With the latest OPEC meeting in the books – now dubbed OPEC+, more on that later – the usual hand-wringing about OPEC’s lack of power, incompetence and irrelevance poured through the writeups from the Vienna gathering.

Liam Denning of Bloomberg summed up that view in an analysis from the meeting:

“The very fact that OPEC has tried to rope in ever more pledgers and shows so much deference to Moscow demonstrates its inherent weaknesses. The biggest of these is the sheer overweening dependence of many of its members on their favorite commodity. This makes them all fragile in an oil market that has become more competitive – especially as U.S. shale supply surges on the back of any price increases – and is subject to building constraints on demand. The big problem here is that ongoing pledges to cut supply are ultimately a sign of weakness in the oil market, not strength. “

That’s one way of looking at it. Another is that if OPEC was even more incompetent, where would the price of oil be? And what country’s oil and gas sector would be feeling the brunt of that decline?

The answer is: a) we don’t know, but lower; and b) almost certainly the United States as well as Canada’s oil sands region.

When you look at the big supply/demand picture in the oil market today, the true scope of what could be the glut to end all gluts becomes stark. If the market is roughly in balance now between supply and demand, where would it be if Venezuelan economic incompetence – topped with U.S. sanctions – hadn’t sunk production to about 750,000 barrels/day (b/d)? (It was about 1.9 million b/d in 2017 and if the country was run correctly, it could easily be over 3 million b/d.) Where would it be if U.S. sanctions on Iran hadn’t dropped production down to about 2.5 million b/d – maybe less – from 3.8 million b/d in 2017? What if peace among our fellow men took over Libya, Sudan and Nigeria? Where would their production levels be?

Even with all of those declines, the International Energy Agency forecast for 2020 is that the “call” on OPEC crude – the amount of supply needed from the group to balance it with global demand – is 29.3 million b/d. The S&P Global Platts estimate for May is that OPEC produced 30.09 million b/d. That’s a 700,000 b/d gap and it comes after OPEC’s output was over 33 million b/d just last November.

OPEC didn’t do much to further close that gap at its recently completed meeting. It rolled over its existing 1.2 million b/d cut that it agreed to in December, two-thirds of it to be supplied by OPEC and the other third by its new partner, the OPEC+ nations that are led by Russia. But the two sides together are more than 160 percent in compliance with the 1.2 million b/d cut. That’s another roughly 700,000 b/d removed from the market beyond the 1.2 million b/d target.

Which brings us back to the question of OPEC competence. Beginning about eight years ago, U.S. production began to rise as the shale revolution spread from natural gas to oil. It had stabilized and ticked up slightly about two years before that when the marriage of horizontal drilling and fracking first started to bolster oil production.

U.S. output crossed the 6 million barrels per day threshold in late 2011. In April, the last full month that the Energy Information Agency (EIA) has supplied data, it was 12.1 million b/d.

The broader backdrop is that world demand rose about 10 million b/d during that period, and the U.S. took about half of that. Throw in gains from Russia, Brazil, Canada – the number of non-OPEC countries that increased their output is a long one – and you see OPEC’s dilemma.

And how did OPEC perform in its self-proclaimed role as defender of the price? You could argue that the answer is “pretty good.” The 30.09 million b/d figure for OPEC’s May production means that in seven years, OPEC (adjusted for the exit of Qatar last year) has increased its output a grand total of about 200,000 b/d from its 2012 level (according to EIA data).

Think about that – world demand for oil went up about 10 million b/d since 2012, from roughly 90 million b/d to 100 million b/d, and OPEC’s restraint led it to claim just about 2 percent of it.

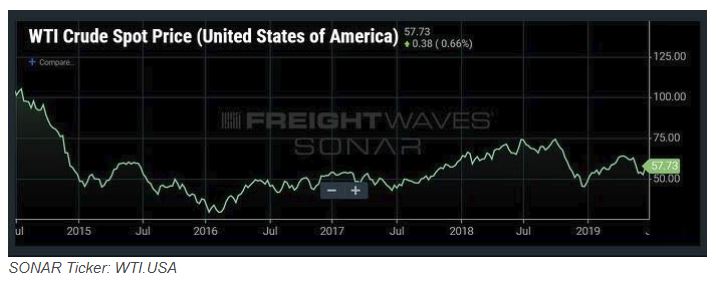

This is failure? It’s true that OPEC was completely blindsided by the shale revolution. Its first reaction was to continue producing as if nothing had happened, figuring this startup pipsqueak would collapse under the weight of its debt levels and relatively high production costs. It didn’t happen and a WTI price that in 2012 generally stood around $90/barrel was down to $30 in February 2014.

