The expectation for truckload (TL) contractual rates to increase by double digits in 2021 is growing. In a Wednesday note to clients, UBS (NYSE: UBS) transportation equities analyst Tom Wadewitz outlined the fundamentals supporting this projection.

“The current extreme tightness in the TL spot market plus a constructive outlook on freight point to double-digit rate increases in 2021,” he concluded.

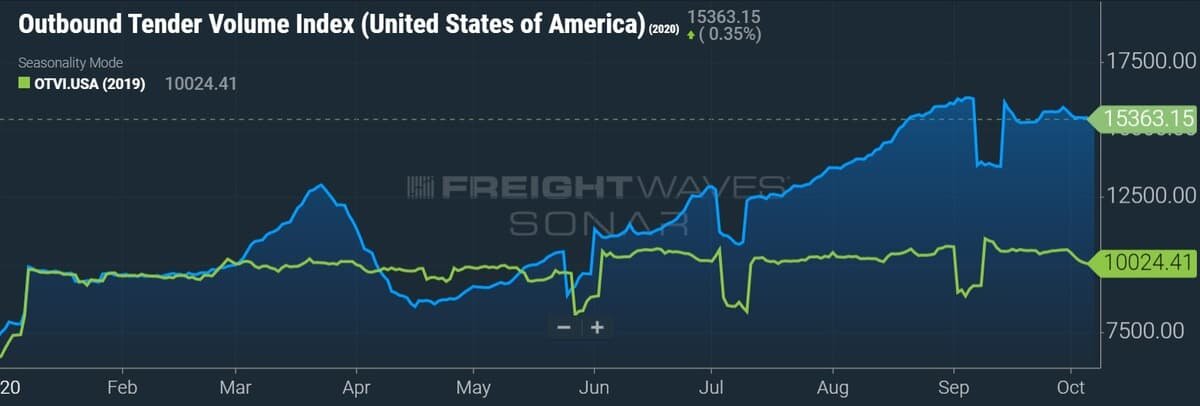

Wadewitz said recent spot market metrics “show a market that remains on a trend of further tightening.” He noted all-time highs in the number of loads in the spot market and a lack of available truck capacity to haul those loads as catalysts for his thesis. He expects “demand to remain strong through peak season and into 2021 as inventory replenishment likely remains a tailwind.”

The note followed a late-September publication from Chattanooga, Tennessee-based TL carrier U.S. Xpress (NYSE: USX) in which the company laid out similar contributors – higher driver turnover, declining TL capacity and “overwhelming” volumes – that are likely to push TL rates higher over the next year-plus. Management from the company had previously indicated that rate increases in 2021 needed to be in the 10%-plus range to recoup the impact of the last two negative bid cycles and two years’ worth of cost inflation.

Demand here to stay?

The new at-home lifestyles adopted by consumers during the pandemic have resulted in accelerated online spending and a large shift in buying habits. Trips and in-person experiences have been replaced by increased spending on food and beverage and other consumer-packaged goods as well as large-ticket exercise and home entertainment items. The changes mean more freight is being hauled by truck. Further, lean inventory practices were exposed in the early days of the virus outbreak and many supply chains are still struggling to restock items. Some companies have vowed to carry more inventory than in the past to avoid future supply shocks.

This demand dynamic is the current backdrop for the trucking market, which has entered peak season and has a robust holiday spending season on the horizon.

On the outlook for goods spending moving forward, UBS is expecting mid-single-digit increases year-over-year through the first quarter, with the second quarter registering a 10% increase. These growth rates are expected to be accomplished by increases in employment and income and a “more normal level” of spending as a percentage of income. A return to spending on services will present a modest headwind to goods purchasing.

“This framework points to continuing growth/strength in the intermodal and truckload freight markets through 1H21, which in turn should support strong contract pricing gains in 2021,” stated Wadewitz.

Consumer spending increased 1% sequentially in August, according to the Department of Commerce. The increase in spending continued a streak of month-over-month gains since registering a 12.7% decline in April. The seasonally adjusted metric is still approximately 3% lower than pre-COVID levels but almost 19% higher than the April bottom. Importantly, consumer spending increased as personal income fell, down 2.7% during the month. August was the first month without the help of enhanced unemployment benefits afforded under the coronavirus aid package.

Rates to surge in 2021

Wadewitz pointed to the 2018 rate cycle, when spot rates peaked 30% higher year-over-year, as a basis for increases in 2021. He noted that the spot-rate surge in that period led to mid-teen percentage increases in revenue-per-mile metrics for carriers like Werner Enterprises (NASDAQ: WERN). Rate changes in the spot market provide a basis from which carriers and shippers negotiate new pricing as contracts come up for renewal.

Spot rates have remained positive year-over-year since mid-June, with the gap to the prior year continuing to increase. Currently, rates sit 40% higher than they were in 2019.

“With the potential for spot rates to be up 30%-40% going into bid season, we believe the truckload and intermodal names could realize high-single to low-double-digit contract rate increases in 2021,” Wadewitz said.

The analyst raised his earnings-per-share (EPS) estimates for 2021 and 2022. He increased EPS by 23% on average in 2021 and 17% in 2022 for the carriers he follows. He also modestly raised his forecasts for the third and fourth quarters of 2020 again.

Price improvements pass directly through a carrier’s income statement to the operating income line without any cost offsets. However, most carriers share some of the rate increases with drivers as an increasing rate environment is accompanied by a tight capacity environment, highlighted by difficulty attracting and retaining drivers. When the TL market tightens, driver recruitment costs and pay rates historically move higher, offsetting some of the newly captured revenue stream.

Risks to Wadewitz’s double-digit rate increase thesis included a slowdown in the economy, more drivers entering the market than expected and higher than forecasted cost inflation for driver pay and retention. Wadewitz shot down the argument that new capacity will flood the market, potentially disrupting the current supply squeeze. He noted that Class 8 truck orders of more than 31,000 for the month of September marked only the first time in nearly two years that new orders were above replacement levels. Further, he views recent employment data as having “a very slow pace of increase in drivers.”

Another headwind to a double-digit rate increase in 2021 could depend on the type of rate actions taken in the last two quarters of 2020. Many carriers have noted the rare opportunity before them to raise rates on contracts ahead of their scheduled renewal. At a recent investor conference, several carriers said they were engaging in mini bids and out-of-cycle rate conversations with shippers as they look to lock in higher rates now and avoid the risk of not having truck capacity in the months to come.

Wadewitz’s forecasts for the remainder of 2020 assume high-single-digit increases in revenue-per-mile metrics for some carriers, potentially creating a tough year-over-year comparison in the back half of 2021.