The future of railway-hauled scrap metals is profitable but slowly declining.

FreightWaves features Market Voices – a forum for voices with unique knowledge of numerous transportation/logistics/supply chain sectors, as well as other critical expertise.

Scrap recycling is an essential logistics business. It is gradually becoming part of the reverse supply chain as more states look for manufacturers to follow their goods from birth to death.

Technically, scrap metal is the combination of waste metal or metallic material that is capable of being recycled from previous consumption or product use.

In both the transportation and the reclamation business worlds, there are two basic categories of scrap metal – ferrous metal and non-ferrous metal. Ferrous metal contains some percentage of iron. Non-ferrous metal does not contain iron as a component. Non-ferrous scrap would include aluminum, copper, lead, nickel and others. Most of this report deals with the ferrous metal scrap business.

For shippers and receivers (railroad customers), the scrap business is profitable. One source reported that during 2015, the U.S. ferrous scrap industry was worth $18.3 billion.

The business of moving scrap isn’t glamorous. It’s frankly dirty. The business objective is to recycle used goods as cheaply as possible. That’s the manufacturers’ and reclaimers’ point of view. The railroads want it to be profitable. And into 2019, it is profitable for the railroads.

To move the scrap, railroads typically use a fleet of gondola railcars. The gondola railcars have a low center of gravity and are about 52- to 65-feet long. The length of railcar used depends upon the track and loading conditions of the customer facilities.

Scrap geography

In the U.S. market, scrap is concentrated in locations that will both produce it and process it – which are mostly east of the Mississippi River. Scrap that is collected in the West is usually exported to Asia (mainly China).

In the eastern U.S. both CSX (Nasdaq: CSX) and Norfolk Southern (NYSE: NSC) move large volumes of scrap metal.

As one example, Norfolk Southern advertises its role in serving more than 20 eastern states with its fleet of over 20,000 railway cars (freight wagons to most of the world) dedicated to the movement of both metals and other construction industry materials. Norfolk Southern trains directly serve:

- 37 integrated and mini steel mills

- 70 transload facilities

- 150 scrap metal processing facilities

CSX reports that about 87 percent of the nation’s steel is produced within the market footprint of its service network. The core of that steel network lies within the Illinois – Indiana – Ohio region and along the East Coast.

The customer’s point-of-view

Recycling of steel is a worthwhile economic business. One estimate suggests that that the recycling of one ton of steel can avoid the use of 2,500 pounds of iron ore, 1,400 pounds of coal and 120 pounds of limestone in making new steel.

Recycling Today states that from the shipper’s point of view, there are two daily business challenges. One is to obtain empty cars for loading. The other is to obtain a consistent pattern of empty cars delivered for loading on the days promised.

Here is the perspective of a large ferrous scrap shipper. David J. Joseph Company (DJJ) is a NUCOR subsidiary that does almost $300 million a year in railroad scrap business. DJJ operates 13 scrap metal brokerages. It operates 50 recycling yards with 15 auto-shredding facilities. This is not a small business. One source reports that DJJ is a $2 billion asset firm.

For smaller independent scrap brokers, the key to using rail is to assemble a large volume for movements that are typically 150 or more miles distance to a steel center or export port – thus beating the trucking costs.

How does the scrap market work?

Based upon personal observations, plus evidence gained from current business intelligence research, there is no sophisticated formal exchange market for pricing or arranging for scrap steel exchanges. There is certainly broad area scrap price information. But there is no scrap futures market.

The scrap market tends to be a cash business when its transacted. Sales of scrap often reflect volatile short-term price moves. Prices reflect both volume available at a location and the quality of the segregated and “sized” scrap piles to be transported.

Market prices can often be described as 30-day contracts. Transactions for scrap tend to be “subjective” as to terms.

As to market pricing, two regions determine the initial transaction prices long before a railway car gets loaded: China for U.S. West Coast scrap; and Turkey for U.S. East Coast scrap.

