Knight Swift warned last week that its numbers would be a disappointment and its earnings release Wednesday morning confirmed that.

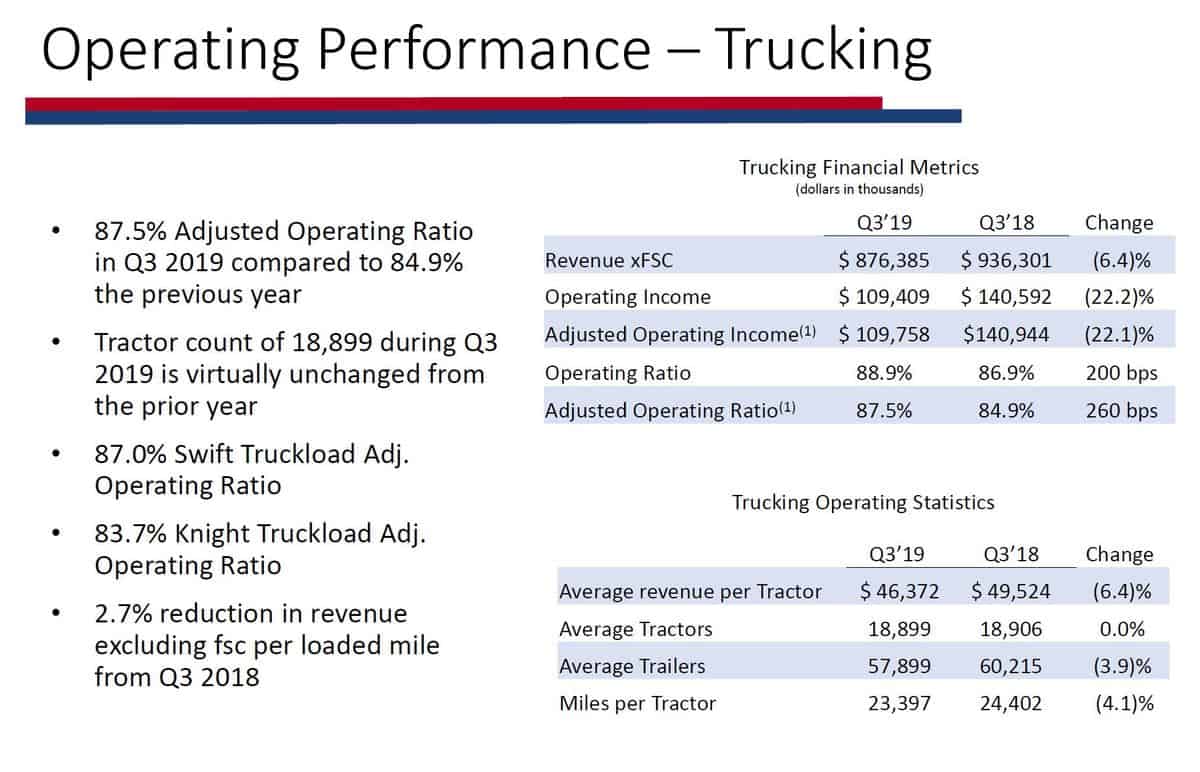

Revenue for the entire company (NYSE: KNX) including fuel surcharge dropped 10.8% to just a small amount over $1.2 billion for the quarter ended September 30. Excluding fuel, the decline was 10.1%.

Operating income was down 28.6% for non-adjusted results and down 27.4% for adjusted operating income.

The end result of all that was an adjusted earnings per share of 48 cents/share, which is what Knight Swift said last week would be its result for the quarter. That was down from earlier company guidance that its earnings would come in at 54-57 cents/share.

