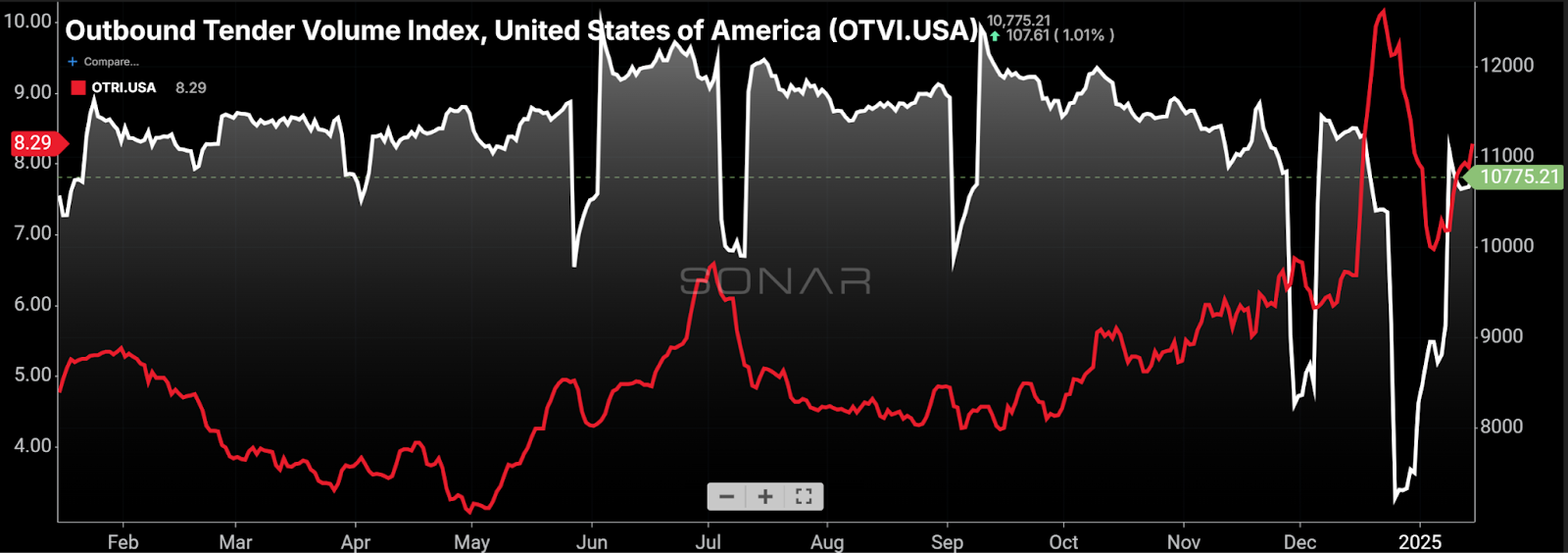

Slipping truckload demand obfuscates capacity exits

Carriers have been rejecting more tenders the past few months, but the change would have been much greater if not for lackluster volume. (Chart: SONAR)

SONAR’s primary measure of volume, the national Outbound Tender Volume Index (OTVI), which measures total shipper requests to carriers, is down 2%, year over year. Weather and the timing of holidays make clean comparisons difficult this early in the year, but volume softness appears to be preventing tender rejection rates and spot rates from rising further. Yet, both of those metrics are higher year over year, suggesting the recent trend in the direction of tightening is primarily, if not entirely, capacity-driven. With those data points in mind, we could see a much greater increase in tender rejection rates and spot rates when we get into a seasonally stronger period of the year, which normally begins in March.

