A disconnect is arising between actual demand for cross-border air cargo service through the first half of 2024 and forecasts for the full year, raising questions about whether the current surge will strengthen during the traditional busy season starting in mid-September or lose energy.

Although the e-commerce fervor powering the air cargo market shows no signs of cooling down, that doesn’t mean other market drivers won’t. Many shippers are pulling forward fall orders to minimize the chance of late-arriving inventory associated with longer ocean transit times and port congestion due to detours around the dangerous Red Sea, and the threat of a dockworker strike at U.S. East Coast ports this fall. Global consumer demand is relatively lukewarm, so it’s possible that pre-buying is cannibalizing future growth rather than a sign of elevated trade activity.

Also, absolute demand is not as strong as the numbers suggest. Growth this year is off a low base in the first half of 2023, when cargo volumes were down 10% from the same 2022 period because wholesalers and retailers were cautious about ordering as they drew down inventory. The market’s recovery in last year’s fourth quarter means growth gains will be harder to achieve in the final quarter, potentially resulting in slower year-over-year growth rates from today’s elevated levels.

Nonetheless, tight capacity and steady price increases on main trade corridors are pressuring businesses to lock in transport deals for the upcoming peak shipping season.

Airfreight volumes in June increased 13% year over year while shipping supply only increased 3%, according to freight market tracker Xeneta. It was the seventh consecutive month of double-digit growth in the chargeable weight carried by airlines, underscoring the pronounced recovery from an 18-month downturn. Capacity utilization increased 4 points to 59%. Cargo volumes are continuing to hold up so far this month, up 12% year over year.

The International Air Transport Association underscored the trend with its latest report showing distance-based air cargo traffic increased 14.7% in May from a year ago against international capacity up 15.5%. WorldACD said global tonnage increased 12% in the first half of 2024, with second-quarter cargo out of Asia up 18%.

Delta Air Lines on Thursday reported that cargo revenue in the second quarter increased 16% year over year to $199 million, a significant improvement after six consecutive quarters of high double-digit declines. Cargo revenue in the first quarter was down 15% and fell 31% in 2023 from the prior year.

Air cargo continues to be fueled by direct-to-consumer fulfillment out of China for Chinese and U.S. retail platforms as well as ripple effects from Houthi rebel attacks on commercial shipping in the Red Sea. The attacks are causing shippers to convert some shipments to air or combine sea-air moves via hubs in Southwest Asia or the Middle East. Logistics providers report extreme weather conditions this week near the Cape of Good Hope have caused further delays for container lines as vessels change course or seek shelter from high winds and waves. Capacity could be further impacted if the situation lasts more than a few days.

A fifth of global air cargo volumes, by some estimates, are attributed to e-commerce. The e-commerce share is even higher on major export lanes from Asia to Europe and North America. Heightened scrutiny by U.S. Customs and Border Protection of e-commerce shipments from China has not resulted in diminished air cargo traffic or canceled freighter flights, contrary to some media reports. Packages may be delayed an hour or two at the most, at some inbound processing facilities, according to trade professionals.

The pressure on ocean shipping isn’t coming from the demand side – volumes are only up slightly from last year – but because the supply of vessels and containers is stretched thin. The average worldwide cost of shipping a 40-foot container reached $4,988 late last week, according to Freightos, more than five times the cost in July a year ago. Ocean rates climbed significantly since late June to $8,200 per 40-foot box out of Asia to the west coast of North America and $9,300 per unit to the east coast, harkening back to rate spikes during the COVID-19 crisis. Peak season demand coinciding with Red Sea capacity constraints have pushed Asia-North America spot rates 60% higher than their February peak, while prices to Northern Europe are 80% higher than peaks seen in January.

With ocean prices climbing much faster than airfreight, the difference in cost between the modes is narrowing and making air cargo a more attractive transportation option for businesses. Analysis by Rotate, a data-driven air cargo consultancy based in the Netherlands, shows that airfreight rates are now only six times higher than ocean – the smallest gap since the third quarter of 2022 – compared to 12 to 15 times higher under normal conditions.

Mark Webb, chief financial officer of J. Jill, said on the company’s first-quarter earnings call that the apparel retailer used airfreight to get merchandise to warehouses in time for the summer shopping season. But it doesn’t need to expedite shipments for the fall because it moved orders forward to compensate for vessel diversions around Africa, as flagged by the Wall Street Journal.

