Industrial carbon dioxide shortage

The industrial CO2 shortage is a supply chain issue that stands to impact the consumer packaged goods industry heavily with food and beverage manufacturing representing approximately 70% of the industrial CO2 usage. It is used to make beer, soda and sparkling water taste like themselves. It is also used to preserve meat in the form of dry ice and in meat processing as a way to stun animals, making slaughterhouses more humane.

The industrial CO2 shortage is being felt by both CPG companies in North America and Europe, but the issue in Europe is more severe and promises to be long lasting. Part of the supply shortfall in the U.S. was caused by a shutdown from a naturally occurring source known as Jackson Dome, an underground deposit in Mississippi, that was resolved earlier this month.

Meanwhile, the European industrial CO2 shortfall is being more heavily caused by the skyrocketing natural gas prices on the continent that are nearly three times higher than they were just three months ago. That is causing fertilizer/chemical producers to cut back on production — industrial CO2 is a natural byproduct of that production. Not only have natural gas prices risen more in Europe than in the US, they are also much higher on an absolute basis, which has been greatly exacerbated by Russia withholding previously agreed upon natural gas volume, a seeming retaliatory response to western sanctions against it. Of course, no one can say how long the war between Russia and Ukraine — and the associated trade impacts — will last. Therefore, it appears this issue could be with the CPG industry for an extended period. CPGs should also consider the related impact that rising natural gas prices could have on consumer demand in Europe as the continent faces “terrible winters” ahead, assuming that natural gas prices stay high. Due largely to energy, inflation has been even higher in Europe than in the U.S. — consumer prices in the U.K. were 10.1% higher in July year over year.