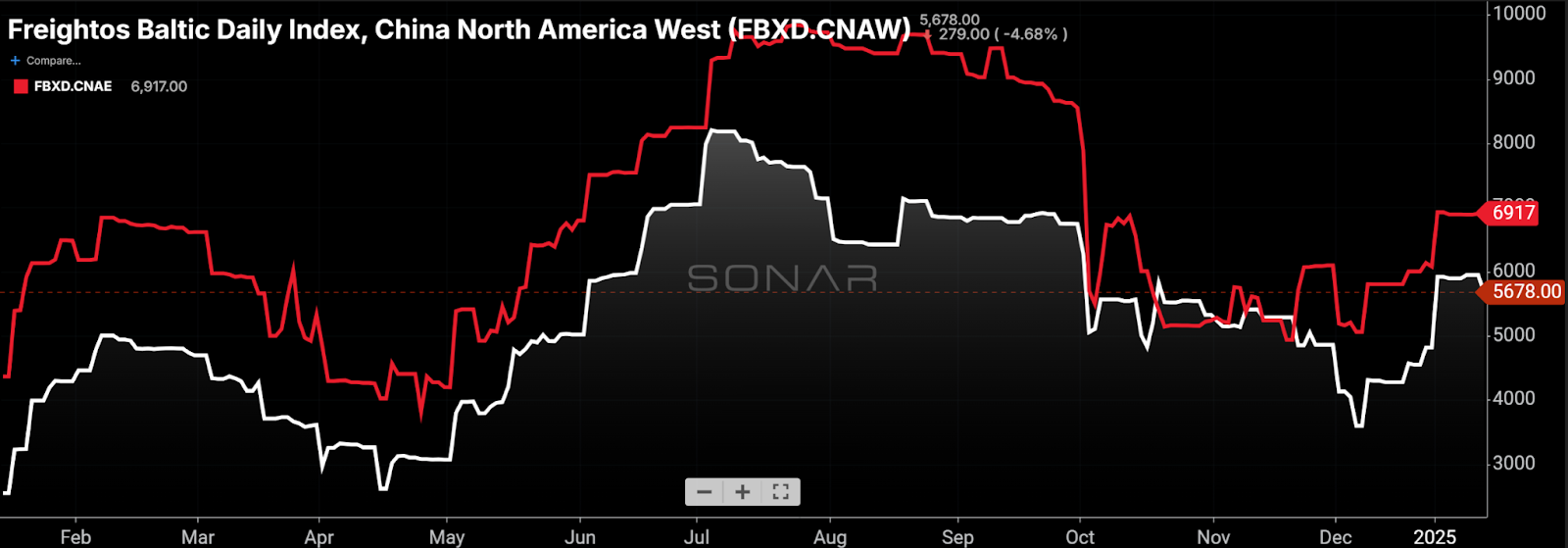

Container ship lines in no hurry to return to Red Sea

A recent FreightWaves article explains why ocean carriers are still avoiding the Red Sea: The effective capacity that has been removed as a result of longer routings greatly boosted carriers’ profits. In fact, China-owned Cosco reported that its earnings before interest and taxes increased 91% year over year in 2024 on only moderate growth in cargo volume. Avoiding the Red Sea was far from the only source of operational disruption in the maritime industry last year – throughput was also impaired by port congestion (notably at the Port of Singapore) and scarcity of oceangoing containers that arose midyear.

Trans-Pacific eastbound spot rates from China to the U.S. West Coast (red) and U.S. East Coast (white) have risen since the start of the year but have since leveled out. Freightos expects rates to decline in late February following the pre-Chinese New Year surge. (Chart: SONAR)

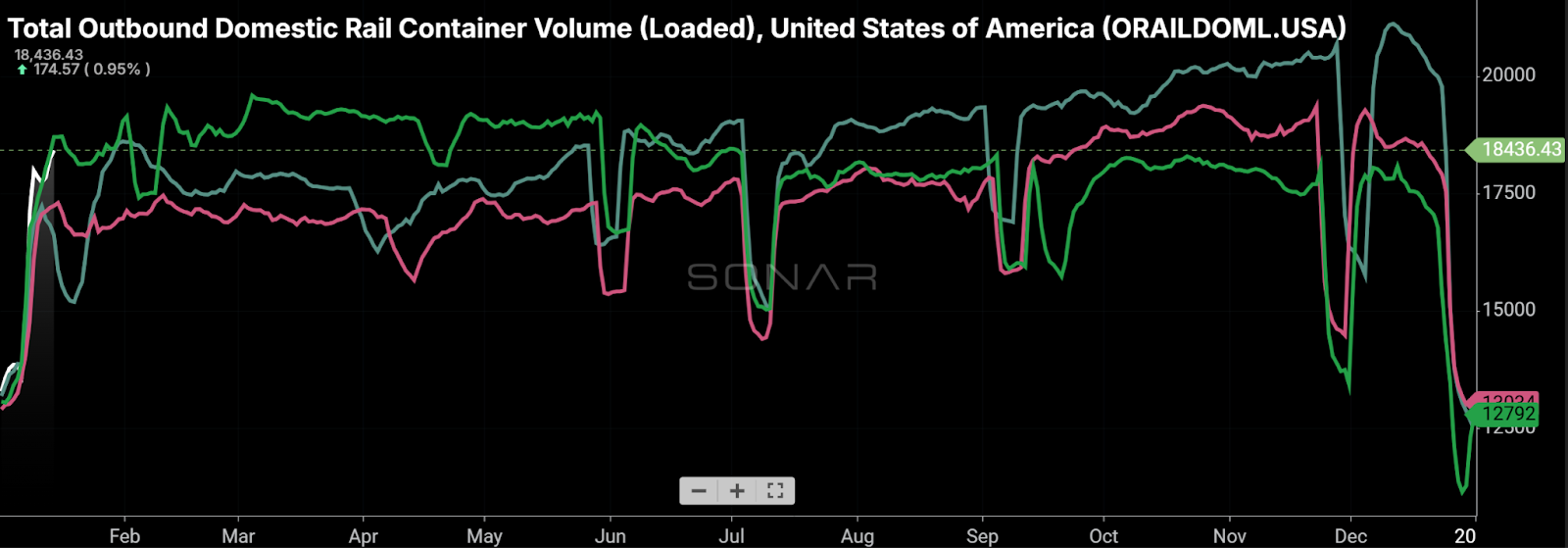

Consumer spending and robust imports drive intermodal volume

The international segment drove most of the growth in intermodal early last year. However, in the second half, domestic intermodal volume growth was stronger as oceangoing container scarcity gave rise to greater transloading volumes. (Chart: SONAR)

2024 was the third-strongest intermodal volume year in history, and December 2024 was the strongest December for intermodal volume ever, according to the Association of American Railroads. The trade group expects that impact to continue since it considers consumer spending “robustly strong” amid continued strength in the labor market. Strong intermodal volume also suggests that shippers are finding intermodal service levels to be at least acceptable. However, last week a SONAR client at a major 3PL relayed negative comments he heard from shippers regarding rail service. His theory is that shippers are using intermodal despite poor rail service because many goods are currently not time-sensitive.

