The US trade deficit in goods widened for the third consecutive month in August as another decline exports was paired with a modest increase in imports. The total value of traded volume fell for the month, but remains generally strong relative to last year.

The Census Bureau reported that the US economy’s goods deficit widened in August to -$75.8 billion dollars on a seasonally adjusted basis, from a revised -$72.4 billion in the previous month. This marks the third straight deterioration in the US trade picture, and nears the record high for the deficit of -$76.0 billion set in February of this year.

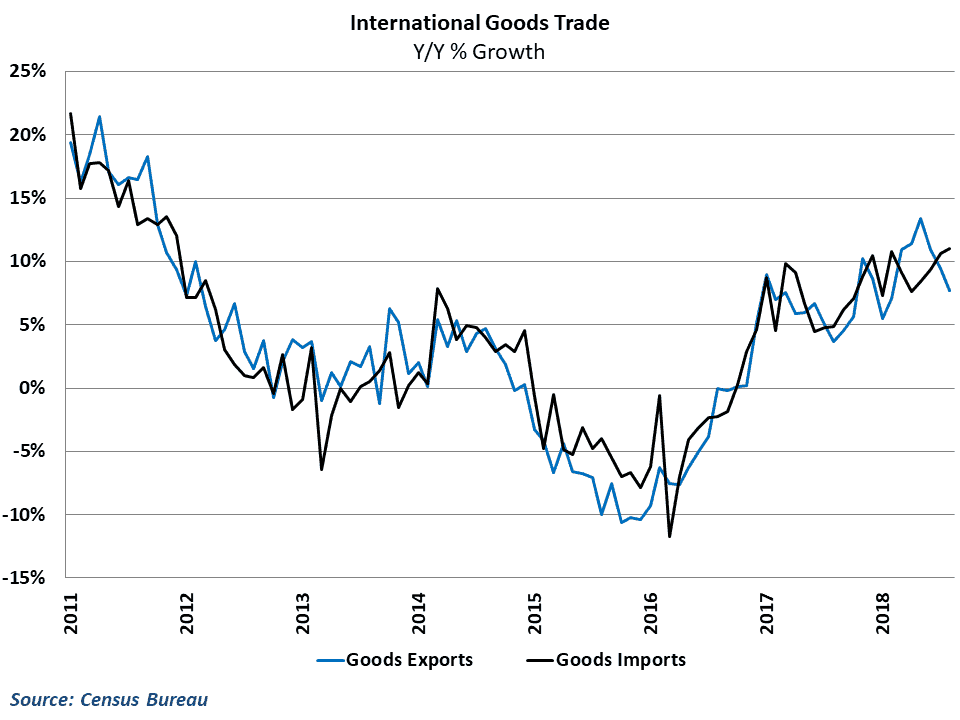

Struggling exports again were the culprit in August, declining -1.5% from July’s levels. Year-over-year growth in exports has tumbled during over the past few months, falling to 7.7% after hitting multi-year highs in May of this year.

As has been the case for the past couple of months, the decline in August is likely payback from a tariff-related surge in the 2nd quarter of the year. The Trump administration began rolling out its plans to implement tariffs on various goods earlier this year, with a particular focus on China. These moves prompted response from the rest of the world, with a variety of retaliatory tariffs scheduled for this year. GDP results showed that international trade added over a percentage point to growth during the second quarter, as many US exporters rushed to get their products out of the country before any retaliatory tariffs from the rest of the world could take place.

The details from August suggest that this surge simply pulled activity forward. Exports during the month were weighed down by a -9.5% decline in food, feed, and beverage exports, which is likely driven by the surge in soybean exports to China in the 2nd quarter.

On the import side, tariff-related concerns may also be contributing to the recent growth in the amount of goods being brought in from the rest of the world. Goods imports rose 0.7% in August, as year-over-year-growth climbed to 11.0%.