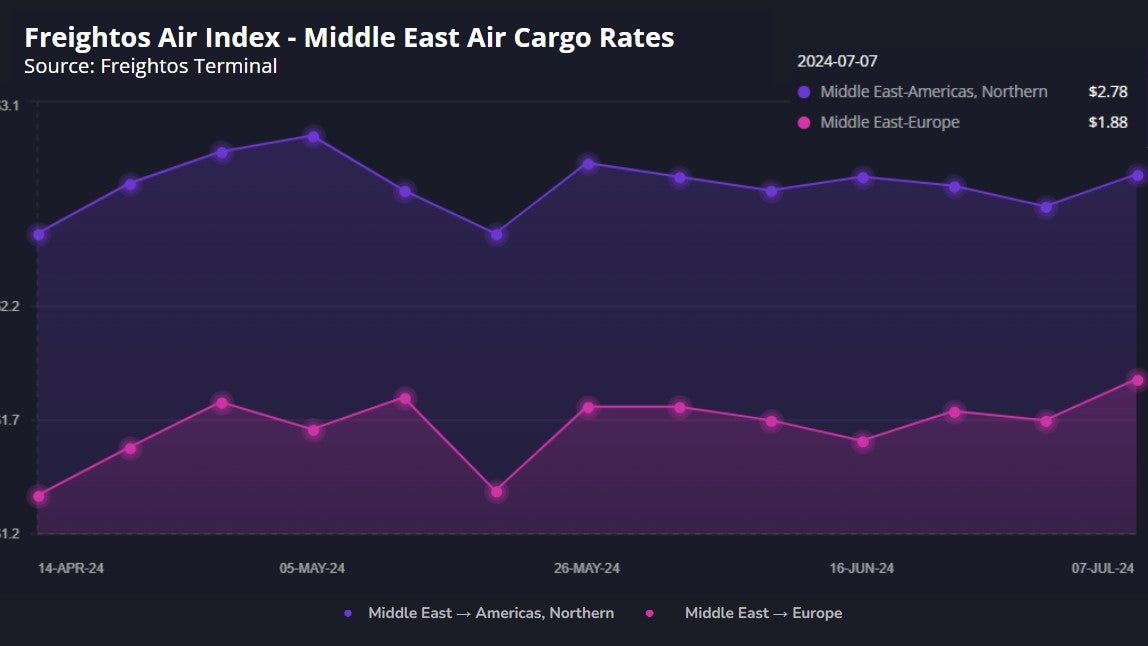

Average global airfreight rates for immediate shipping have significantly increased during the past two months. The cost of airfreight is 13% higher than it was a year ago, according to the TAC Index. Rates out of China are well above normal off-season levels at about $5.60/kilogram to North America and $3.38/kg to Europe, per Freightos. The shipping cost from Middle East airports to Europe has increased 10% in the past week, perhaps an indication that worsening ocean disruptions could be pushing additional volumes to air.

In a reversal from a year ago, WorldACD noted that growth in general cargo exceeded that of special cargo products, such as pharmaceuticals, by 3 points because of e-commerce, which falls under the umbrella of general cargo, and Red Sea disruptions. Midway through 2023, demand for specialty air cargo was growing, while the market as a whole was down 7% year over year.

Logistics providers continue to report that reserving guaranteed space allotments with airlines for the remainder of the year is extremely difficult because Chinese e-commerce platforms have pre-bought long-term capacity, with other shippers paying a premium for any remaining blocks or booking loads on the spot market. Some carriers are expected to hold back a portion of their capacity for spot-market transactions to take advantage of rising yields.

“We expect lower demand growth year-on-year in the second half of 2024 because of such a strong Q4 2023 comparison, but if you haven’t arranged your capacity by now you could be in for quite a ride. Shippers will pay more throughout Q4, the question is how much more?” said Niall van de Wouw, Xeneta’s chief airfreight officer, in the company’s latest report.

Shippers and forwarders with capacity agreements in markets that are already tight will have reduced exposure to rate hikes and peak season surcharges. Businesses that go above their allotted threshold, or don’t have a block space agreement, could face a 50% increase in rates from current levels, he noted.