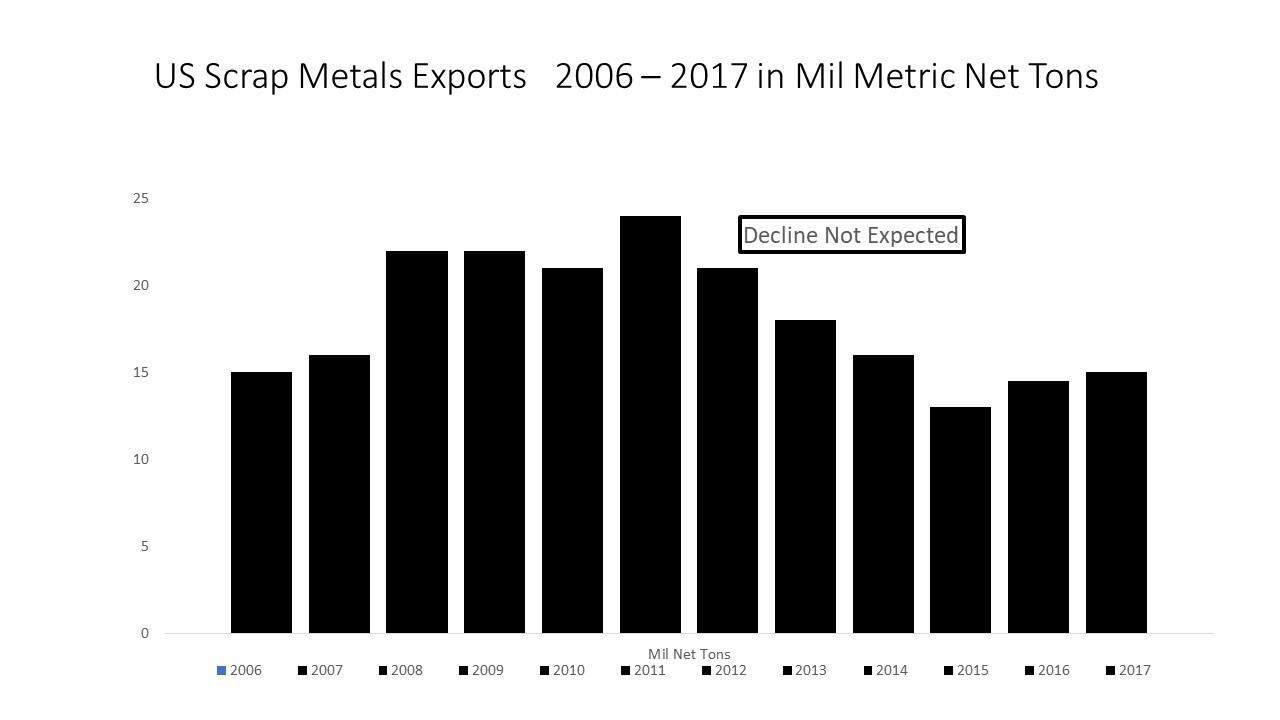

Domestic steel manufacturing market demand and market size no longer seem to be the principal drivers for scrap pricing. Instead, over the past two decades, the export market started to play a significant price-setting role.

The highest export scrap pricing occurred in the period 2010-2011 – and then the global market fell dramatically in the 2012 to early 2015 period. This corresponded to a drip in demand for U.S.-produced steel. U. S. scrap steel prices fell – sometimes by 50 percent or more.

The promises seen two decades ago of a large and continuing export scrap market hasn’t returned yet.

As exported scrap volume declined, scrap used to “charge” U.S. domestic steel mill furnaces hasn’t recovered to its previous market highs.

U.S. steel manufacturing capacity utilization rates in the 75 percent to 90 percent+ range fell in 2009 to less than 50 percent – and after a brief two-year recovery period back towards 80 percent utilization, then fell in a consistent downward slope back to less than 70 percent by 2017.

