Knight-Swift Transportation Holdings, Inc. (NYSE: KNX) reported second quarter 2019 adjusted earnings per share (EPS) of $0.58 compared to analysts’ expectations of $0.57 and within its recently lowered guidance range of $0.57 to $0.58. Adjusted EPS were $0.02 higher year-over-year.

On July 17, North America’s largest truckload (TL) transportation company issued a press release lowering its earnings expectations, citing an oversupply of capacity in the TL freight market, which is creating a drag on revenue per loaded mile (excluding fuel surcharge).

KNX reiterated its recent guidance change, which calls for adjusted third quarter 2019 EPS in a range of $0.54 to $0.57 and fourth quarter 2019 adjusted EPS in the range of $0.73 to $0.77. Management said that this guidance assumes revenue per loaded mile will move negative year-over-year as prior contractual rate increases lap favorable year-over-year comparisons and the spot market is providing “less favorable” opportunities. Additionally, management expects typical sequential seasonal trends in the third and fourth quarters and believes that declines in miles per tractor will ease.

When discussing their 2019 market outlook, management noted that significantly lower truck and trailer orders, an increase in truck order cancellations, weakness in the used equipment market and an increase in carrier bankruptcies signal that capacity reductions are underway. Management believes that revenue will continue to be pressured as there are “fewer and less attractive non-contract opportunities,” but believes that acquisition opportunities have increased throughout the industry.

The carrier generated $1.242 billion in total revenue, down 6.7 percent year-over-year, down 5.7 percent excluding fuel surcharges. Revenue declines were seen across all three segments, with the bulk of the year-over-year decline being attributed to the TL segment, which was down 4.3 percent excluding fuel surcharges and intersegment transactions.

From the press release, “Our consolidated operations continued to show progress and resilience, as we navigated through the softer freight environment in the first and second quarters of 2019. Focusing on the fundamentals of our business enabled us to improve our adjusted operating income by 1.5 percent to $137 million, despite a 5.7 percent decrease in revenue, excluding trucking fuel surcharge, from the second quarter of 2018 to the second quarter of 2019.”

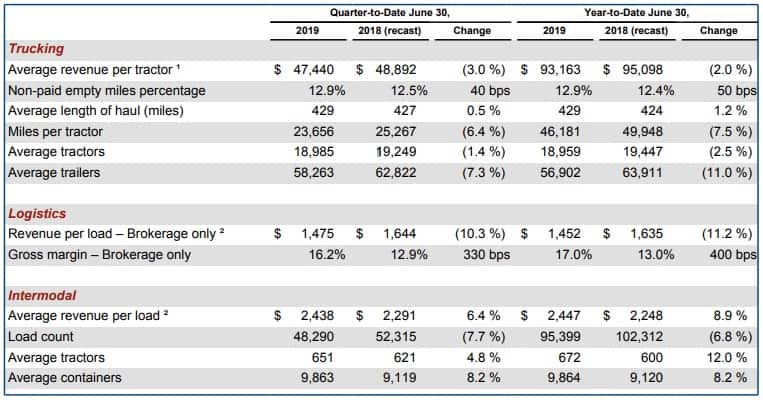

Truckload

The more than 4 percent decline in TL revenue was due to a 3 percent year-over-year decline in average revenue per tractor, a 6.4 percent decline in miles per tractor, a 40 basis point increase in empty miles (12.9 percent empty mile percentage) and a 264-unit decline in average tractors. Some of the revenue degradation was partially offset by a 4.1 percent increase in revenue per loaded mile. TL adjusted operating income improved 1 percent year-over-year to $128.3 million as KNX’s adjusted operating ratio (OR) improved 70 basis points year-over-year to 85.8 percent. Swift’s TL fleet reported year-over-year and sequential adjusted OR improvements at 84.2 percent compared to Knight’s trucking fleet which operated at an 81.8 percent adjusted OR.

Logistics

Logistics revenue, primarily Knight and Swift’s brokerage services, declined 16.7 percent year-over-year to $80.3 million as loads declined 3.9 percent and revenue per load declined 10.3 percent to $1,475. The adjusted OR improved 150 basis points to 93.7 percent as brokerage gross margins improved 330 basis points year-over-year to 16.2 percent. Segment operating income improved 8.8 percent to $5 million in the period.

From the press release, “A competitive market during the second quarter of 2019 resulted in a 13.8 percent decrease in brokerage revenue, excluding intersegment transactions, as compared to the second quarter of 2018. Competition increased as the quarter progressed, putting more pressure on revenue and margins.”

Intermodal

Intermodal revenue declined 1.8 percent year-over-year to $117.7 million as load counts declined 7.7 percent, which was partially offset by a 6.4 percent increase in average revenue per load. The adjusted OR deteriorated by 10 basis points to 96.4 percent. Operating income declined 6.4 percent to $4.2 million in the period. Management said that the “competitive market pressured volumes and revenue” and reiterated its plans to drive costs lower in the division and grow intermodal volumes.

Shares of KNX are up more than 2 percent on the earnings report.