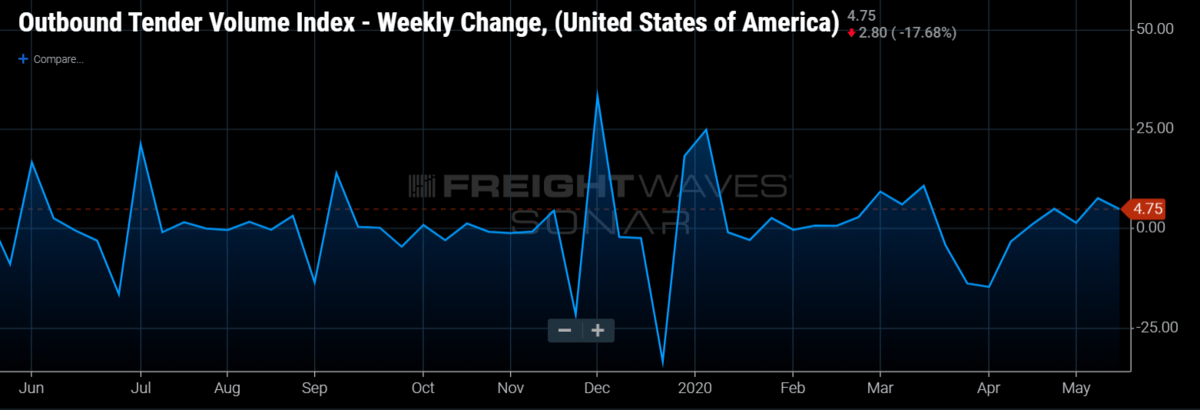

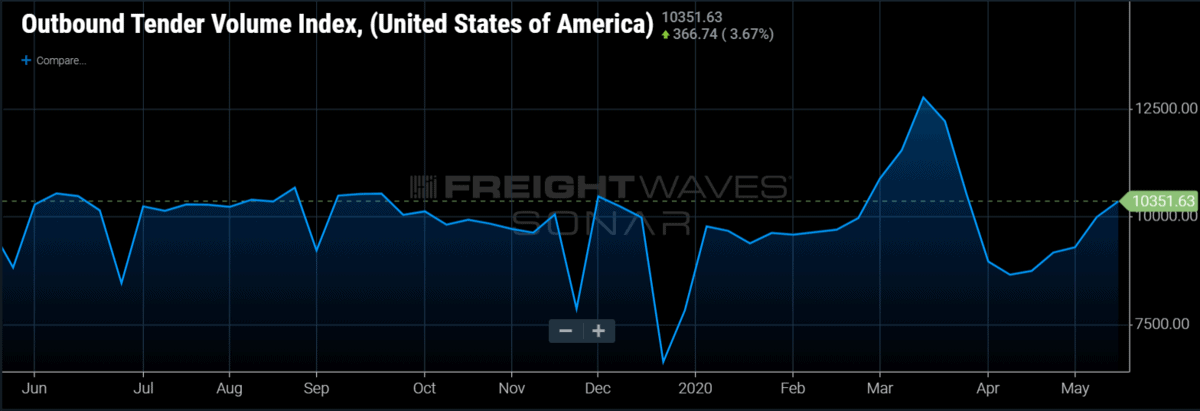

National outbound tender volumes continued to climb this week by 5% week-over-week and 7% year-over-year. Overall volumes are surging even as import volumes are plummeting. There is typically a week lag before imports get tendered and included in our OTVI. The surge in imports at the end of April is playing a part in the volume surge. California is home to two of the largest ports in the country but is also the largest agricultural-producing state.

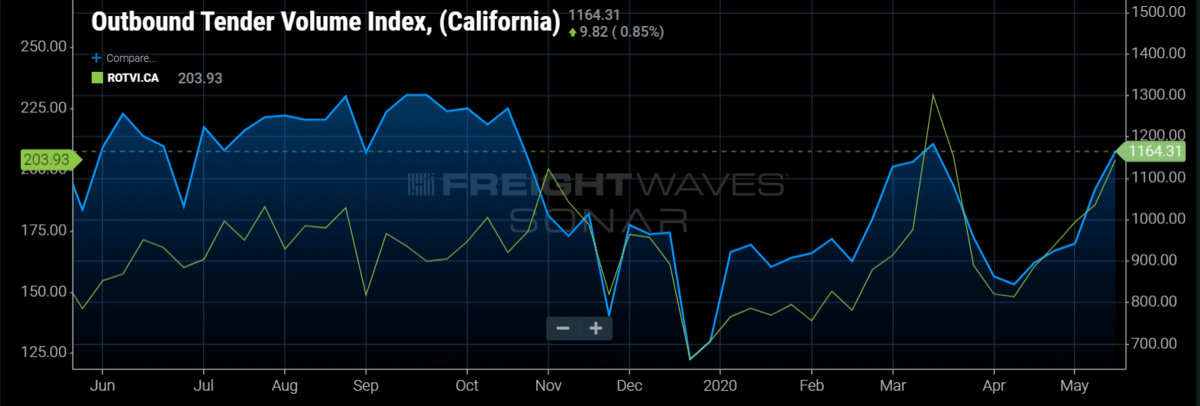

Both total volumes and reefer volumes out of California have surged over 30% in the past month. OTVI.CA is now at precrisis surge levels, which is remarkable. However, the volume surge that has occurred on a national level is too significant to have come from just one market and upward momentum is broad.