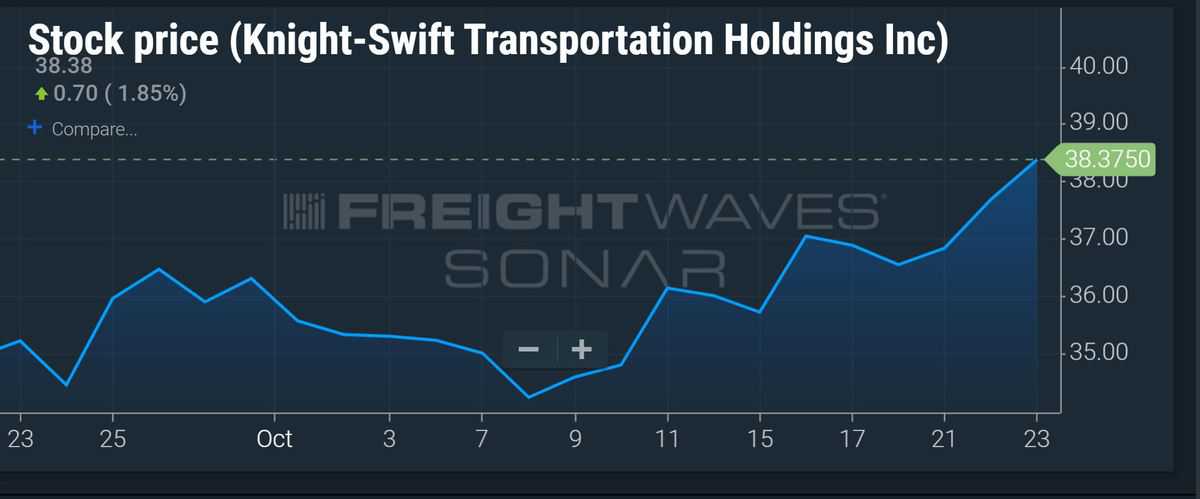

The result on Wall Street? The price of KNX was rising midday Wednesday, up 1.57% to $38.25/share. Since the announcement of the revenue and earnings shortfall on October 15, the stock is up about $2.35 from the close that day of $35.91 per share. In the last 52 weeks, with KNX having been scorched like most trucking stocks in the middle of last year – the market assuming that the fantastic second quarter of 2018 was likely a market high – the stock price of KNX is up more than 26%.

Although the disappointing numbers had been signaled, Amit Mehotra’s team at Deutsche Bank said Wednesday morning the results were “a bit weaker than we expected.” Specifically, Deutsche cited an operating ratio at Swift of 87%, a decline of 250 basis points compared to the corresponding quarter of last year.

The report was “so bad it’s good,” Deutsche said, which has helped propel the stock higher. Deutsche has been positive on the KNX stock recently, with “market participants seemingly willing to discount a positive inflection in the second half of 2020, and in this context the worse it is today, the easier the comparisons this time next year (which is a reasonable thesis for a highly fragmented industry like truckload).” But the performance in Swift’s truckload operations was a disappointment, and “the performance likely reflects the dearth of volume and yield opportunities that were specific to the (quarter), but nonetheless the weaker performance at SWFT does create some questions around valuation, which has propelled KNX shares higher in recent weeks.”

Knight’s operating ratio (OR) was 83.7%. As a whole, the full company’s OR declined to 88.9% from 86.9%, and on an adjusted level, the decline was to 87.5% from 84.9%.

The performance on the road for the truckload division of Knight Swift was pretty much as one would have expected given the projected turndown in earnings. Average revenue per tractor fell 6.24% to $46,372. Miles per tractor dropped to 23,397 from 24,402.

The decline in operating income came even as the company kept its expenses in check, declining close to $42 million. But salaries were only down less than $6 million while revenues were falling $146 million.

Declines in the company’s intermodal division were expected to be a key reason for the decline and the actual numbers showed that. The IM division at Knight Swift posted a $2.65 million operating loss for the quarter, against operating income in the corresponding quarter last year of about $9.7 million. The OR for intermodal both adjusted and non-adjusted was 102.4%.

Revenue for the group was down to $108.7 million from $130.1 million. The transportation team at Morgan Stanley said last week after the Knight Swift announcement of lower expected earnings that intermodal looked like a key cause. “While most investors have been focused on stabilizing spot rates, pickup in volumes with peak season and limiting the downside in contract rates in 2H, management commentary implies the drag came from IM (increased competition within the intermodal market, leading to unexpected reductions in volume and revenue per load) primarily together with a soft (truckload) rate environment,” Morgan said at the time.

On a more granular basis, the intermodal average revenue per load was down 6.8% for the quarter, to $2,393 from $2,568. The load count dropped 10.3% to 45,445.