Container lines have “blanked” (canceled) an unprecedented number of sailings to bring capacity in line with coronavirus-stricken cargo demand.

Blank-sailings data is a key leading indicator for U.S. ports, cargo shippers, truckers and railways. A container ship that doesn’t depart from Asia equates to a container ship that doesn’t arrive on the U.S. West Coast two to three weeks later, or on the East Coast four to five weeks later.

What matters to American businesses is U.S. port arrivals, not foreign departures. American businesses want to know exactly how much arrival capacity will be reduced, exactly when it will be reduced, and how this reduced capacity will compare year-on-year.

Copenhagen-based eeSea — a platform founded in 2016 that maps container-industry schedules — has provided a snapshot of this U.S.-arrivals-centric data on blank sailings to FreightWaves.

The latest information, updated on Sunday, shows changes to headhaul capacity from Asia to North America, as well as changes to mainline capacity to individual U.S. ports. Taken together, this data offers the clearest publicly available picture yet of how the coronavirus is affecting the container-shipping network that supplies America.

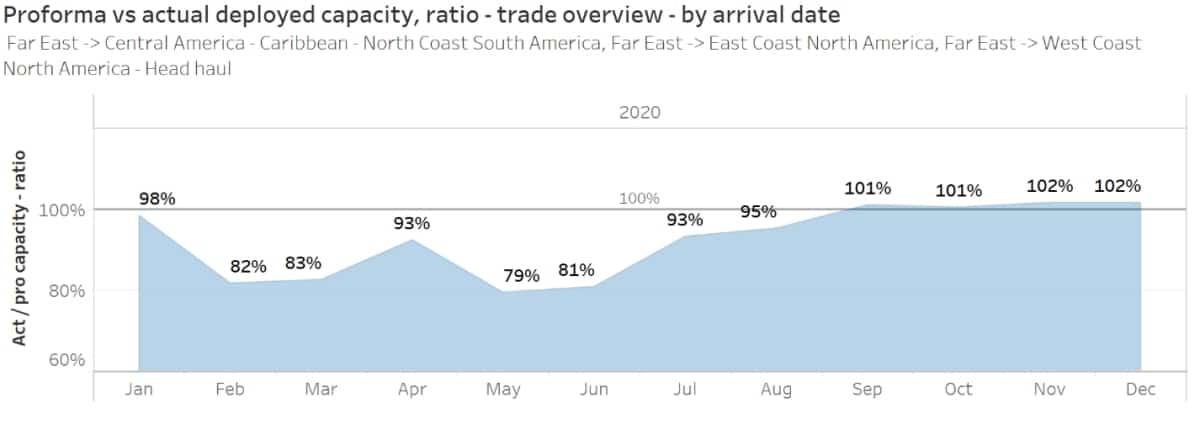

Reduction in Asia-US sailings

According to eeSea data, 51 of 243 scheduled North American arrivals from Asia have been cancelled this month; 44 of 236 next month; and 23 of 240 in July.

