Late last month, the Organization of Petroleum Exporting Countries made a decision to expand the amount of oil that it would supply to the rest of the world, ending an 18-month period which saw output capped to boost prices in the oil market.

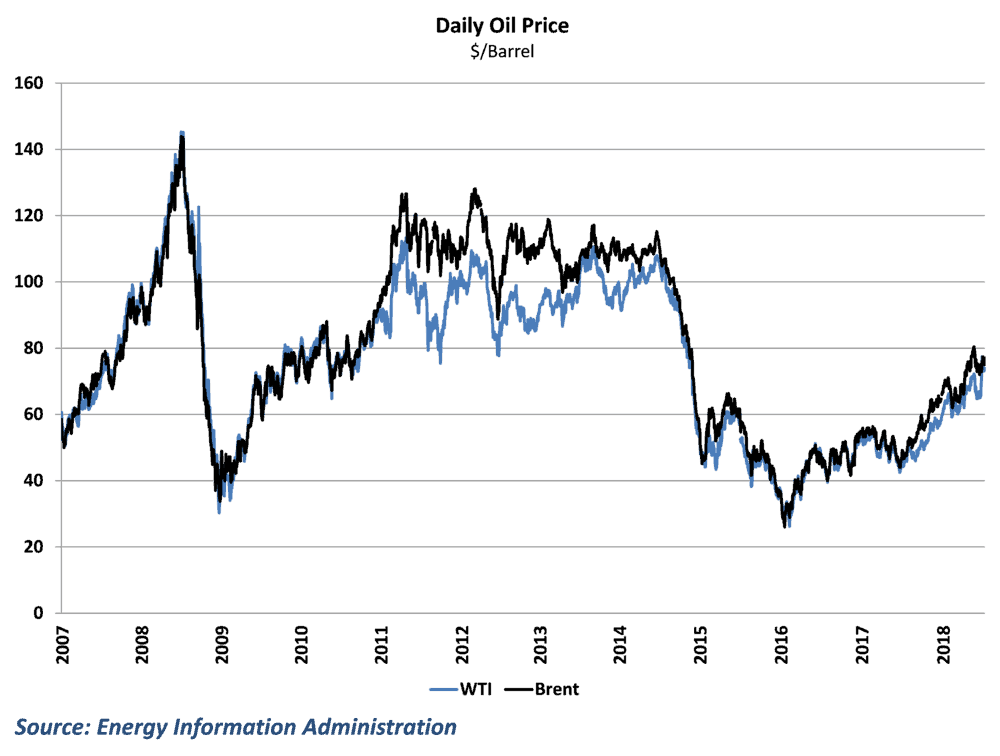

The increase in oil supplies has brought some stability to oil prices, which had climbed from nearly $25 per barrel at the end of 2016 to over $80 per barrel in May of this year. Prices have since retreated slightly in recent weeks, but remain elevated relative to recent history. This, in turn, has stoked some concerns that the high cost of oil and gasoline may curb the momentum in the economy.

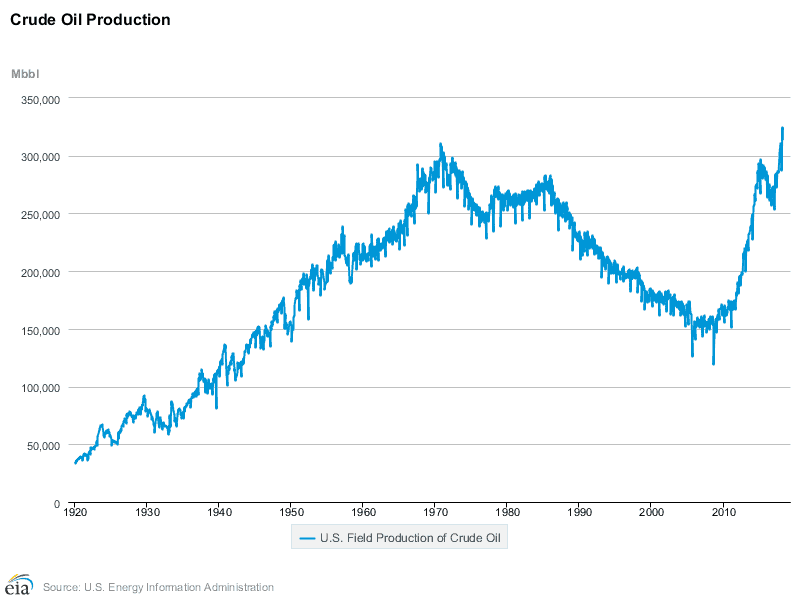

The classic narrative on oil and the economy stems from the pre-recession experience in the US, when the country imported large amounts of oil from the rest of the world and faced declining production from aging oil rigs in the domestic economy. US field production of crude oil fell over 40% from 1985 through 2007, while consumption of oil increased steadily before leveling off in 2005.

