The views expressed here are solely those of the author and do not necessarily represent the views of FreightWaves or its affiliates.

It’s not a forecast. It’s a prudent warning…

The continuing coronavirus pandemic and our social reaction so far are driving our business culture towards a high-risk economic impact.

Stay-in-place warnings and increasingly mandated government requirements will drive down income and gross domestic product (GDP). Fundamentally, the American economy will likely face choosing survival spending tactics.

Cash will be preserved. A survival kit approach to managing family budgets will focus upon water, food, shelter, heat and medicines.

Budgets will be managed as if there is no discretionary income to be spent on non-essentials.

How long will the internet and individual cell phone accounts be maintained? That’s an unbelievable question to even ask. Or is it?

Experts can’t agree on the level of economic impact. Just a week ago some suggested that the chance of a U.S. recession was about 50-50%. It was less than 30% three weeks ago.

Nobody knows. There are no previous experiences like this pandemic pattern upon which to build a reliable input/output GDP change model. We are all flying blind.

With this as background, let’s briefly examine what the role of the rail freight sector is. How relevant is rail freight’s services during a stay-in place period? What are rail freight’s capabilities at serving the essential survival kit?

Let’s be simple about this. How much petrol and car flexibility do we need under such grim conditions?

Is this anything like the months after the bombing of Pearl Harbor?

When the U.S. entered World War II, there was definitely an important role for railroad companies to move the nation’s freight and people. Railroads moved more than 60% of the nation’s freight volume back then. That included express parcel movement in carload units.

This is now. In 2020 trucks are moving emergency supplies and food. Truck volume was up by more than 15% year-over-year last week.

No database reports a similar surge in rail freight to help with the critical emergency stock replenishment.

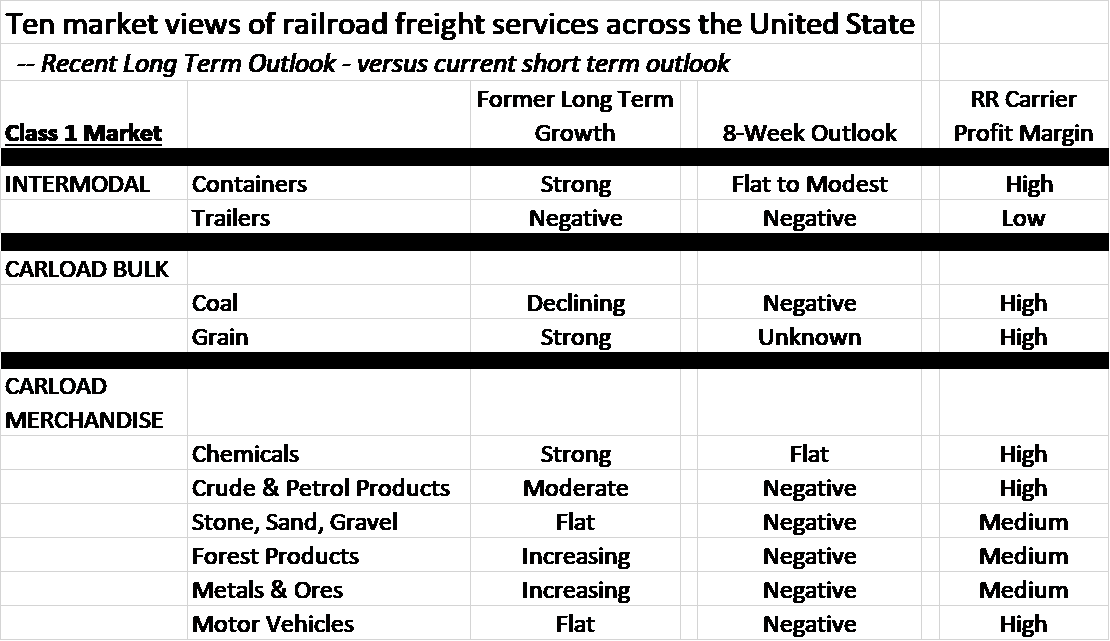

Perhaps we just don’t have the correct railway dataset to examine? For the moment, we can examine the recent American Association of Railroads (AAR) and rail industry freight market sectors.