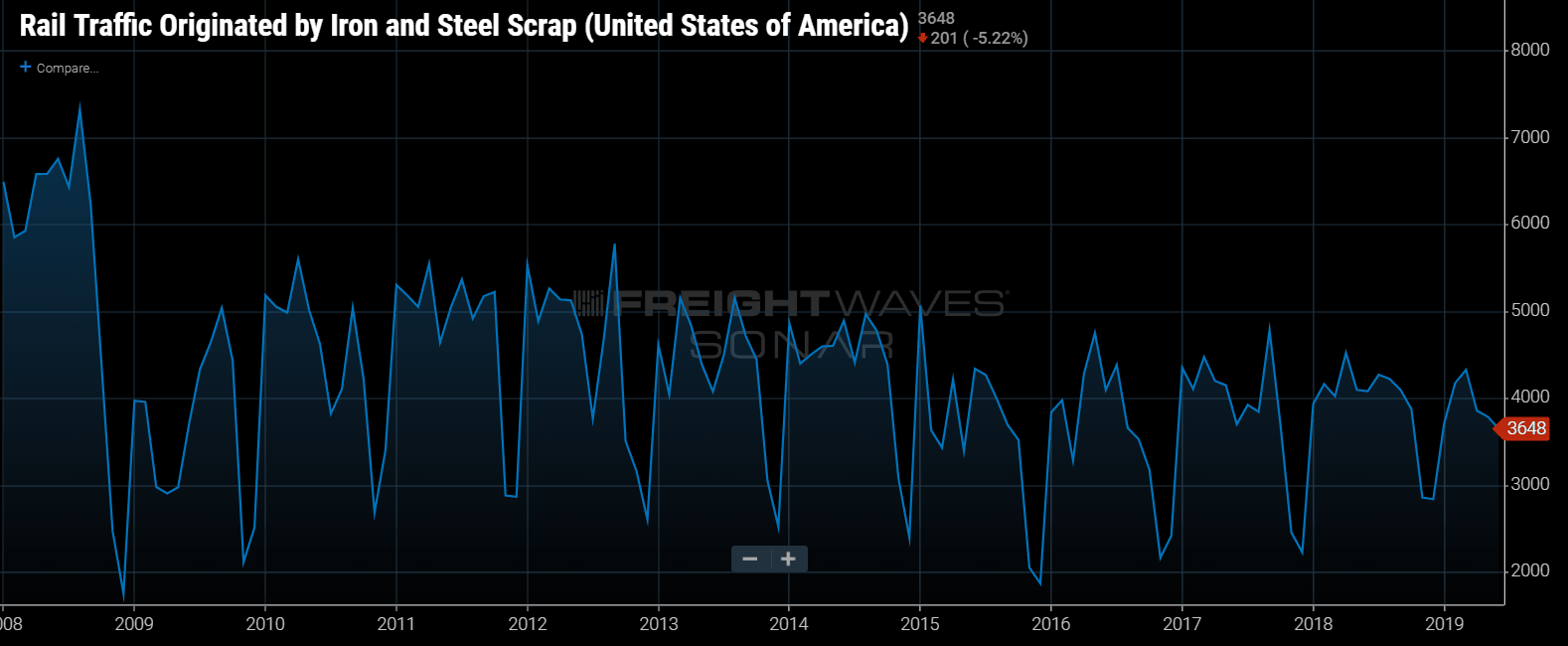

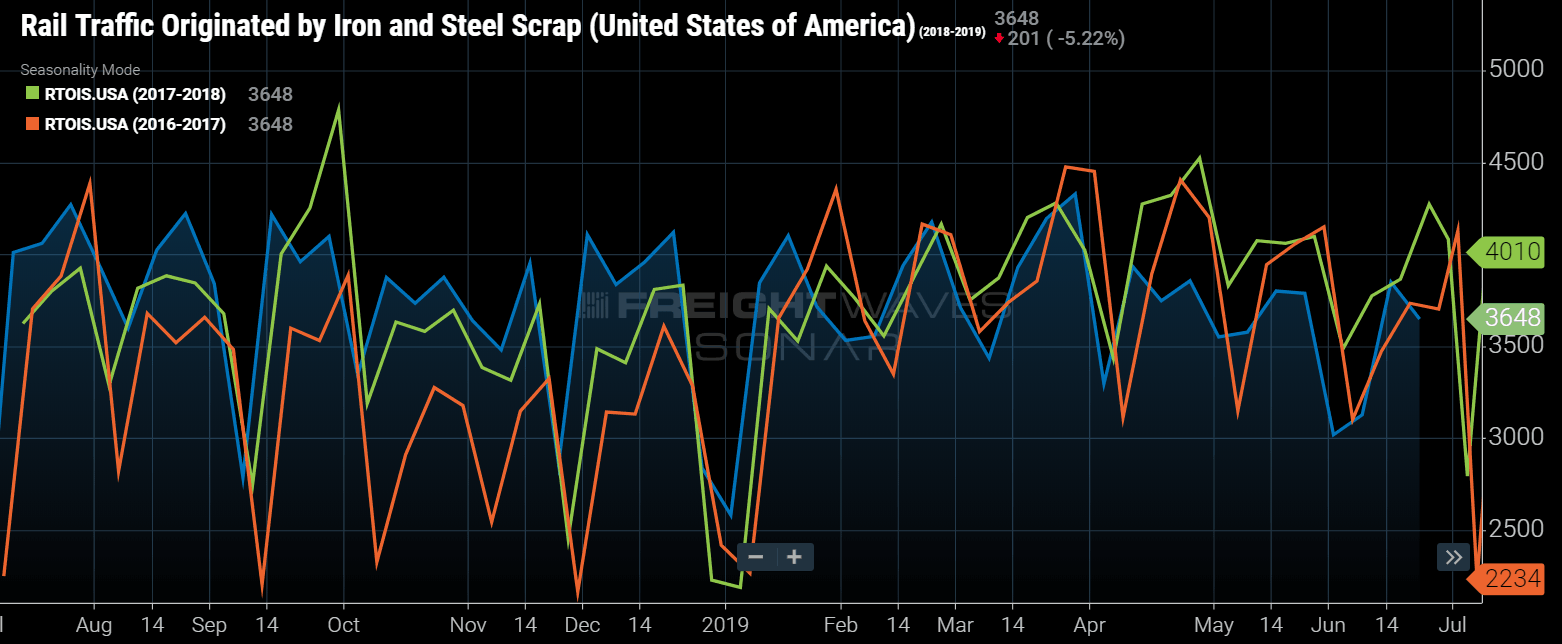

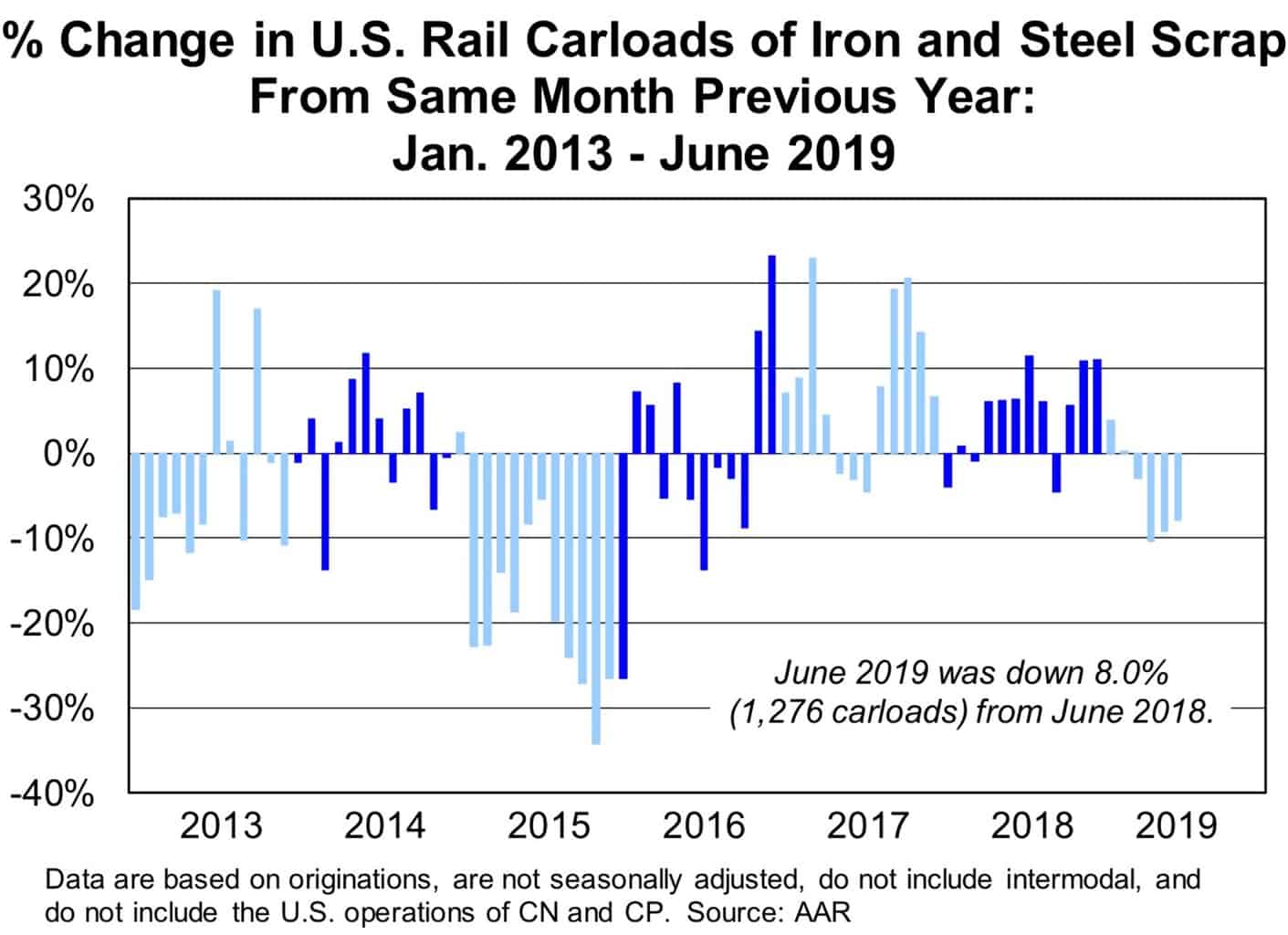

The cumulative impact has resulted is extreme volatility in the market price of scrap as seen below.

What is the current outlook for U.S. rail hauled scrap?

At best it is tenuous. At worst, it is highly questionable as a growth market.

Why questionable? Beyond 2019 geo-politics are fundamental challenges as steel and its scrap feedstock both face threats from source competition and product substitution.

The source competition comes as over time the expansion of China’s own durable and consumable steel products for goods like automobiles will see China’s mills increasingly sourced by nearby domestic scrapping. Imports of scrap will continue, but the percentage of imports to local Chinese scrap will change.

However, the largest scrap steel market threat may come from chemical-based product substitution of plastics and from emerging ceramics and composite materials.

