Chart of the Week: Outbound Tender Volume Index – Los Angeles and Ontario, Outbound Tender Reject Index – Los Angeles SONAR: OTVI.LAX, OTVI.ONT, OTRI.LAX

Truckload tender volumes have dropped about 18% out of Southern California over the past year while tender rejection rates are currently exceeding the previous year’s levels. This seemingly contradictory data shows that even in a loose aggregate environment, capacity is not just about the number of trucks in the U.S.

The recent decline in carrier acceptances is not a straight example of aggregate capacity correcting, but of carrier networks becoming unbalanced as natural freight flows shift.

After many retailers recognized their overordering methodology had filled their warehouses in early 2022, they did what anyone would do: They turned off the faucet. And over the past year, carriers have responded by positioning less equipment out West.

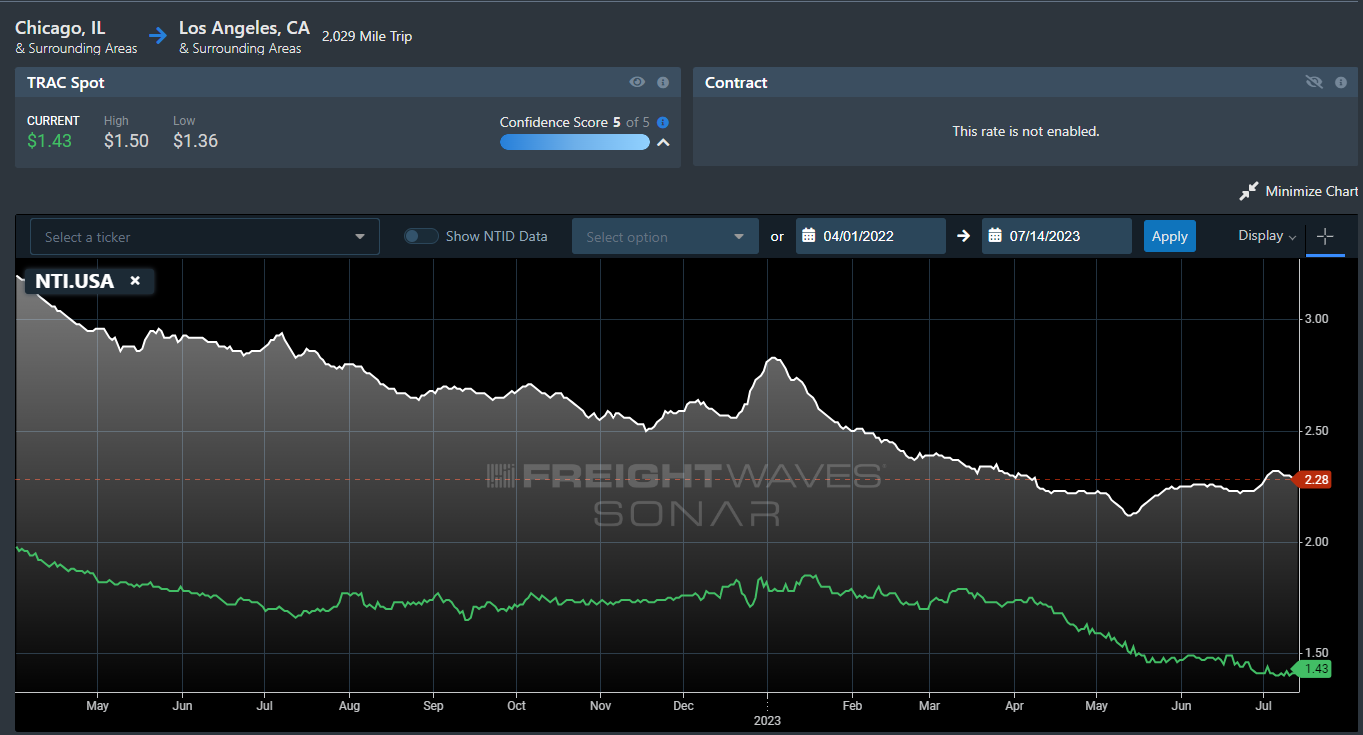

This is reflected in the spot rate from Chicago to Los Angeles. Spot rates in this lane stabilized last summer and actually increased 4% from last July to April of this year, according to FreightWaves TRAC contributors.

The National Truckload Index (NTI) — a measure of all dry van spot rates — fell 23% over that same period.

Once capacity again started to show signs of tightening out of Los Angeles — reflected in the steady rise in tender rejection rates that began in April — spot rates for loads moving into the region started to fall again as carriers attempted to position themselves where they were needed.

Overcorrection

Over a third of the containerized imports enters the country through the port complexes of Los Angeles and Long Beach. Prior to the pandemic, this activity peaked in the mid- to late third quarter as shippers pushed freight to the Eastern half of the country for the holiday season.

During the pandemic, this pattern persisted throughout the year as companies struggled to keep up with consumer demand. Not only did truckload capacity grow, but carrier networks were designed to move capacity into Southern California.

Once the import faucet turned off and Eastern warehouses were filled, capacity was stranded out West with nothing to move. Carriers were now left with underpriced lanes heading into the region due to the lack of volume enabling them to price inbound loads at a lower level. And now even though demand is lower from an annual perspective, capacity in the region has fallen at a slightly faster pace.

On the flip side, spot rates are rising out of Los Angeles, but they are not breaking any records. TRAC rates from Los Angeles to Chicago are up 17% versus early April but still below where they were to start the year.

If and when the freight market does eventually turn, these types of irregularities will become increasingly pronounced. The underlying demand pattern shifts are harder to identify in a market where capacity is in abundance.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.