It isn’t just oil.

With the trucking industry’s most important benchmark oil number — the weekly Department of Energy/Energy Information Administration retail diesel price — rising for 11 weeks in a row, it’s important to note that the surge in oil prices is occurring against a backdrop of climbing commodity prices for almost everything.

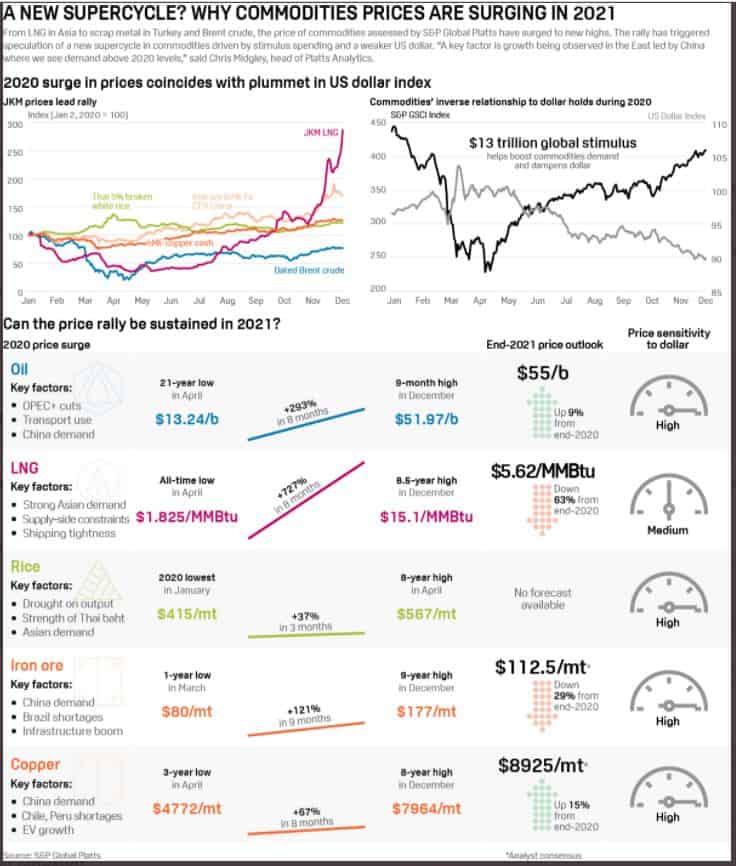

The benchmark U.S. copper price stood at about $2.17 a pound April 1. It’s now near $3.60. Lumber at about $660 per thousand board feet is off its recent highs but has been on a wild ride, jumping to $830 in the latter half of August, slumping to about $480 by the end of October and them jumping back to $840 in mid-December before its latest decline. Corn stood at $3.10 per bushel at the end of August before moving up to recent prices near $5.30 a bushel.

The craziest market might be liquefied natural gas in Asia. From a low of less than $2 per million BTUs in May, spot prices for sales of LNG into Japan recently crossed the $30 mark, propelled in part by an unusually cold winter in Asia and cutbacks in U.S. supply from associated oil production that was reduced on low prices.

In a recent podcast interview, Jeff Currie, the highly influential head of commodities at Goldman Sachs, looked over the commodities landscape and declared, “All this suggests a structural bull market is underway.”

That differs from a bull market in which the price of a commodity moves up by 20% from a starting low point. A structural bull is longer-lasting and brings in a wider range of commodities rather than a bull market in a single commodity or a random collection of them. Defining when they start and finish isn’t a precise art. But commodity analysts will tell you a structural bull commodities market ended in 1982 and a structural bear market in commodities ended in 1999. The 17 years between the two were viewed as fully encompassing a structural bear market.

With trucking and rail transportation intertwined with so many commodity markets, the prospect of trucking rates staying in check while there is a broad-based inflationary surge driven by commodities is unlikely. As FreightWaves has noted, there is a strong correlation between diesel prices and freight rates.

The question then is whether the movement in the price of diesel and the price of oil, and any concurrent movement in the price of freight rates, is leading commodity prices higher or whether they are just along for the ride.