The Trump administration began imposing tariffs on China in July, and has followed with announcements of significantly more tariffs on Chinese goods in the upcoming months. As a result, US businesses appear to be bringing in more goods now and storing them in inventories to avoid future tariffs. Data on inventories also showed a sizeable increase during the month, in part reflecting the trends in imports.

Implications for the economy, freight

As a result of falling exports and rising imports, net trade is expected to be a large drag on GDP growth when 3rd quarter results are released next month. Expectations are that net exports will subtract nearly two percentage points during the quarter, which will cause GDP growth to slow overall from the rapid growth seen in the 2nd quarter.

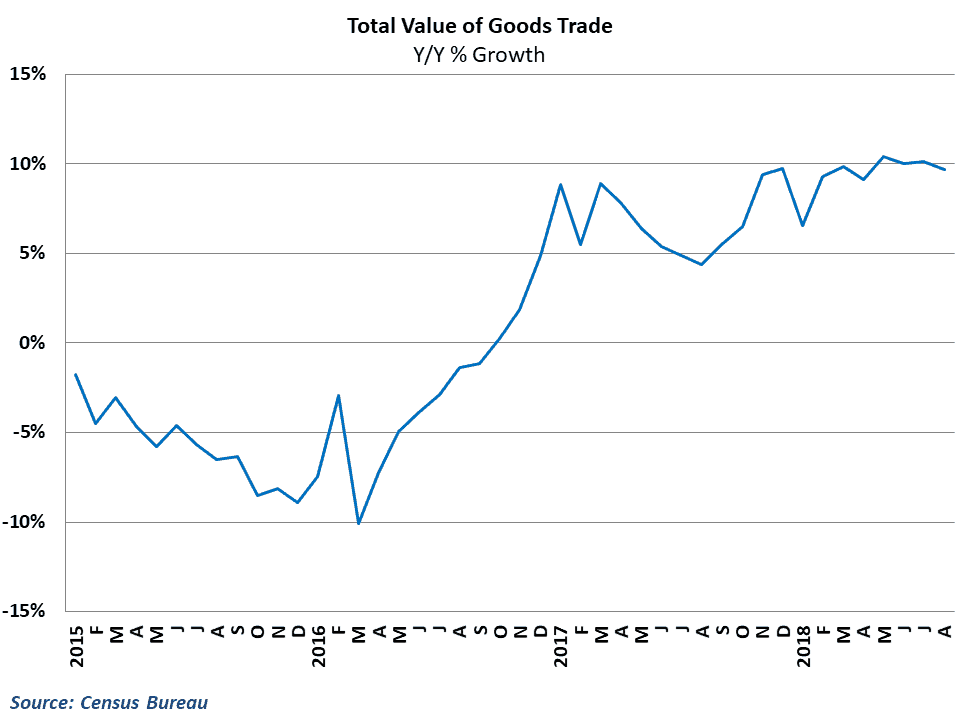

Of course, from a freight perspective it is more important to pay attention to the total amount of goods being transported instead of the size of the trade deficit. Both imports and exports require freight movements, and as long as the amount of trade is strong, carriers that are involved in these movements will benefit. To that end there has also be some deterioration, as the total value of goods traded has fallen in each of the past two months. However, the decline has be far less pronounced, and growth in the value of traded goods remains near 10% despite all of the recent tariff-related noise.

Behind the numbers

The tariff-related forces on both the import and the export side are making it difficult to discern what the underlying trends in exports and imports are. At the same time that businesses are shifting around purchasing patterns to prepared for potential future tariffs, the dollar has been gaining value and global growth conditions in the rest of the world have weakened relative to the US. This would also have the effect of weighing down exports and boosting imports, and right now it is unclear how much to attribute to tariffs vs. market forces.

This distinction means very little for the current environment; whether it is tariffs or market forces the fact is that exports are in a tough spot right now. However, it does have some significant implications for the outlook. The next couple of months of data should go a long way to understand how permanent this deficit-widening environment will be going forward.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.