A few weeks back, the automotive industry seemed to represent a promising source of pent-up volumes once its factories came back online. The Michigan (OTVI.MI) and Ohio (OTVI.OH) outbound tender volumes have not risen as rapidly as the national average. However, inbound volumes to both Ohio and Michigan have been rising rapidly. This may translate into much-needed outbound volumes from the two states.

This time of the year, we should expect to see a produce bump, but total volumes are rising faster than reefer is currently. That said, traditional produce markets in the Southwest have exhibited the largest monthly changes in volumes (Tucson, Phoenix). The rapidly improving consumer spending data is also playing a role in this surge. The reopening of most states is unleashing the pent-up demand from Americans who have grown tired of being on house arrest. How long the surge can last remains to be seen.

On the positive side, 13 of the 15 major freight markets FreightWaves tracks were positive on a week-over-week basis. This ratio continues to be very strong in recent weeks. The markets with the largest gains in OTVI.USA were Los Angeles (17.10%), Atlanta (14.76%) and Savannah, Georgia (8.96%). The markets with declines were Seattle (-7.77%) and Laredo, Texas (-7.42%).

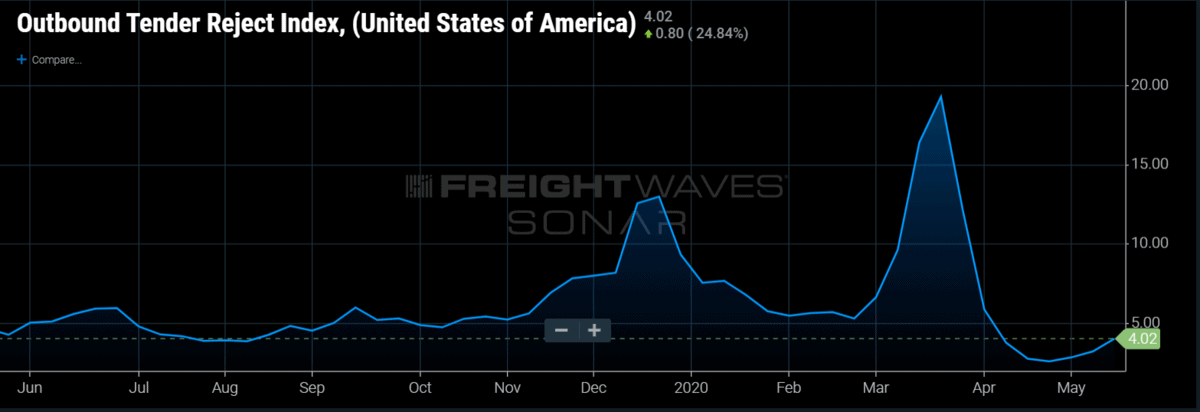

Tender rejections continue to improve with volumes

Outbound tender rejections have increased week-over-week for the third week in a row after tumbling for the six weeks since the OTRI peak of 19.25% on March 28. It seems the trough is now behind us, but at 4.02%, OTRI is still in a historically low range.

Rejection rates vary by trailer type. Currently, reefer rejections are more than double van and four times higher than flatbed. However, reefer rejections have flatlined this week. Van rejections are the primary source pushing OTRI.USA higher this week.

There are pockets of tightening capacity, mostly on the West Coast and in New England. Now that volumes have begun to return, OTRI is likely to rise modestly in the coming weeks as carriers regain confidence that they may have options besides their contracted freight. However, as of now, carriers are still accepting nearly every contracted load they can get their hands on to keep utilization high and keep trucks rolling. Capacity will not tighten significantly until freight volumes are restored in most markets around the country and that has not happened yet.

For more information on the FreightWaves Freight Intel Group, please contact Kevin Hill at khill@freightwaves.com, Seth Holm at sholm@freightwaves.com or Andrew Cox at acox@freightwaves.com.

Check out the newest episode of the Freight Intel Group’s podcast here.

CM Evans

Looking at those volumes on the charts I’m starting to wonder how much of the spot market is actually on contract. I’d like to see some relative charts to compare Tenders rejections and spot Market loads YOY. I’ll guarantee a good percentage of the loads the brokers are moving so cheaply lately are actually contract loads billed to the shipper at contract rates. FW trolls these comments so I expect they’ll be looking at that data if not already, unlikely they will post it to be viewed/exposed.

Those interested in how the recent rate wars are shaping up should follow the beef/pork industry. Ranchers are in a similar pricing war w/the producers and continue to press for action. Regardless your position this may offer insight into how the feds may/may not involve themselves truck pricing.

Dave

This volume headline seems completely different than what is going on out here. These numbers say we are in the best growth economy in years. Where do they come from?

Eat Shit

“being on house arrest”

I will not be reading your online posts anymore. You can’t even publish an article on freight rates without displaying a bias. Gross. Seth can’t be aware of what he is saying and how it can be interpreted? This explains how he ended up writing opinions on Freight Rates. Hell, that the commentators can’t even agree with him. Chumps.

Steve

And we still do not know how many of the automotive parts manufacturers have closed their doors permanently. The press has been silent on all of this.

Steve

Going to be two to three months before automotive freight is running in any form or shape of normal, there are no parts. Mexico is still down, many local shops cannot lure employees off their couches, where they are making more money than the job pays. Meanwhile, the temp agencies are sending in their crew, but it may take months to train that bunch according to one auto parts manufacturer. And then we have the raw materials, more than a few parts manufacturers are unable to source the materials needed to manufacturer the parts. Don’t hold your breath on this industry folks…

Elvis Durant

“Great week for load VOLUMES”???? Ha! Good one!