It’s that time of year – retail news abounds on FreightWaves and elsewhere

I thought Target’s management team put it well last week as it now describes consumers as “resourceful,” meaning they are still shopping but are looking for value and waiting for deals, rather than “resilient,” the term it used previously. Along similar lines, the National Retail Federation expects November-December holiday sales to rise moderately – it forecasts a 2.5%-3.5% year-over-year increase, suggesting it doesn’t expect it to rise any more than inflation. On Target’s earnings call, an analyst highlighted another retail trend – that consumers are concentrating their shopping with a smaller group of preferred retailers. After all, stocks are trading as if we will buy EVERYTHING from Amazon, Costco and Walmart. Here are a handful of articles that describe that environment in addition to other turmoil in the retail industry:

- Walmart driver wins defamation case against retailer for almost $35 million (FreightWaves)

- Amazon workers plan global protests on Black Friday, Cyber Monday (FreightWaves)

- Macy’s says lone worker hid up to $154M in delivery expenses since 2021 (FreightWaves)

- We Messed Up: Kohl’s CEO Gives a Mea Culpa (The Wall Street Journal)

- Target’s Slide from Cheap Chic to Dull Chore (WSJ)

- Black Friday: How Some Shoppers Plan to Score the Best Deals (WSJ)

- Nordstrom tops Wall Street’s earnings expectations, as shoppers buy more clothes and shoes (CNBC)

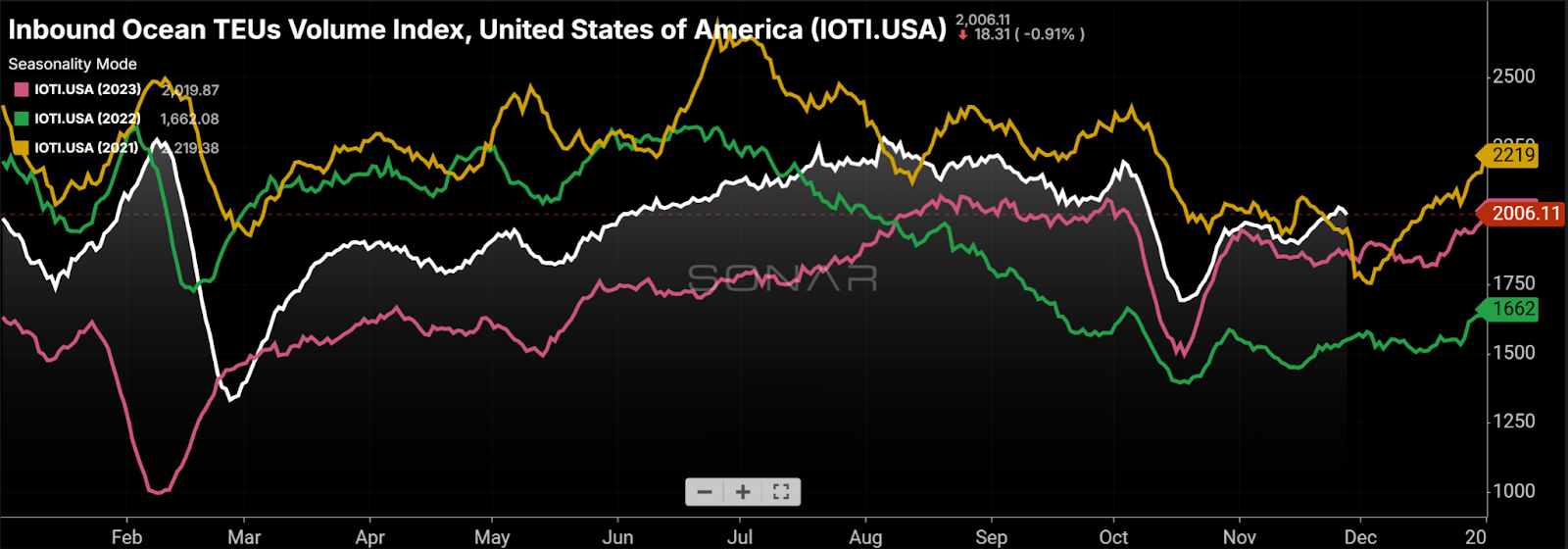

Import demand ahead of seasonal norms

(Chart: SONAR)