But OPEC did get serious about restraint after that and the price of WTI rose to $75 by mid-2018. The rising weight of shale production, increases in production from other non-OPEC nations and relatively tepid demand growth pulled that market back to its current level near $60.

What sort of credit should OPEC get for the current price, roughly $30 more than its 2016 low? Imagine if your own industry went through a roughly 10 percent increase in size in seven years. Outside of the fact that it would be illegal, how many manufacturers of widgets – the old economics class standby – would be willing to get together with a few other widget makers, give up virtually all claims on any of that growth and hope to be compensated for that restraint by better returns from the higher prices of widgets?

This is exactly what OPEC has done. And here at the end of all of it, it’s probably not going to be enough. Its output is still high compared to what is needed and it’s unrealistic to expect much more help from declines out of Venezuela and Iran. (Libya could always erupt too but its output has been remarkably resilient, though certainly less than it was before the fall of Qaddafi.)

The fact that the call on OPEC crude in 2020 is less than that of 2019, and less than what the group is producing now, means that the group of nations that let the rest of the world grab almost all the demand growth since 2012 will need to give up even more market share next year.

What would the world have looked like if OPEC hadn’t done that? The answer to that is easy in the sense that when supply of widgets exceeds demand for widgets, the highest-cost widget makers are pushed out of the business.

What OPEC has done since the shale revolution began is to take on the role of the highest-cost widget maker, even though they’re not, resulting in the highest-cost widget makers, primarily in the U.S. and Canada, being able to sell at a price that offers more of them the prospect of continuing their operations.

This is why the attempts to punish OPEC through the so-called NOPEC legislation have a whole lot of unintended consequences related to them. If OPEC ceased its efforts to restrain supply, where does the price of oil head? Remember, it briefly reached $30 in 2014 when the shale fields were starting to ramp up and OPEC was limiting its restraint. If OPEC abandons all restraint and goes toe-to-toe with the shale fields again, where does the price of oil end up?

It certainly ends up lower. But then what are the consequences to the U.S.? The U.S. is still a net importing nation. But if you toss out Canadian supplies which are heavily attached to the U.S. through pipelines – it isn’t likely to go anywhere else – the U.S. is a net exporter of oil.

That has allowed the U.S. to do things like put sanctions against Iran to squeeze it as part of pushing back against its nuclear ambitions. It has allowed it to place sanctions on Venezuela, hoping to push that authoritarian government out of power. The natural gas that has come along as part of the shale revolution has turned the U.S. into a major LNG exporter with all the foreign policy advantages that has created.

And from frac sand miners in Wisconsin to truck drivers in the Bakken to thousands of workers in the Permian Basin – including the burger chefs at McDonald’s in Midland/Odessa making close to $20/hour – the shale revolution has been a boon in hundreds of thousands of workers’ pockets, to say nothing of the royalty payments that have flowed to landowners and state and municipal governments.

What if OPEC just took its ball and went home?

Consider the current landscape for U.S. producers, even with OPEC holding back supply to support the price. The U.S. industry increasingly is getting squeezed. It’s already under tremendous pressure to grow up and start doing things like generate steady free cash flow and return profits to shareholders via dividends. That investor pressure has been strong enough that even a solid shale company like Pioneer Natural Resources has seen its stock decline about 20-plus percent in the last 52 weeks despite the fact that it actually pays a dividend, albeit with a small yield of 0.44 percent.

The demand for better performance is squeezing enough companies that this past week, Weatherford, a long-standing oil service company, filed for Chapter 11 protection in U.S. Bankruptcy Court.

If OPEC was the abject failure that some people are describing it as, the U.S. sector without it looks a lot smaller. From a trucker perspective hauling reefer or dry van loads, that might be a good thing. The price at the pump is less; for them, that’s an unmitigated benefit.

But a lot of those truck driver jobs in the oil fields go away to say nothing of production jobs, which generally pay more than the drivers. So does a lot of the rail hauling of frac sand. The U.S. starts to become more of a net importer of oil after years of watching that dependence decline, weakening those foreign policy advantages. Original equipment manufacturers building equipment for the oil fields see some of that business disappear.

OPEC’s market share would be higher. It doesn’t need to be stuck claiming just 2 percent of growth anymore.

Most importantly, the price at the pump is lower.

Is that a good tradeoff for the U.S.? That is what would happen under a full fail by OPEC. Given that scenario, is what’s going on now with OPEC really a failure?

Be careful what you wish for; you might just get it.