose 100,000 barrels a day — was making the road to $100 Brent increasingly difficult to navigate. That century mark for Brent seemed inevitable as recently as two weeks ago. But the market is now more than $12 a barrel away from it.

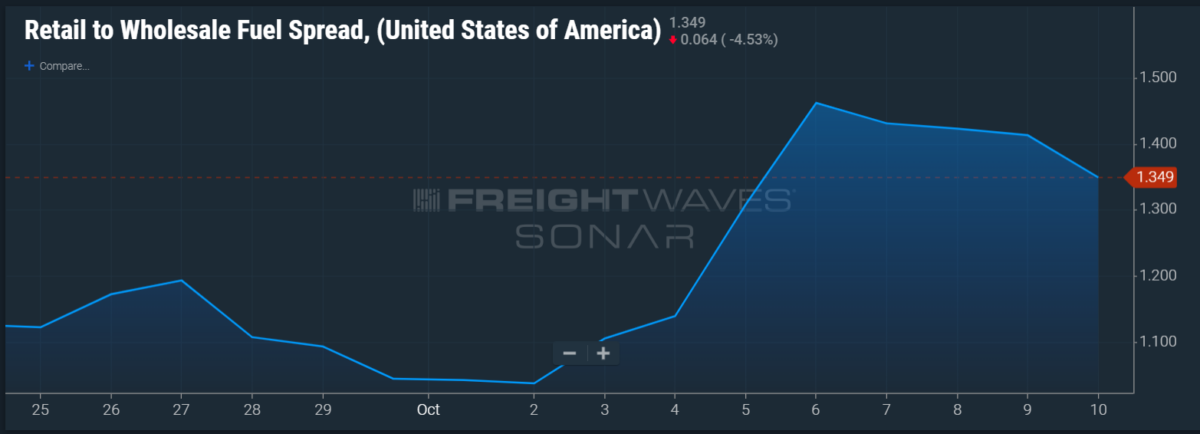

The wild swings in the market are, as expected, creating enormous volatility in the spread between wholesale and retail diesel prices, as evidenced by the numbers in the FUELS.USA data series in FreightWaves’ SONAR.

FUELS.USA measures the spread between the national average retail price and the national average wholesale diesel price. That spread on Oct. 2 was $1.037 a gallon. But as diesel markets fell hard last week and retail was slower to react, the spread had risen to $1.462 a gallon by Friday.

It has since fallen back to $1.349 a gallon Tuesday, as retail continues to fall even as futures and wholesale diesel prices have risen as a result of the conflict in Israel.

More articles by John Kingston

Truck transportation employment ranks rebound

XPO’s Jacobs on his next venture: Wait and see

Broker dodges liability in $18 million verdict, had no ‘control’ over carrier