The impact of tariffs, and their resulting influence on the domestic freight markets, is top of mind for shippers. One SONAR dataset to watch is the Inbound Ocean TEUs Volume Index, which measures demand to move ocean containers at point of origin (most often China when considering ocean imports coming into the U.S.) The index is rising now at a time when demand is typically slowing seasonally, up 7.8% year over year currently and at levels above each of the past three years, including 2021, an unusually robust year for imports. A portion of this strength appears to represent a pull-forward ahead of tariffs. In addition, the ongoing Red Sea avoidance seems to have altered seasonal trends given the extra two-week sailing time for vessels that need to sail around the Cape of Good Hope.

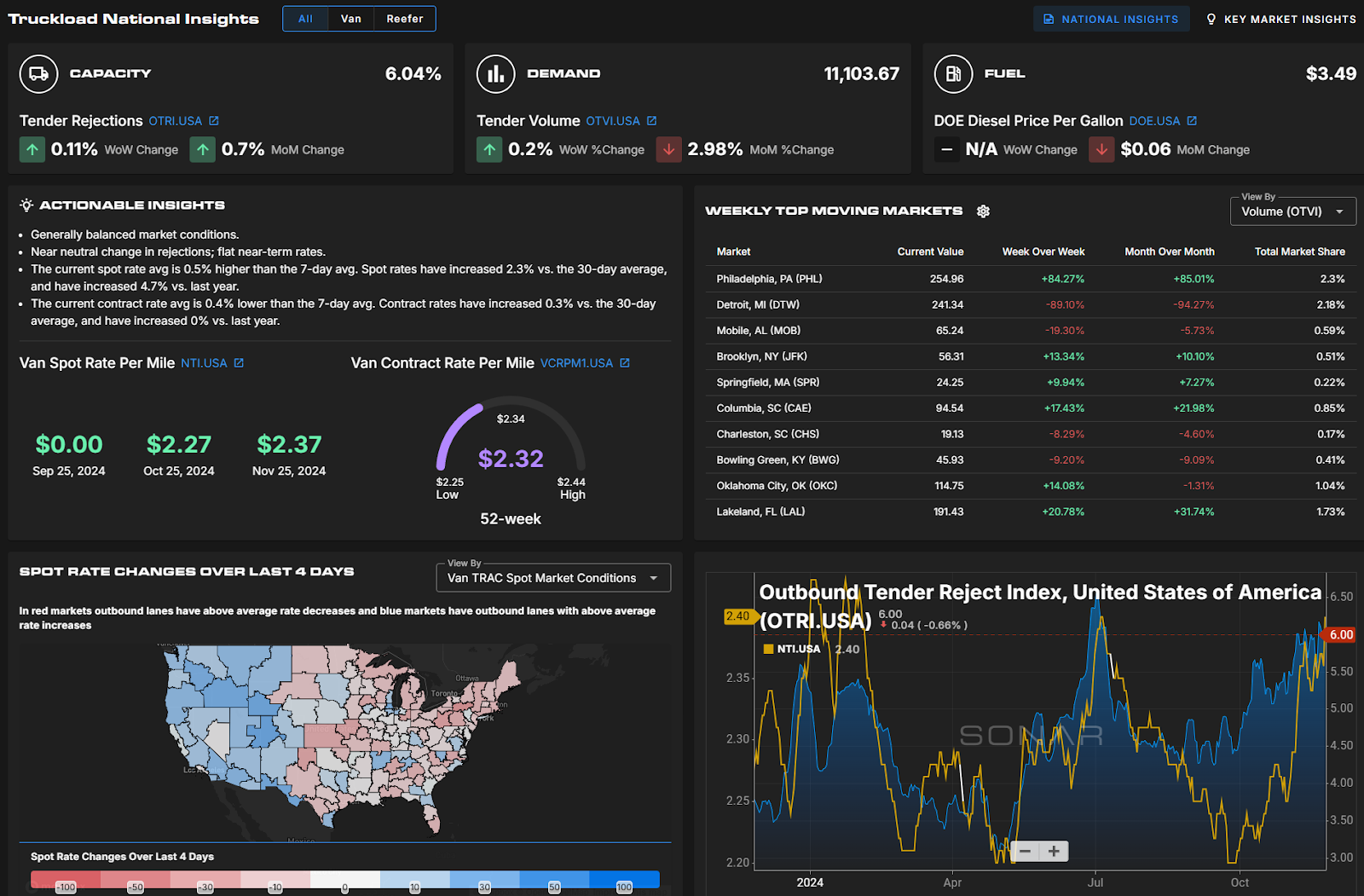

The Stockout show highlights SONAR enhancements

(Image: FWTV)