Currie is in the school that sees the oil market as a leading indicator of commodity movements. He also sees it as a market that has uniquely been impacted by COVID-19. He didn’t mention trucking in his remarks but if oil prices are the leader in the commodity market movement, and there’s a correlation between freight rates and oil prices, it’s a quick jump in terms of seeing an impact on those rates from the booming commodity market.

“If you separate them out, the commodity most severely impacted by COVID is oil, because it sits in the center of social contacts and globalization,” Currie said in the Goldman Sachs podcast. Given that, he sees oil markets as a “vaccine play,” one where it would be expected that the greater penetration of the COVID-19 vaccine into the global economy will bring back more of that socialization and travel upon which so much of the oil market resides.

But Currie also said it is more than an oil-driven increase that is fueling commodity markets across the board. He said that in all the years he has been following commodities, he is witnessing something he has never seen before: “Every single commodity market is in a deficit today, meaning that demand exceeds supply.”

In the case of oil, the increase in the price of global crude benchmark Brent to more than $56 a barrel recently from near $40 as recently as early November (and below $20 at the market’s lowest point near the pandemic’s worst early days) has been held in check by inventories that were at almost record levels. In particular, U.S. inventories of non-jet fuel distillates, which is mostly diesel, were at record levels relative to consumption over the summer. Note that the percentage increases in the price of oil are not on the level of some of the commodities cited earlier in terms of percentages.

(Currie’s forecast for the average annual Brent price in 2021 is $65 a barrel.)

And while inventory levels have been drawing down in oil, it hasn’t been at the rate seen in other markets. For example, copper inventories on the London Metal Exchange, the world’s most important metals market, have been plummeting.

That supply/demand deficit across the board is created by what he said was “structural underinvestment in supply.”

Mike McGlone, the senior commodity strategist at Bloomberg Intelligence, had a different take on the commodity surge, noting that the increase in the price of oil is an outlier and its longer-term future is far less bullish than that of other commodities.

McGlone spoke of a “massive incentive to decarbonize” the economy. The oil market, even after its gains, faces the prospect of higher prices of U.S. shale output rebounding from its recent collapse but also is facing the possibility of “demand not coming back” because of the decarbonization trends.

Other commodities are benefiting from the combination of decarbonization and electrification, McGlone said, citing copper in particular. Copper’s key markets have always been tied to its role as one of the best conductors of electricity, so copper “is part of the new electrification and decarbonization economy,” McGlone told FreightWaves.

But copper supplies also are suffering from supply deficits in part because of the investment emphasis on environmental/social/governance (ESG) principles, which is seen as pushing investment out of less environmentally friendly activities like mining.

McGlone and Currie both see broader macroeconomic trends helping to drive the price of commodities higher. The decline in the U.S. dollar that has been going on since April generally has the effect of driving up commodity prices that are priced in dollars. McGlone noted that the entire world of agriculture looks to U.S. prices for commodities generally delivered on a major waterway like the Mississippi.

Currie cited the underinvestment in supply as one “theme” of his bullish outlook for commodities. But he had two other themes that he said were driving markets.

One is current “social policy-driven demand.” Currie talked about the dot-com boom from 20 years ago draining capital out of old economy activities like oil drilling, with the result that underinvestment culminated in the surge in prices that topped out at $145 a barrel for West Texas Intermediate crude in 2008.

“This time, instead of the dot-com boom, it’s the banks” Currie said, noting banks’ reluctance to invest in oil and gas drilling. He added that it isn’t just oil: “I see it across the board in metals, mining and agriculture,” he said.

Currie also said the reaction to COVID-19 is one that involved “accommodating social needs … policy will be directed at lower-income households that consume much more of the stimulus” than save it. The impact on commodities is a boost in demand, as opposed to steps taken in 2009 and 2010 to shore up banks, which would not have put money into consumers’ hands to do things like buy commodity products.

More articles by John Kingston

Why the feared IMO 2020 spillover effect on diesel markets didn’t happen

Key price spread in diesel market affirms tightening inventories

Good news for diesel consumers, tough news for oil patch drivers in federal report