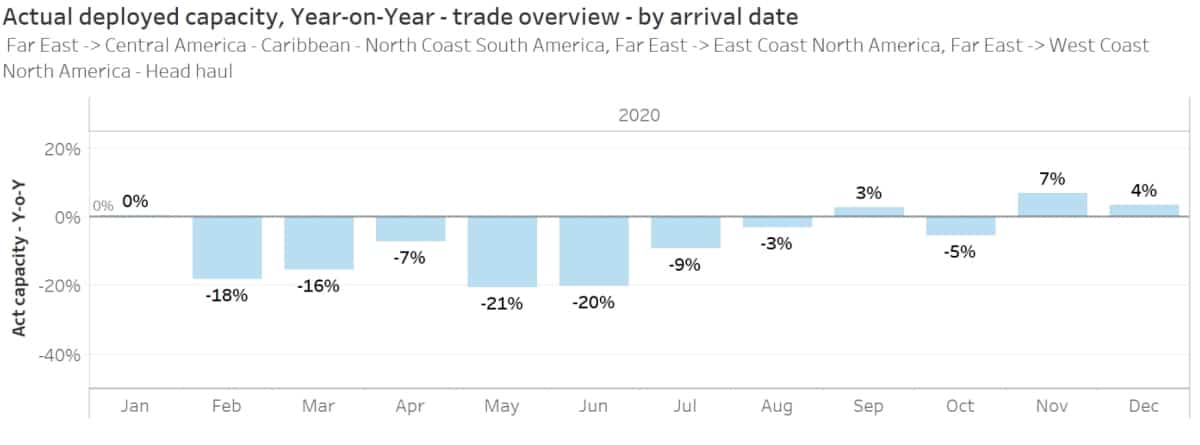

Measured in twenty-foot-equivalent units (TEU), not number of sailings, headhaul capacity to North America from Asia is down 21% this month compared to the original (pro forma) schedules, 19% next month and 7% in July.

The TEU capacity that remains in place after canceled sailings is down 21% this month year-on-year. It is down 20% year-on-year in June, and 9% in July.

Major capacity reductions in May and June are telling — and ominous. Lower cancellation numbers starting in July do not prove a positive trend because the carriers have not decided on schedule changes that far out. May arrival numbers are set in stone, June numbers have room to creep up, and numbers for July and thereafter could increase substantially.

Simon Sundboell, founder and CEO of eeSea, told FreightWaves, “If you look at July arrivals, cancellations were only 2% three weeks ago and now they are around 10%. The question is whether July, August and September will go up to the 19-21% range. They could definitely go up.

“The carriers already know what sort of [cargo] orders they have today, for example, for a ship leaving from Singapore three months from now, and they also know the capacity utilization they should be at for that ship three months before departure,” he said.

If current bookings stay too low compared to historical norms, carriers increase blank sailings to compensate. “This is why blank sailings are a hugely important leading indicator,” said Sunboell, who likened the data to a purchasing manager’s index for container-line purchasing managers.