Against this backdrop, rising oil prices were a fairly clear-cut negative for the economy overall, as it meant rising costs for fuel and production for consumers and businesses. Surges in oil prices had negative economic consequences in the early 90’s, early 2000’s, and again in the summer of 2008, helping to reinforce the idea that high oil prices were bad for the economy overall. Similarly for trucking, the basic idea had been that rising oil prices meant less freight and higher fuel costs which may or may not be passed on to shippers in the economy.

A switch in conditions

So ingrained was this narrative that when oil prices fell at the end of 2014 due to rising US production and high OPEC supply, most expected a big boost to economic activity. Falling prices would be a big boon to consumers and businesses, serving as a sort of implicit tax cut and providing a jolt to the economy.

The results were actually quite different. For one, consumers and businesses that benefited from lower fuel costs ended up pocketing much of the extra savings instead of spending significantly more on goods and services. In addition, oil consumption in the economy has generally plateaued since the great recession and has yet to return to pre-crisis levels as consumer and businesses have gotten more fuel efficient. (The Energy Information Administration’s proxy for demand, called Product Supplied, crossed the 21-million b/d mark several times on a monthly basis in 2005-2007. It has yet to return to that level.)

Perhaps more importantly, conditions in the oil industry had changed significantly in the post-recession period. The emergence of hydraulic fracking, combined with horizontal drilling, allowed the US to tap into large shale oil and natural gas reserves, which helped drive investment in new oil rigs in the economy and helped double US crude oil production between the end of the recession and the end of 2014. The number of active oil rigs in the economy rose nearly eightfold during this time, which helped drive additional spending on machinery and equipment for use in fracking. This, in turn, had positive implications for freight markets. We at FreightWaves estimate that each additional rig generates nearly 1 million additional miles for truckers in the economy.

As a result, the decline in oil prices snuffed out one of the key drivers of growth in the economy. Investment in mining and drilling activities plummeted in the aftermath of the oil price decline, and the number of active rigs fell more than 75% from the start of 2015 through the end of 2016. Industrial production, which had been a source of strength in the economy throughout 2014, saw negative growth in 2015 and 2016 amid large cutbacks in mining and supporting industries.

Not coincidentally, this was also a difficult time for the trucking industry. Lower oil prices did reduce fuel costs, but all of the tonnage associated with the fracking industry largely disappeared. Carriers that were heavily involved in the energy sector, carrying fracking sand and equipment to rigs, saw much of that business decline significantly in response to oil price drops.

So rising oil prices are a positive?

As a result, there is an increasing belief that rising oil prices are good for the economy and trucking overall. Certainly there has been a revival in activity around the mining sector over the past 18 months as oil prices have climbed. Mining production has enjoyed double-digit growth throughout 2018, pushing to record highs by the middle of the year. The number of active oil rigs has not returned to previous levels, but has more than doubled since its trough as producers restarted some previously dormant rigs. This increase in activity has played a role in reviving freight markets, creating an additional source of demand for trucking and rail services and offsetting some of the additional costs that come with higher fuel prices.

In addition, the rise in prices has restarted investment in new rigs and drilling in the economy. Late last year, the World Bank estimated that the break-even price for existing shale drilling rigs is about $30-$35 per barrel, while prices above $50-$60 per barrel help to stimulate new exploration and drilling. This has helped spur growth in machinery production and new drilling equipment.

Moreover, consumers and businesses haven’t shown any significant signs of slowing their spending in the face of rising oil and fuel prices. Overall inflation has ticked up recently in the economy, but households have continued to buy and businesses have sustained high levels of investment in the economy. Overall GDP has accelerated fairly steadily over the past several quarters, which would indicate that the economy overall has been helped rather than hurt by the gain in oil prices.

Positive, to a point

Still, I would caution against reading too much into the recent experience with oil prices. For one, much of the reason why consumers and businesses have not been hurt by rising oil prices this year is because they have also benefitted by tax cuts put into place at the start of the year. These tax cuts have offset much of the potential negative impact and allowed the economy to largely shrug off the higher oil prices.

More importantly, there are some limits to how much additional oil will be generated by higher oil prices. Pipeline capacity has become an issue in the economy, as producers in the Permian basin have already started to push up against limits. Additional pipeline construction is in the works, which has helped economic activity, but current capacity has imposed some restrictions on how much additional drilling and mining will result from a higher oil price.

Tariffs on steel and aluminum have also affected the mining sector, as many of the machines and equipment used in the exploration and mining process are made from these metals. These tariffs, enacted in March, have imposed further costs on the oil industry and have reduced the profitability of exploration and mining at any given price.

In addition, the mining sector is running up against the same constraint that has plagued many other sectors in the goods side of the economy: they cannot find trucks to move the freight. Rates for trucking services connected to the energy sector have surged during the year as capacity constraints take hold, further affecting the profitability of oil production. And with unemployment near historic lows at 4%, the challenges of finding quality skilled labor have affected oil producers as well.

All of this to say that the relationship between oil prices and the economy is more complicated than it seems on its face. While the recent rise in oil prices has probably had a modestly positive effect on the economy so far, higher oil prices are positive to a point. There is no guarantee that any further increases will help the economy further.