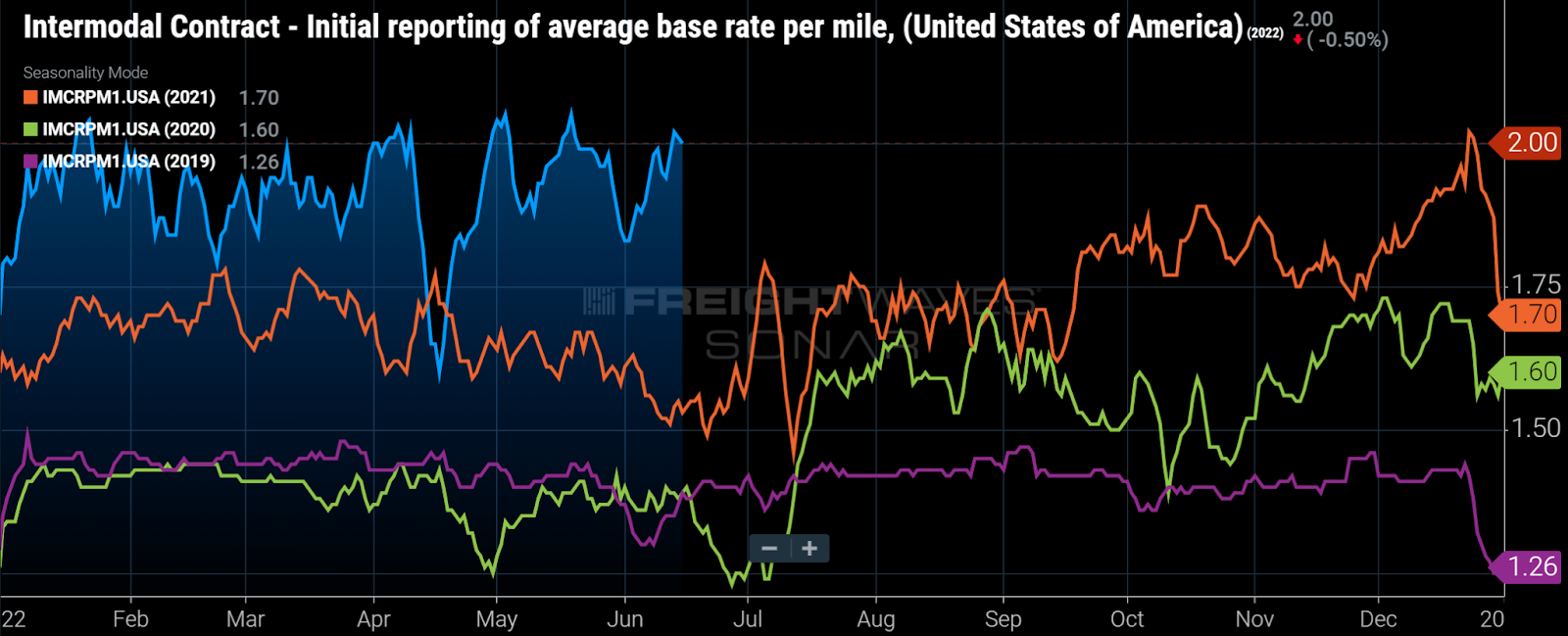

General Mills’ supply chain disruptions to persist

At a Wall Street conference earlier this month, Jonathan Nudi, General Mills’ president of North American retail, said, “We’re seeing 10 times the number of disruptions in our supply chain from an ingredient standpoint coming into our plants than we ever experienced before. And this gets really challenging because we can’t see them coming in many cases. So a truck is supposed to show up with oil at our refrigerated dough plant in Tennessee and doesn’t show up. So we have to shut the line down. Obviously, that creates lots of issues in terms of having the right amount of product and supply to our customers. And at the same time, it drives a lot of incremental costs as well. So we have thousands of these material disruptions every single month now, and it’s something that we haven’t seen before.”

One of the major takeaways from the company’s analyst call on Wednesday is that management does not expect supply chain issues to get much better in the near term. The company had previously told investment analysts to expect supply chain issues to create $200 million to $250 million of cost pressure on an annual basis — the equivalent to about a 500-basis-point impact to gross margin.

No evidence of easing food prices in General Mills’ results

General Mills’ cost inflation was 8% for its fiscal 2022 (year ending May 31) and it expects its cost inflation to be 14% in fiscal 2023. Management also said that its expectation for inflation for fiscal 2023 rose since closing its fiscal 2022 at the end of May.

After adjusting for M&A, pricing in fiscal 2023 is expected to rise about 15%, which should offset cost inflation and some of the incremental costs related to supply chain inefficiencies. General Mills’ share reacted positively to the earnings announcement, up 5%, and I believe that is, at least partially, attributable to a strong pricing expectation for the upcoming year.

Management is confident in that level of pricing because, so far, it has seen elasticities that are below historical norms. Management expects elasticities to increase some in its fiscal 2023 but still remain below historical levels — I consider elasticity to be the key question for the CPG space in the next one to two years. Aside from recent data, General Mills’ management expects that consumers eating more at home rather than restaurants will be a widely used cost-saving technique that provides a partial offset during a period of consumer retrenchment.

Under a new agreement, Ben & Jerry’s will again be sold in Israel

Last year, Ben & Jerry’s created a major headache for parent company Unilever when it stopped sales in east Jerusalem and the West Bank. This week, nearly one year later, Unilever announced that it sold all of its Ben & Jerry’s business interest in Israel to the owner of the Israeli licensee. Under the new agreement, the Vermont-based ice cream maker may continue to speak out against what it considers to be Israeli occupation of Palestinian territory, but Ben & Jerry’s ice cream will now be sold under its Hebrew and Arabic names throughout Israel and the West Bank under the full ownership of its current licensee.

According to Unilever, the 2000 acquisition agreement with Ben & Jerry’s allowed the ice cream maker’s board to make decisions about its social mission, but Unilever reserved primary responsibility for financial and operational decisions and, therefore, believes it has the right to enter this arrangement.

With consumer goods companies increasingly taking an activist approach on hot-button issues, this episode seems to demonstrate the limitations of that approach, particularly when a company is affiliated with a multinational that is a staple of state pension plans. While Ben & Jerry’s has a long track record of being outspoken on various causes, pulling out of Israel appeared to be an overreach, creating distractions for Unilever’s management team at a time when it was under the pressure of activist investors to improve margins by becoming leaner. Unilever’s announced corporate restructuring, going from three units to five, including making ice cream its own segment (which includes other brands in addition to Ben & Jerry’s), has led to speculation that Unilever might divest its ice cream business.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, please click here.