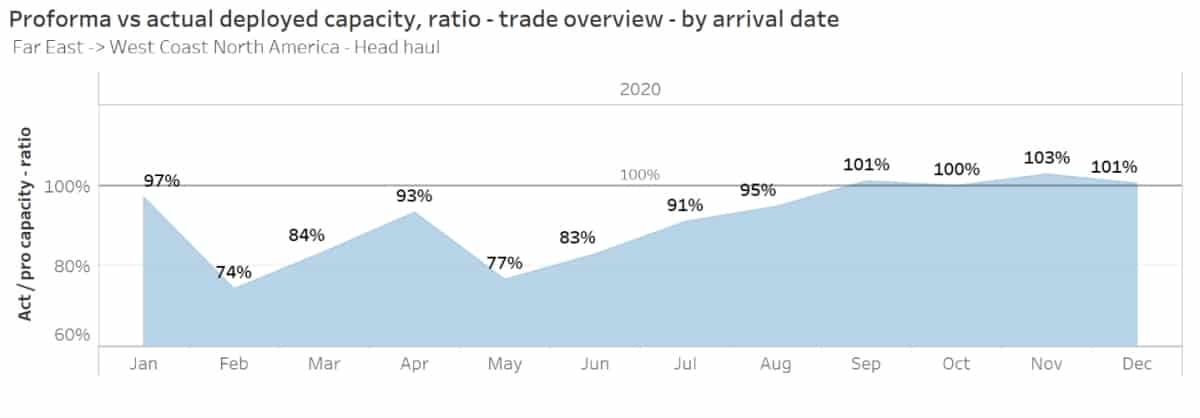

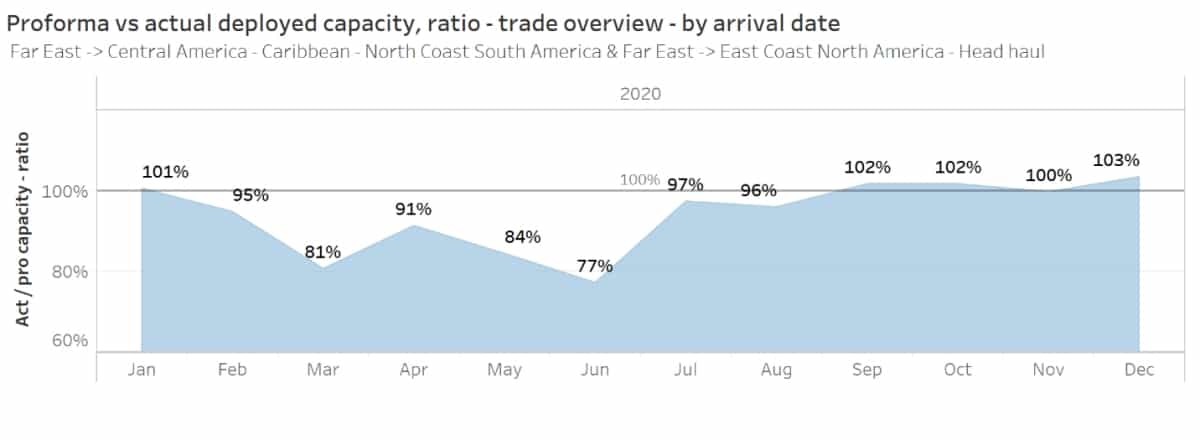

West Coast versus East Coast

The eeSea trade-lane data compares Asia-West Coast arrivals to Asia-East Coast arrivals. (The East Coast data includes arrivals to the Gulf Coast as well as arrivals in the Caribbean Basin transshipment region; the countrywide Asia-U.S. data includes Caribbean arrivals as well.)

Blank sailings will cut inbound TEU capacity to the West Coast by 23% this month and at least 17% next month.

The pattern is different on the East Coast, possibly because of the longer transit times from Asia. Blank sailings will reduce this month’s inbound capacity by 16% versus what was previously scheduled, and will lower next month’s capacity by at least 23%.

Sailing cancellations by arrival port

The eeSea port-level data provided to FreightWaves covers schedule changes on all mainline east-west and north-south trades, but not feeder and intraregional voyages.

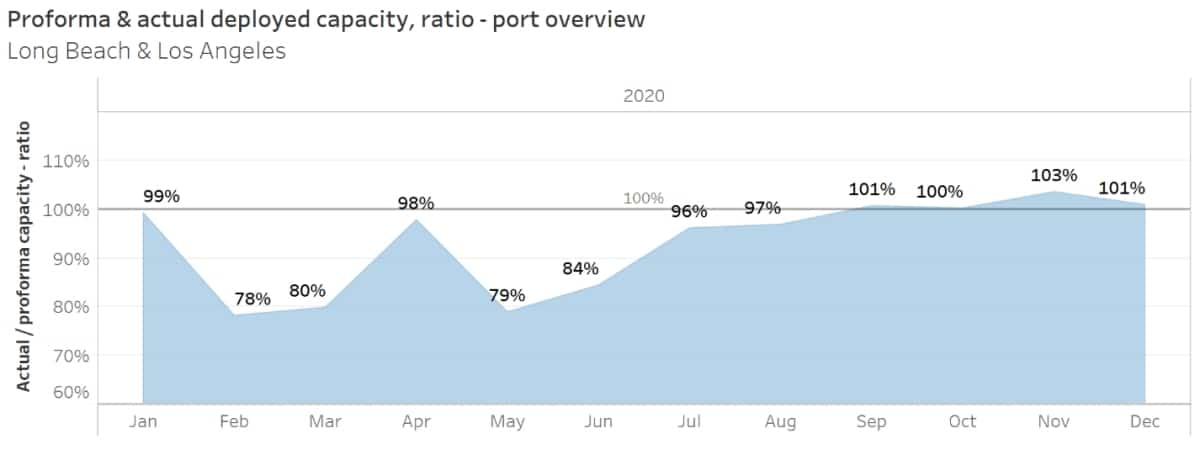

In Los Angeles/Long Beach, blank sailings have decreased this month’s TEU capacity by 21% versus previously scheduled levels, and June’s by 16%.