Here in a table are a few trend points.

The 8-week outlook and the railroad carrier profit margin assessments are mine. They are based on a review of multiple sources. It is a judgment call.

The critical question is how do you or your alternative sources see the outlook – with market behavior and demand changing as we move toward the end of March.

Most of the trucking-provided services use semi-trailer units. That’s a market that railroads have been largely exiting. Thus the negative outlook.

The intermodal container market is driven more by international commerce than domestic commerce. Those supply chains must cover long distances and normally take weeks to deliver to U.S. ports. Goods now moving toward our ports by ship may now no longer be in high demand given the expected shift in 2020 discretionary income. Much of the goods still to be delivered might well end up being warehoused. Many of the landed containers might not move inland via rail intermodal – at least not immediately. That assumption is part of this “fog of war” and therefore, my negative 8-week assessment.

Coal may suffer greater than expected market share losses because natural gas prices are now even lower than previously expected. Metallurgical coal exports may have to await orders as metals manufacturing decreases globally into the summer months.

Only grain – a fundamental food stock and livestock feed – may increase via larger than expected post-trade war agreements. Yet, that purchasing signal hasn’t yet been seen.

Meanwhile, there was this headline – “Consumers could spend $20 billion less for gasoline this April as futures prices collapse?” (March 23). Less motor vehicle travel reduces the crude oil market demand as does the availability of cheaper imported fuel from overseas sources. It’s a very complex question.

Under such market demand conditions, prices at the pump could fall 20%. In a related downstream demand report, some sources believe the U.S. refining industry will shut down about 30% of its capacity.

My short-term conclusion is that even more railway tank cars will be stored. The financial outlook within railway headquarters must be gloomy. Realistically, there is no rapid turn-around expected in regard to railway traffic volume.

Here are my late March conclusions…

The seven largest Class 1 railroad carriers will likely resort to proven historical management weapons of cutting variable costs and cutting capital expenditure projects during the remaining months of 2020.

The bottom line? It’s a fluid and unknown rail freight market right now. Moreover, there is no similar downturn model with which to calibrate an upside market demand for rail freight.

Therefore, rail industry experts will hedge their bets. This economist sees a negative rail carload business cycle lasting another seven to 10 weeks based upon the current pattern of government social distancing mandates.

Housing and non-housing construction has ceased in many of the hardest hit states like Pennsylvania and New Jersey.

The current federal initiatives targeting personal aid and corporate financial aid are not by themselves generating new business growth confidence. They will be “survival” payments.

They are not creating “buyers.” Without buyers, market confidence and market demand will not translate into new orders.

The length of this market lag time is the great unknown. Freight transportation is after all a derived demand function. And railroads are limited in their ability to positively increase derived demand.

They could decrease their rates. But so far, no railroad appears to have significantly done that. At best, rail freight might be in a holding pattern.

In a search for balance, others are more optimistic. Bill Stephens in Trains offered this outlook:

“Bloomberg analyst Lee Klaskow says Class I railroad earnings growth is likely to be reduced to low-single digit percentages. Financial analysts previously expected mid- to high-single digit growth this year.”

In December 2019, before the coronavirus pandemic was declared, Richard Kloster of Integrity Rail Partners Inc. wrote in Progressive Railroading:

“Longer term, there is more to be optimistic about. Just not in 2020.” Yet, he said we can always hope for “better,” earlier.

In closing, what are your data points signaling about rail freight demand?

Which Class I railroad has an upbeat real-time story? In such tumultuous times, there is more to be optimistic about longer-term, than in the short-term (all of 2020?). So, let’s hunker down and hope for “better” – sooner.