Railroad strike in next month seems less likely than it did a week ago

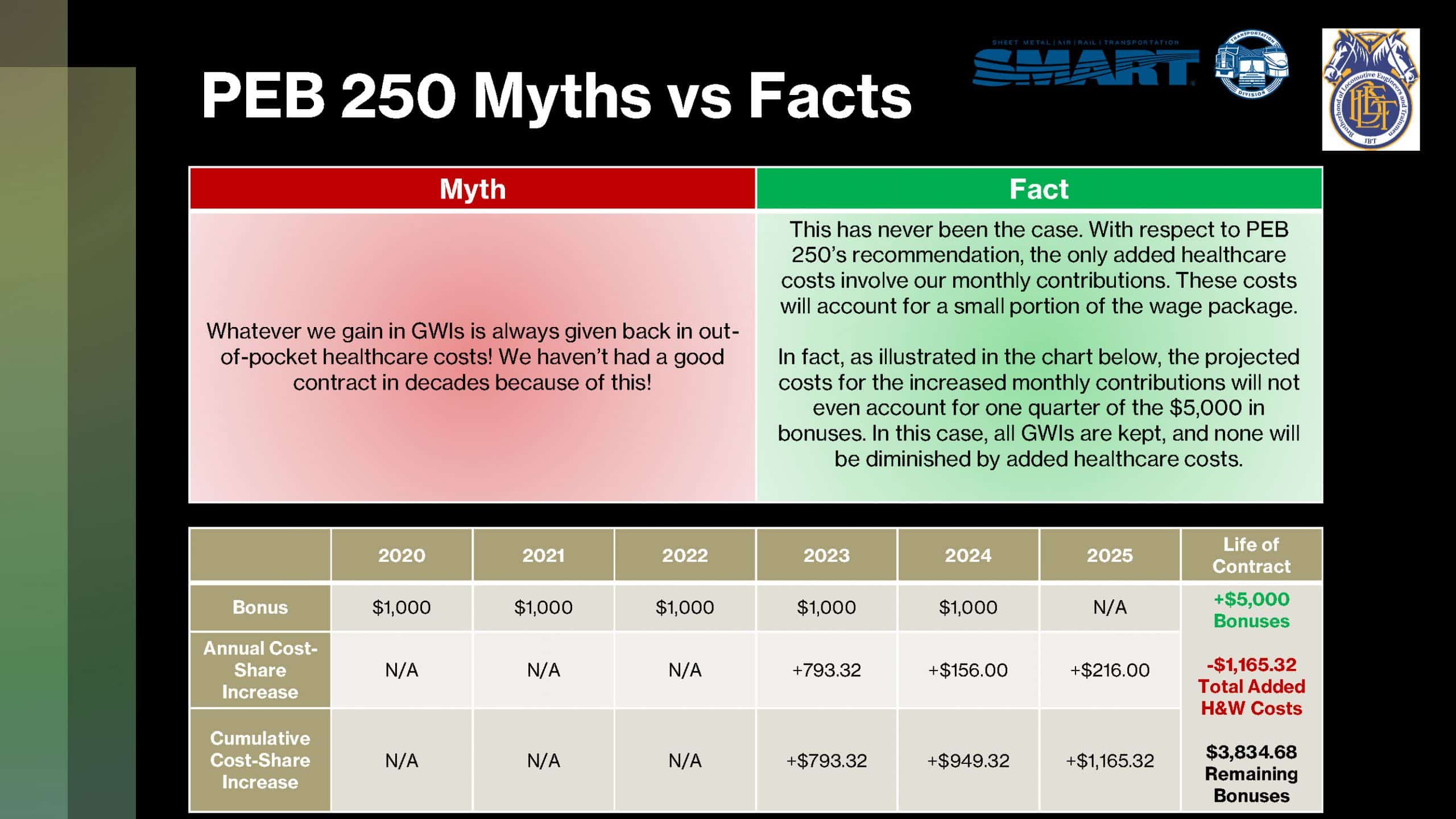

On Monday, three railroad unions reached tentative agreements toward ending their contract standoff. While those three only represent 11% of the total employees that are represented by unions currently in the middle of negotiations and the agreements still need to be ratified, I believe it represents a significant step toward avoiding a rail strike. Following the recommendations of the Presidential Emergency Board (PEB), if ratified, the union workers would receive a 24% compounded raise for the five-year period from 2020-24 among other adjustments to health benefits and paid time off.

What I have found most interesting of late on the topic of rail labor discussions is that the unions, including the Brotherhood of Locomotive Engineers and Trainmen (BLET) and the Sheet Metal, Air, Rail and Transportation Workers (SMART), have been dispelling “myths” associated with the PEB report. Here is an example where the unions are educating members on the PEB recommendations. The unions appear to be trying to persuade members that an ultimate resolution that is roughly in line with the PEB’s recommendation would be balanced between management and labor interest and one that they should vote to ratify. It appears to me that a strike is in no one’s best interest, and the negotiation process under the Railway Labor Act is designed to prevent a work stoppage, which is now less likely to happen with three unions reaching tentative agreements.

{kind=link}

Cross-border rail capacity expansion — implications for agriculture and intermodal

Class I railroad Kansas City Southern is set to build a $75 million rail bridge in Laredo. The bridge would represent a major capacity expansion at North America’s busiest freight border crossing, potentially doubling the number of trains that can be processed in that location. The pending merger with Canadian Pacific and the capacity expansion at the border have the potential to impact numerous rail traffic segments — the ones most relevant to CPG are agriculture and intermodal. The pending merger would extend the reach of the combined railway without interchange, potentially allowing for easier marketing of Canadian grain in Mexico. In intermodal, the developments have the potential for enabling a service from the Port of Lazaro Cardenas, on Mexico’s west coast, to Chicago that is competitive with routes from Los Angeles/Long Beach to Chicago, the densest intermodal lane in North America.

I recommend checking out my interview with Kevin Williamson, CEO of RJW Logistics Group.

RJW Logistics Group is an asset-heavy 3PL that has a specialty in guiding CPGs through their retail relationship and the middle-mile segment of their freight networks. Topics discussed on the show included the relative advantages/disadvantages of a collect delivery system versus a prepaid one, how CPGs can improve their on-time and in-full percentages and thus avoid retailers’ penalties and value-added services that can be provided by 3PLs.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, click here. For more information on SONAR or to request a demo, click here.