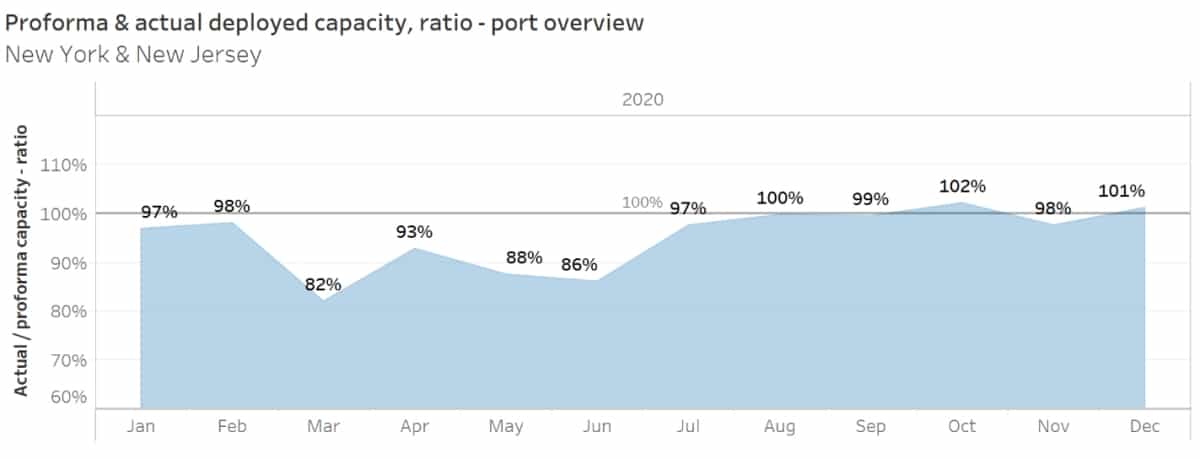

Declines are 12% this month in New York/New Jersey and 14% next month.

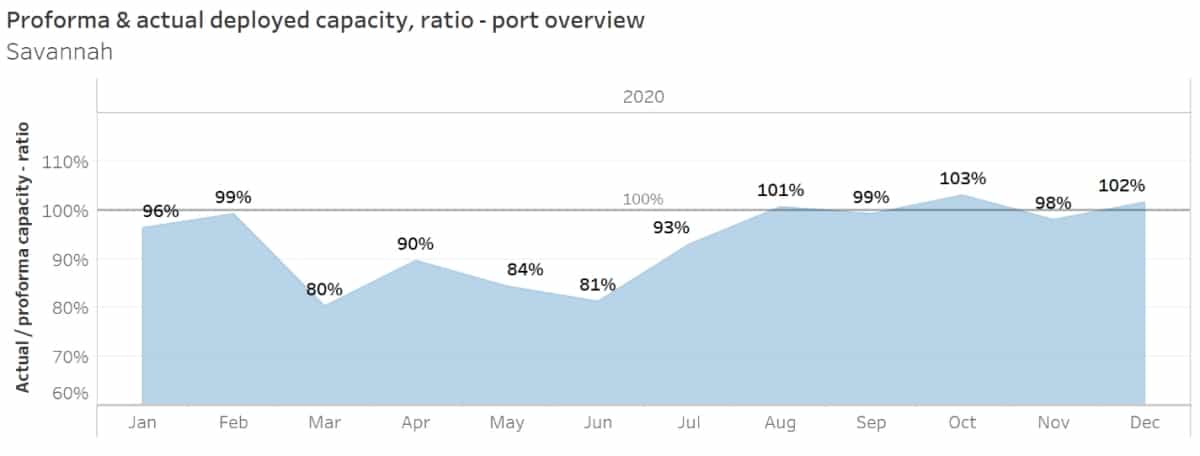

In Savannah, Georgia, capacity is down 16% this month versus what was previously scheduled, and down 19% next month.