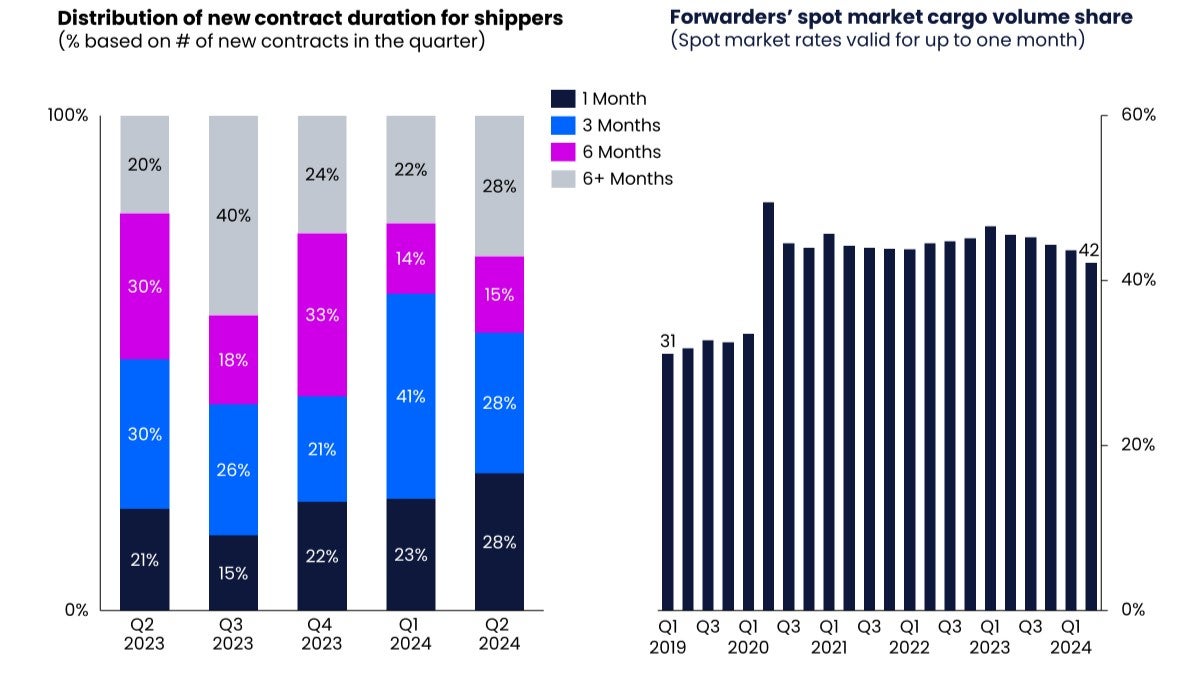

During the second quarter, shippers increasingly opted for contracts lasting more than six months over three-month contracts to avoid freight rate fluctuations during the peak season rush later this year, according to Xeneta. The data showed the proportion of cargo volumes procured in the spot market accounted for 42% of the total market, down 3 points versus a year ago.

Some carriers are still adding capacity out of China, especially to support Chinese e-commerce players. Air China Cargo, for example, recently launched service four times per week between Chengdu and Paris with its first Airbus A330 freighter, according to a monthly market update from AIT Worldwide Logistics. The cold chain logistics arm of China Eastern Airlines last month opened an Ezhou-Seoul, South Korea-Miami route operated once per week by Kalitta Air utilizing a Boeing 747 freighter. Primary commodities being shipped are e-commerce goods, flowers, electronics and perishable foods, such as lobsters, salmon and cherries.

But for the most part widebody freighter capacity is scarce on major trade routes. An indicator that rising passenger belly capacity is influencing the market comes from the Bank of America, which said in a recent report that dedicated freighter flight activity is not growing after sinking 5% in 2023. Charter aircraft will become increasingly difficult to procure when the busy peak season starts in September, logistics experts say.

Second-half deceleration?

Despite the surprising first-half resurgence of air cargo demand, IATA forecasts that full-year cargo revenues for airlines will decrease because an influx of lower-deck capacity associated with growth in passenger travel is outpacing volumes and putting downward pressure on yields.

The airline group last month predicted airfreight traffic will increase 5% in 2024 (up from its prior estimate of 4.5%) while capacity will grow 8.6%. The supply-demand imbalance, which reflects a move back to pre-pandemic patterns, is expected to reduce average shipping prices by 17.5% from the prior year. The outlook essentially assumes there will be little, if any, growth in the second half of the year – a scenario that is difficult for some to envision under the current circumstances.

Cargo revenues will decrease 13% year over year to $120 billion because of the lower yields, said IATA. High yields and revenue were enabled by severe capacity shortages and supply chain constraints during the pandemic, which reversed with the strong return of passenger belly capacity. The rate of revenue decline is better than the 33% drop experienced in 2023.

IATA’s forecasts for revenue and yield decline were revised upward from $111 billion and negative 21% in December. By comparison, industry cargo revenue was $101 billion in 2019.

Global yields year-to-date through April were still 28% above pre-pandemic levels, although IATA economists hint they are on track to approach pre-COVID-19 levels, settling slightly above the long-term average.

Whether air cargo demand will hold up remains an open question. Factors in air cargo’s favor include expansion in global manufacturing. But growth isn’t uniform around the world and actually grew at a slower pace in June, while new export orders showed their first decline in three months. Inflation is headed in a positive direction, declining in May in the European Union and Japan. The U.S. government on Thursday said the Consumer Price Index ticked down 0.1%, but price hikes are still up 3.3% over the past year. Meanwhile, U.S. retail sales barely increased in May and prior months were revised downward, suggesting great financial hardship among consumers, according to Bloomberg.

It should be noted that the U.S. government’s retail sales figures aren’t adjusted for inflation, which means changes in prices could push up totals even without an increase in volumes sold. Major retailers in recent weeks have implemented major discounting programs to help bring back shoppers that have tightened their pursestrings.

RECOMMENDED READING:

What does air cargo’s early peak season mean for peak season?