As substitute materials are used more extensively, many economists see a significant drop in the Chinese steel consumption per capita from today’s high of ~500 kilograms.

Strategically, previous projections for a huge increase in China’s per capita steel consumption were based primarily on the growth pattern seen between the 1990s and the 2012 period. That was when China’s GDP increase was in the double-digit range.

It is time to reconsider those previous outlooks.

Impact on railway scrap business?

The resulting outlook for U.S. railway scrap steel is therefore one of low growth for a period – followed by a gradual volume reduction. To be sure, that is not a projected elimination of steel or scrap metals rail traffic.

Shifting market demand for ferrous scrap should lower gondola freight car replacement orders in the decade ahead. Railroads won’t order replacement gondolas as long as scrap prices remain low.

Over the next two decades, both railroad volume and scrap sector volume derived revenues should also start to fall.

As always, FreightWaves encourages discussion of counter arguments.

Acknowledgements: Credit for some data and market analytics include the following:

- Trey W. Savage at David J. Joseph from his REF17 presentation “Trends and Outlook for Scrap & Steel Related Gondolas”

- Railroad writer Lynn R. Novelli.

- Annual reports and selected quarterly reports and investor presentations made by CSX and Norfolk Southern managers in the period 2006 to 2018

Amy Winters

Thank you for pointing out that scrap metal is the combination waste of metal or metallic material that is capable of being recycled. My brother has been thinking about joining his friends in collecting scrap metal. It’s good to know that it is collecting metal that can be recycled.