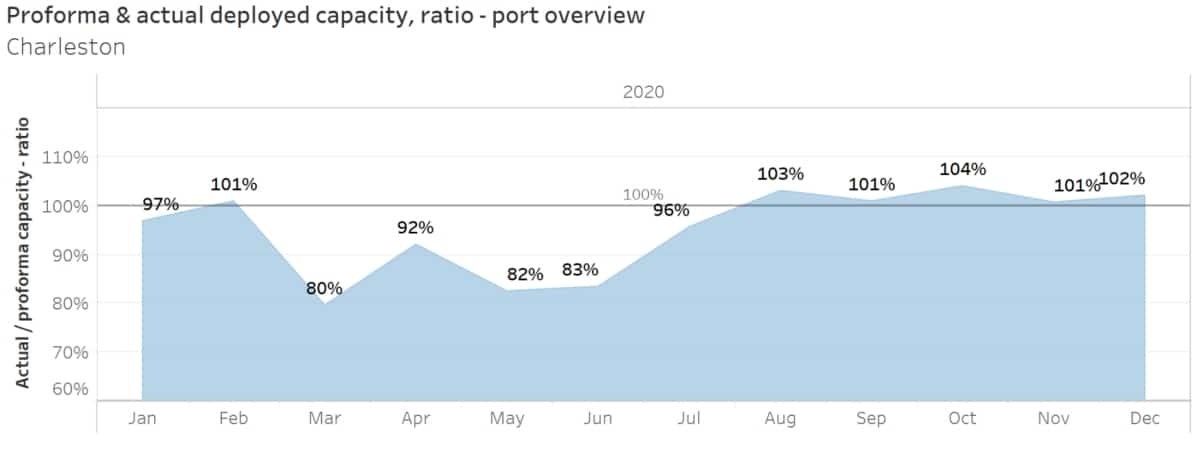

Declines are 18% this month for arrivals in Charleston, South Carolina, and 17% next month.

Interpreting the data

The most important takeaway from the eeSea data is that container-ship capacity to the U.S. will definitely fall, and fall sharply, both this month and next month — and possibly thereafter.

Declines will range from the teens on the East Coast to around 20% on the West Coast, both in relation to what was previously scheduled, and to the same month last year.

There are a few caveats, however. First, capacity is a strong leading indicator of throughput trends, because it shows carriers’ reaction to cargo demand, but ship-capacity reductions do not directly translate into volume reductions.

The relationship between capacity and volume depends on utilization — the percentage of available container slots on the ships that are used. If total ship capacity is reduced but average utilization is increased, TEU volume may fall at a slower rate than total ship capacity. If utilization decreases despite reduced total capacity, volume may decline faster than total capacity.

“There is not a one-to-one [correlation] between capacity and volume. The link between the two is utilization — which is the number everybody wants to know,” said Sundboell.

A second caveat to the data involves the port numbers, particularly on the East Coast. On the West Coast, sailings are more focused on Los Angeles/Long Beach. On the East Coast, noted Sundboell, “A 10,000-TEU ship may call at New York/New Jersey, Norfolk [Virginia], Savannah, Charleston and Jacksonville [Florida]. It could be dropping off 2,000 TEU at each port, or 4,000 TEU in New York/New Jersey and 1,000 TEU in Norfolk.”

The data would show that 10,000-TEU vessel as 10,000 TEU of capacity at each of those ports and schedule revisions would not show changes in that ship’s cargo allocations among the individual ports.

Value of blank-sailing data

On an individual company level, Sundboell explained that blank-sailing data is important for trucking businesses seeking to match capacity to expected carrier throughput, to terminals needing to gauge demand for longshoremen and cranes, and for individual shippers on the lookout for supply-chain disruptions.

“I have never had my phone ring more than for this particular product,” he exclaimed.

On a macro level, the greatest value of the blank-sailing data comes from monitoring it over time.

A month from now, if carriers have still not brought their July and August capacity cuts up to the 15-20% levels of May and June, it would imply that carriers see cargo demand rebounding — a positive signal on the coronavirus recovery.

If monthly capacity cuts remain persistently high at around 20%, or increase even further, the implications for the U.S. economy would be dire. Click for more FreightWaves/American Shipper articles by Greg Miller

Paul Maass

info