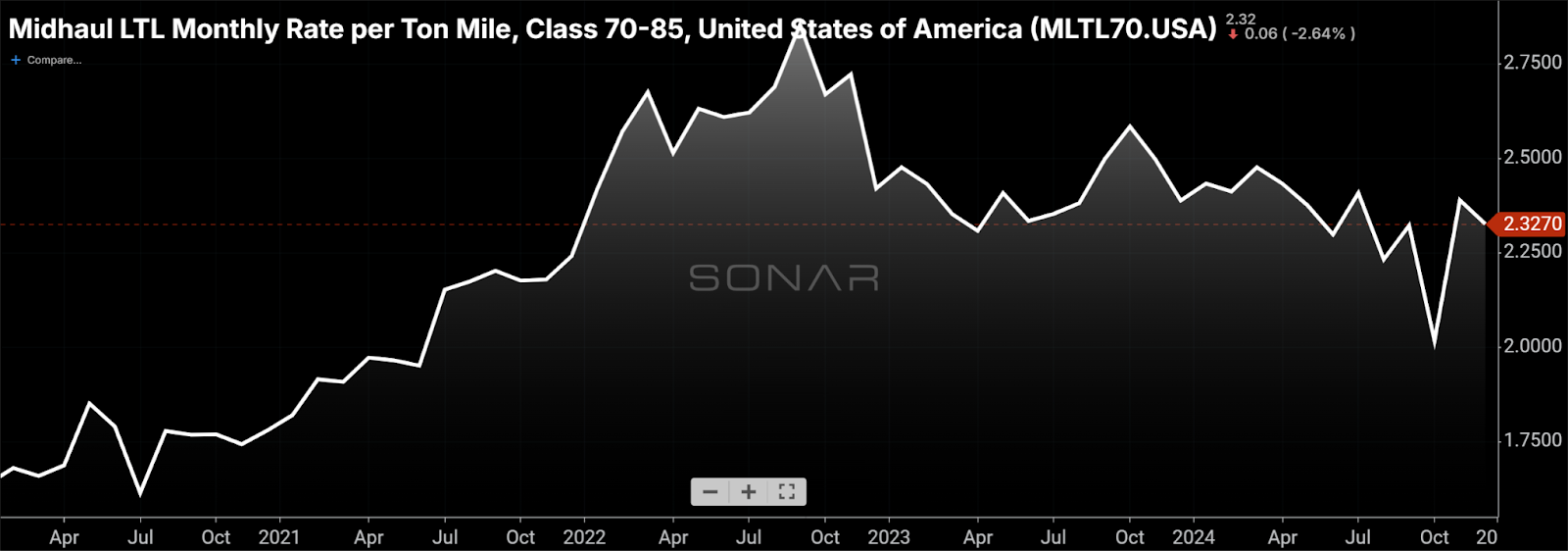

Roadrunner follows other LTL carriers, announces general rate increase

SONAR publishes LTL rates by freight class and length of haul. LTL data most relevant for CPG shippers is Class 70 freight with short-to-medium lengths of haul. (Chart: SONAR)

LTL carrier Roadrunner announced a 6.9% GRI, its first since 2021, which is roughly in accordance with rate increases announced by its peers. Per Todd Maiden’s article, “ABF Freight, a subsidiary of ArcBest (NASDAQ: ARCB), implemented a 5.9% GRI on Sept. 9 as did FedEx Freight (NYSE: FDX) on Jan. 6. Saia’s (NASDAQ: SAIA) 7.9% GRI went into effect on Oct. 21, and Old Dominion Freight Line’s (NASDAQ: ODFL) 4.9% increase took hold Dec. 2.

The Stockout: GLP-1 drugs hit grocery sales

(Image: FWTV)

On Monday’s The Stockout show, Grace Sharkey and I discussed numerous trends set to influence shippers in the retail and CPG industries this year. In addition to tariffs, many of the retail trends this year center around potential changes to industry composition, including potential consolidation, loss of relevance among direct-to-consumer brands, and an uncertain outlook for department stores and retailers under financial stress. Meanwhile, the CPG industry has shifted its focus in the direction of finding new ways to grow volume after the past few years, when sales growth was driven almost entirely by higher prices.

Volume growth will not come easily for manufacturers of packaged goods considered indulgences – that appears to be the category most impacted by GLP-1 users’ changes to buying behavior. A study by Cornell and Numerator found that a household with at least one GLP-1 user reduced its total grocery spending by 5.5% in the six months following the start of treatment. The use of those drugs is set to become more widespread – Goldman Sachs estimates that 13% of the U.S. population could be on the drugs in the next five years.

Watch the full show here and check out The Stockout playlist here.