On Monday’s The Stockout show, Grace Sharkey and I discussed the SONAR enhancements unveiled at last week’s F3: Future of Freight Festival. In addition, we discussed Target’s disappointing earnings and the FreightTech Top 25 awards.

The SONAR enhancements include two sets of “insights” pages: one National Insights page that summarizes the entire truckload market and a Key Market Insights page that summarizes any local freight market the user types in. Those pages are designed to improve the SONAR user experience through greater ease of use, especially for newcomers.

The new Truckload National Insights page provides a one-page tear sheet. In short, the market is generally balanced amid a rise in spot rates and tender rejection rates the past few weeks. (Chart: SONAR)

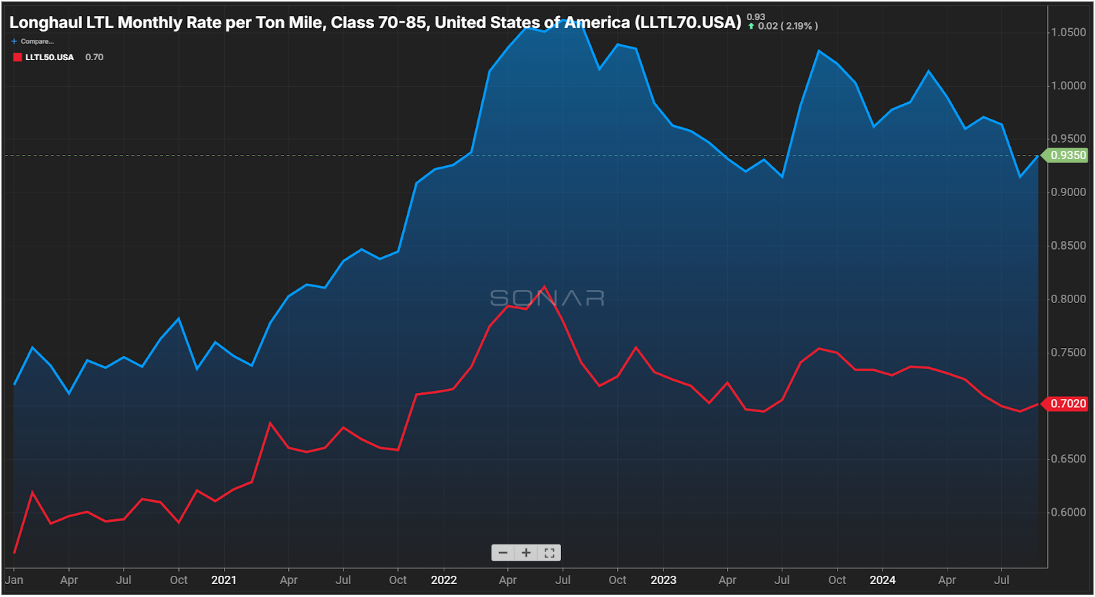

In addition, SONAR is adding 20 new less-than-truckload tickers and 69 new intermodal tickers. The LTL tickers show rates broken down by freight class and length of haul. For instance the LLTL70.USA ticker will show the monthly rate per ton-mile for long-haul LTL shipments within classes 70-85.

LTL shipments with higher classes (less dense freight) are associated with higher rates. (Chart: SONAR)

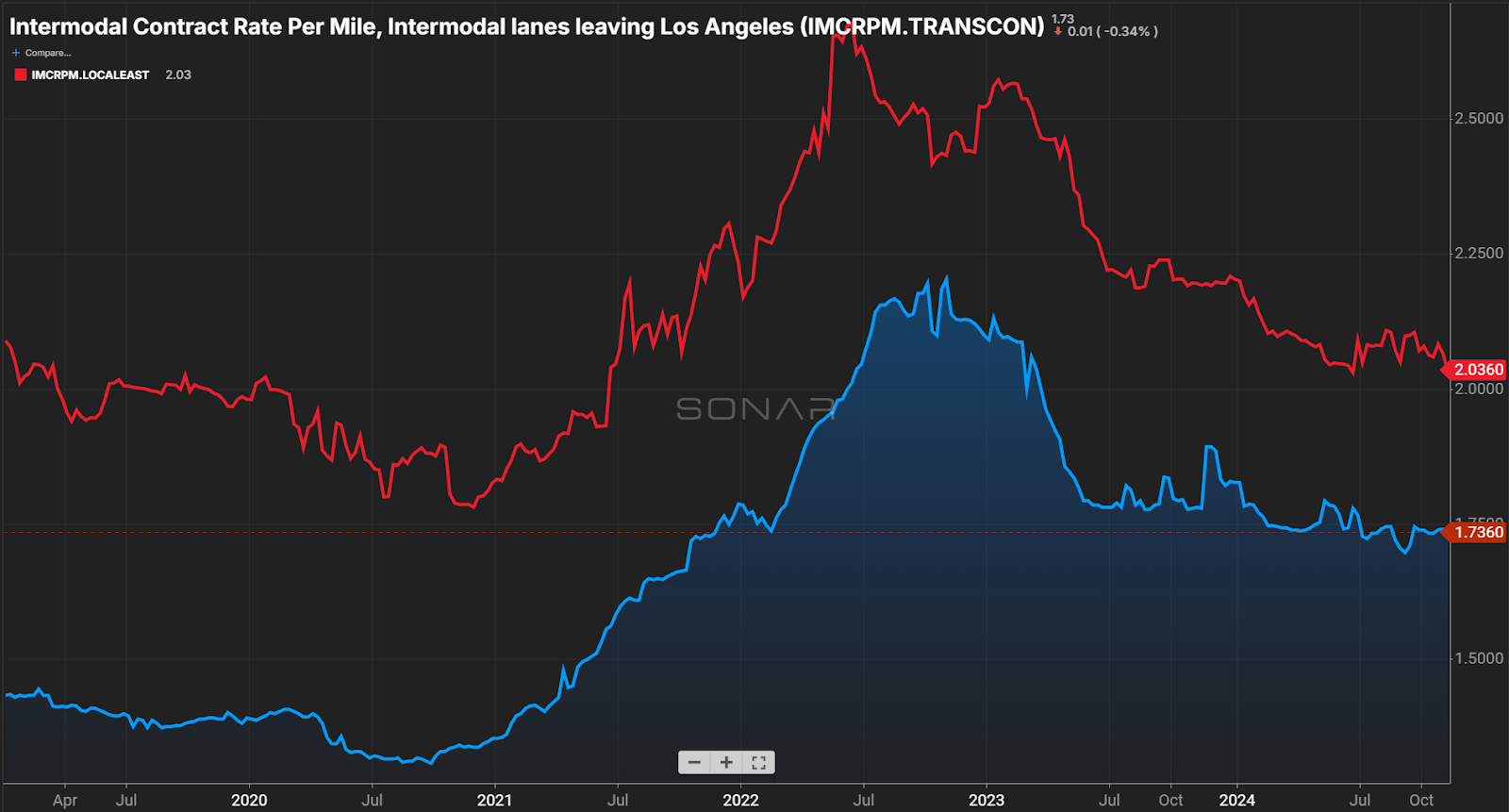

The new intermodal data shows domestic intermodal contract rates by lane for 67 lanes, including fuel surcharges. An example is IMCRPM.LAXCHI for LA to Chicago. The new intermodal data also includes two aggregates indices, a headhaul index (IMCRPM.TRANSCON), which is an average of five long-haul outbound LA lanes, and a Local East Index (IMCRPM.LOCALEAST), which is an average of nine dense lanes in the Eastern third of the U.S.

Long-haul intermodal lanes (long-haul transcontinental average is in blue; shorter-haul local east lane average is in red) generally have lower rates per mile, making it easier for shippers to realize savings versus truckload. (Chart: SONAR)

See Monday’s show here and check out the full The Stockout playlist here.